.png)

Volumes remain muted on Term amid a broader lack of yield opportunities across all of DeFi. Staple yield-bearing strategies, such as basis-driven yields from Ethena, have collapsed, and activity among DeFi-native yield farmers has fallen sharply. On the ETH side, some residual borrowing remains and continues to roll but as ETH staking rates continue to drift lower expect volumes to decline in the near term.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

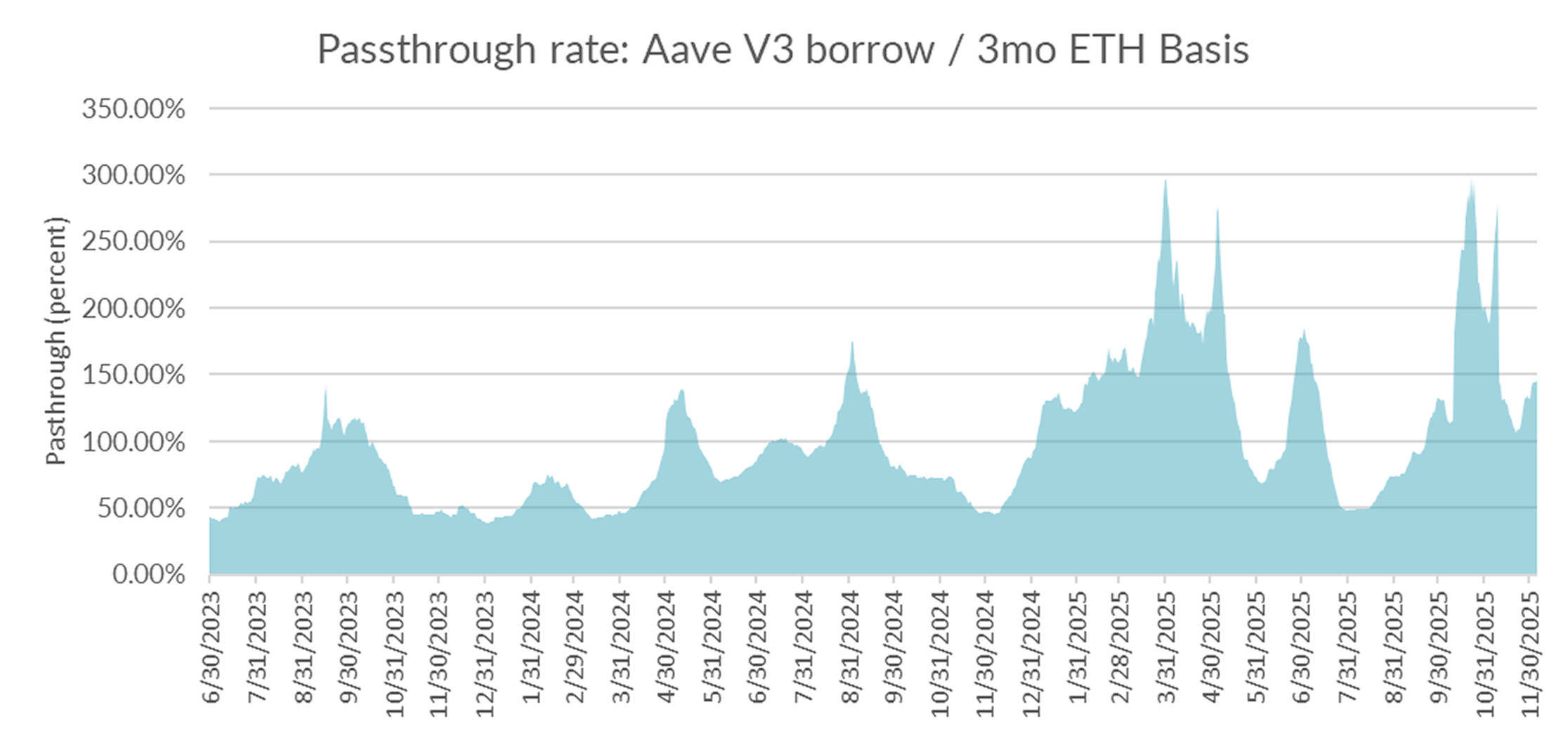

In derivatives markets, funding rates were mixed, with 3-month basis rising +7bps to 4.67% and perpetual funding rates falling by -55bps to 3.63% on a 30-day trailing basis.

After a brief reversal, perpetual rates are back on the decline going into year-end.

The lack of renewed demand for leverage on this week’s pop suggests limited conviction in a sustained bounceback.

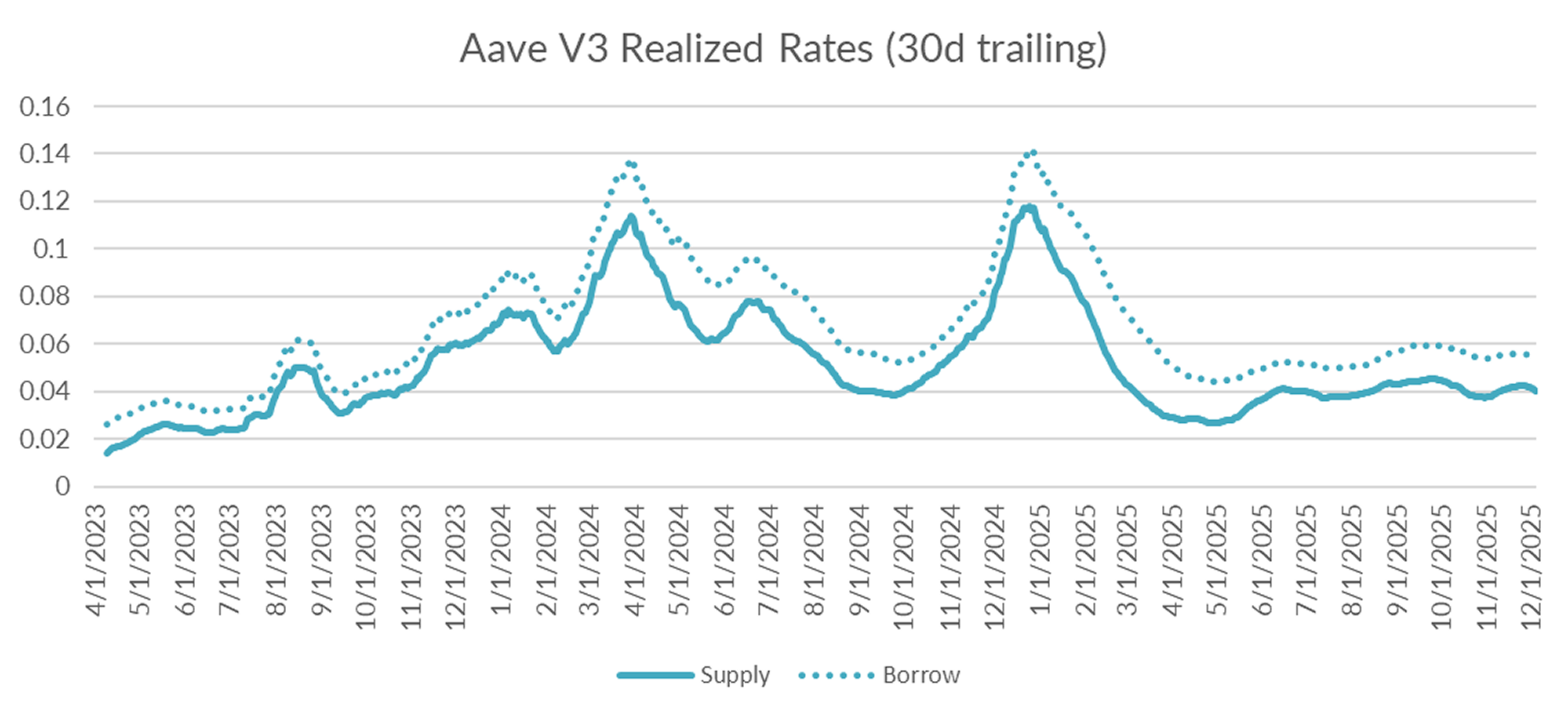

Turning to DeFi variable rate markets, the 30-day trailing average declined by -23bps to 5.32% on a 30-day trailing basis. On a shorter lookback, USDC borrow rates averaged 4.73%, suggesting that rates are likely to continue to decline in the near term.

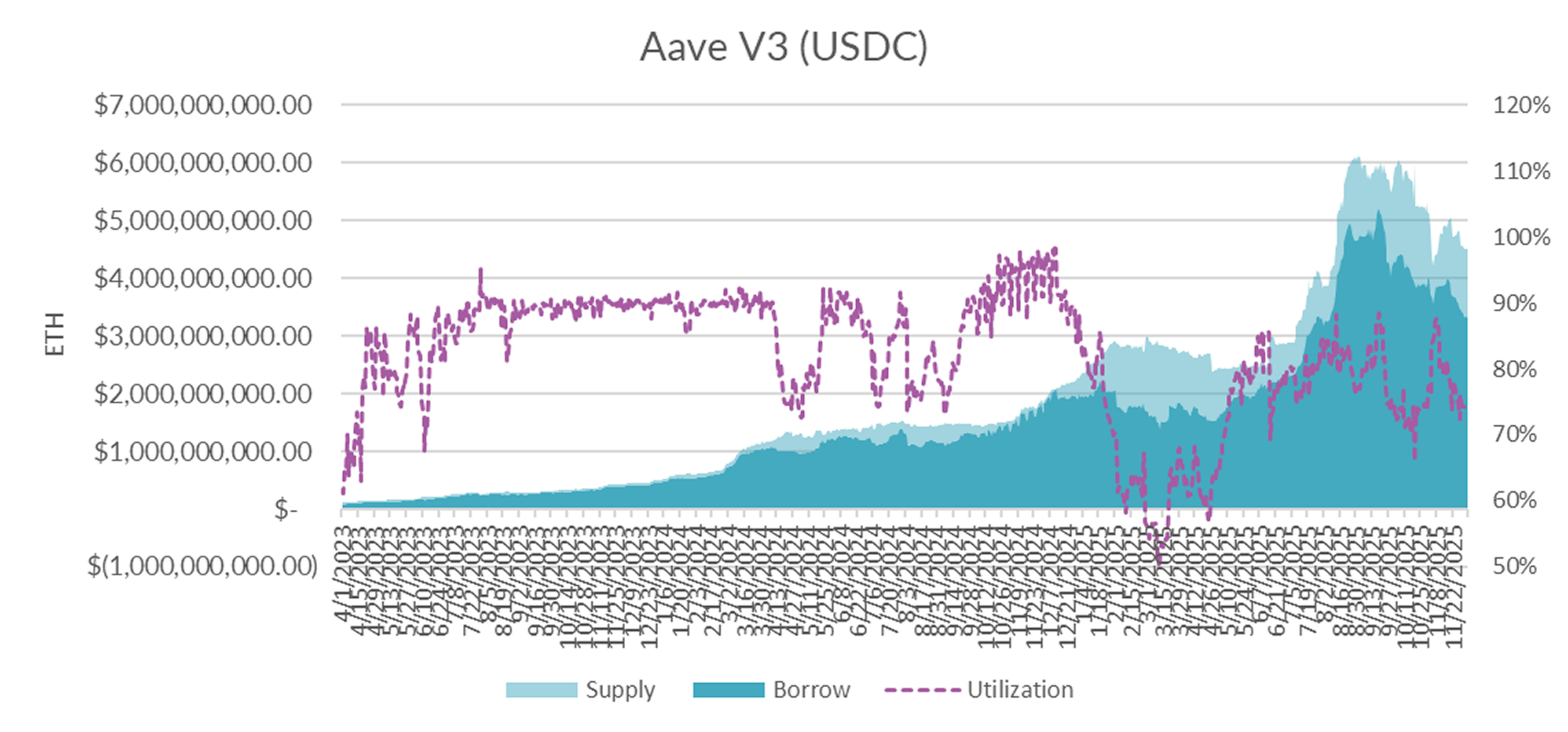

Diving into the microstructure of Aave’s USDC markets, internal metrics show utilization steadily declining into the low-70% range, driven by continued deleveraging and only partially offset by supply exiting alongside borrow demand.

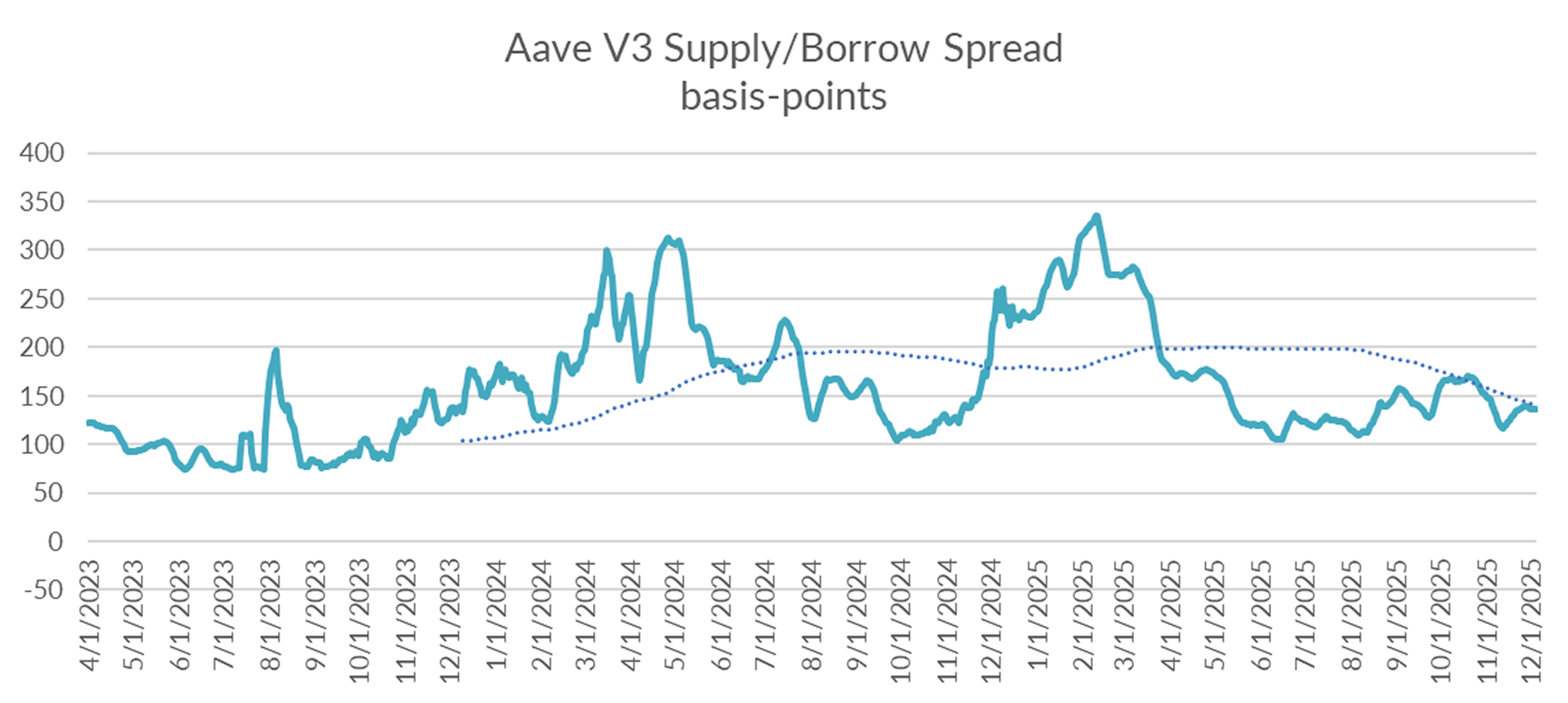

With utilization back down to 73%, expect the supply/borrow spread to rise back toward historical averages of +150%.

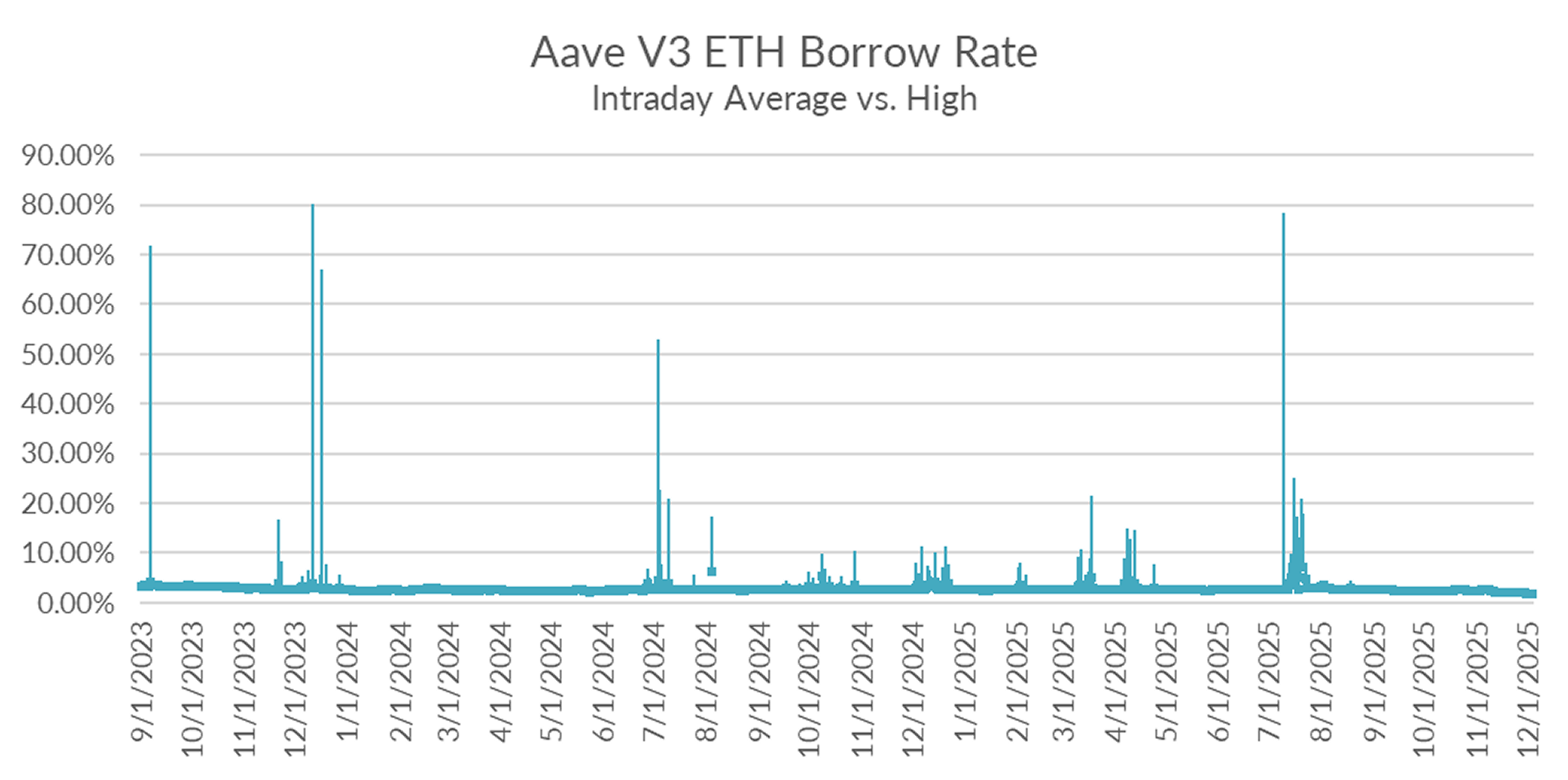

A glimpse into intraday rate dynamics show that the market remains liquid with no signs of any intraday squeeze over the past week.

Given the subdued state of DeFi yield markets more broadly, we expect deleveraging to persist as the new normal sets in.

Turning now to ETH markets, ETH rates fell -14bps on the week to 2.08% on a 30-day trailing basis. This move is consistent with the broader trend in the CESR staking index, which declined- 5bps to 2.85% over the same period, though ETH borrow rates are falling at a notably faster pace.

Internal market microstructure shows that utilization remained low with little to no pickup in demand to absorb the +150K of ETH deposited over the past week.

Consistent with this picture, no sign of liquidity stress can be found in intraday charts.

With utilization hovering just above 60% and supply continuing to flow in with little corresponding pickup in demand, an adjustment to the optimal rate appears likely in the near term.

Markets closed the week mixed, with BTC down 1.86% and ETH up 1.15%. Basis rates continue to signal limited appetite for leverage from the fast-money community, offering little evidence of a near-term trend reversal. With the holidays approaching, volumes are expected to remain light and price action choppy. This directionless trading, with risk skewed to the downside, suggests DeFi rates are likely to remain suppressed in the foreseeable future.