.png)

Volumes on Term remain light. We’re beginning to see reverse inquiries to borrow against USD-denominated exotics, but the market still refuses to reprice risk. As a result, no stablecoin loans cleared except those backed by liquid collateral. And that’s fine—sometimes the best trade is no trade when the alternatives, such as Euler or Morpho, are clearly mispriced..

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

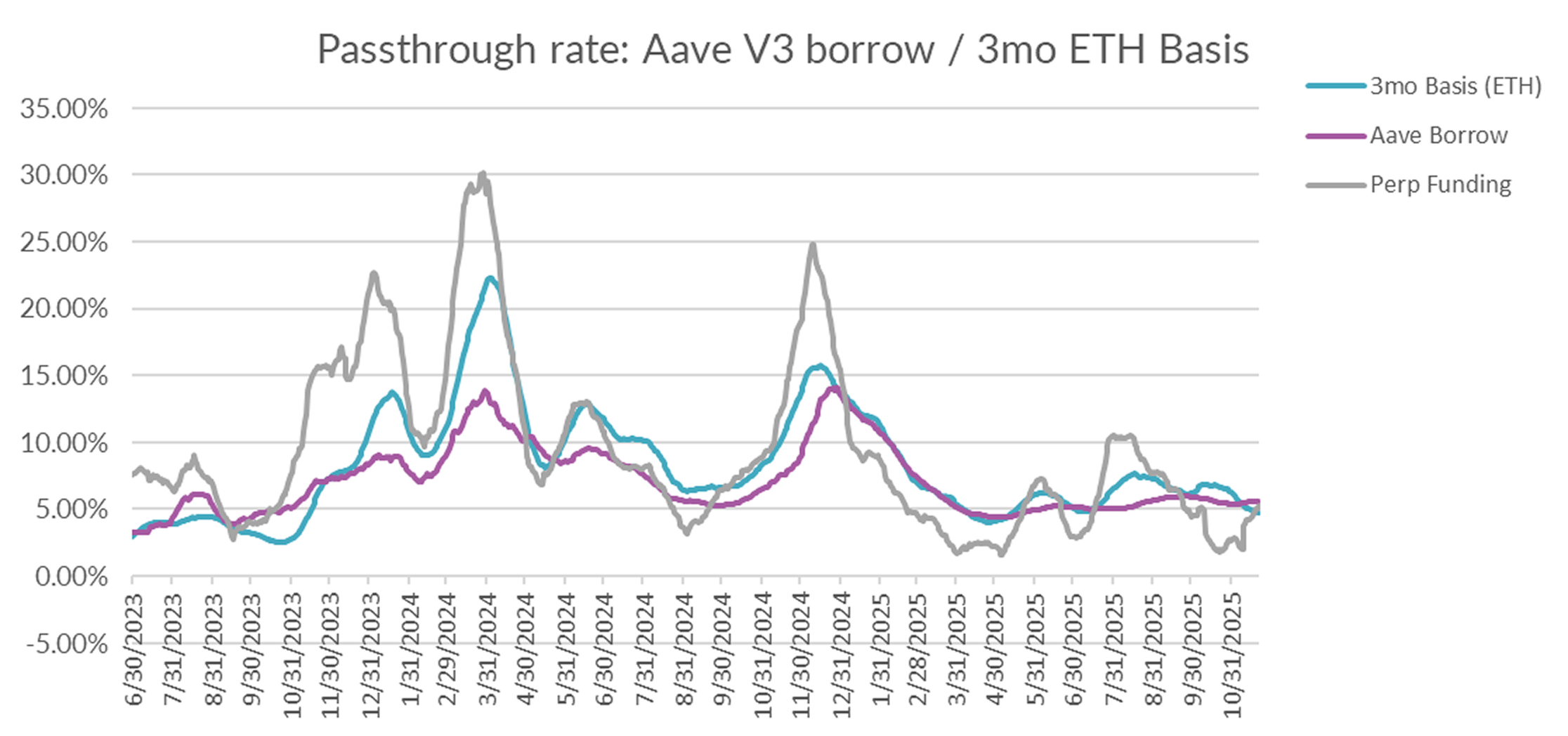

Basis and Perpetuals Markets

In derivatives markets, funding rates were mixed, with 3-month basis falling another -28bps to 4.72% and perpetual funding rates rising by +103bps to 5.22% on a 30-day trailing basis.

This reversal in perp funding rates continues to normalize the spread between DeFi and CeFi rates back toward historical averages.

The continued recovery in perp funding rates suggests short-term traders are covering hedges, while the ongoing decline in 3-month basis indicates that longer-term participants continue to delever and pare back risk.

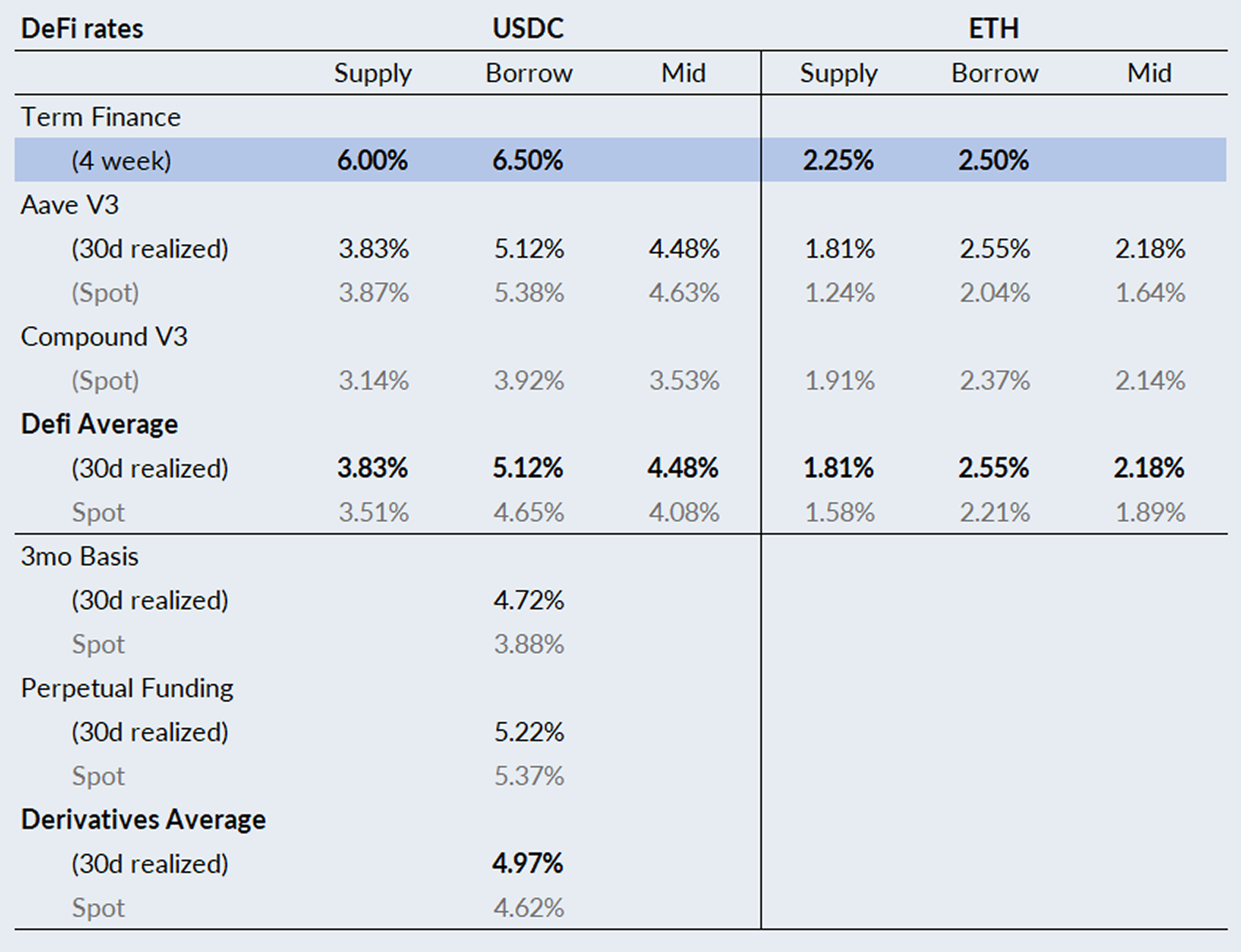

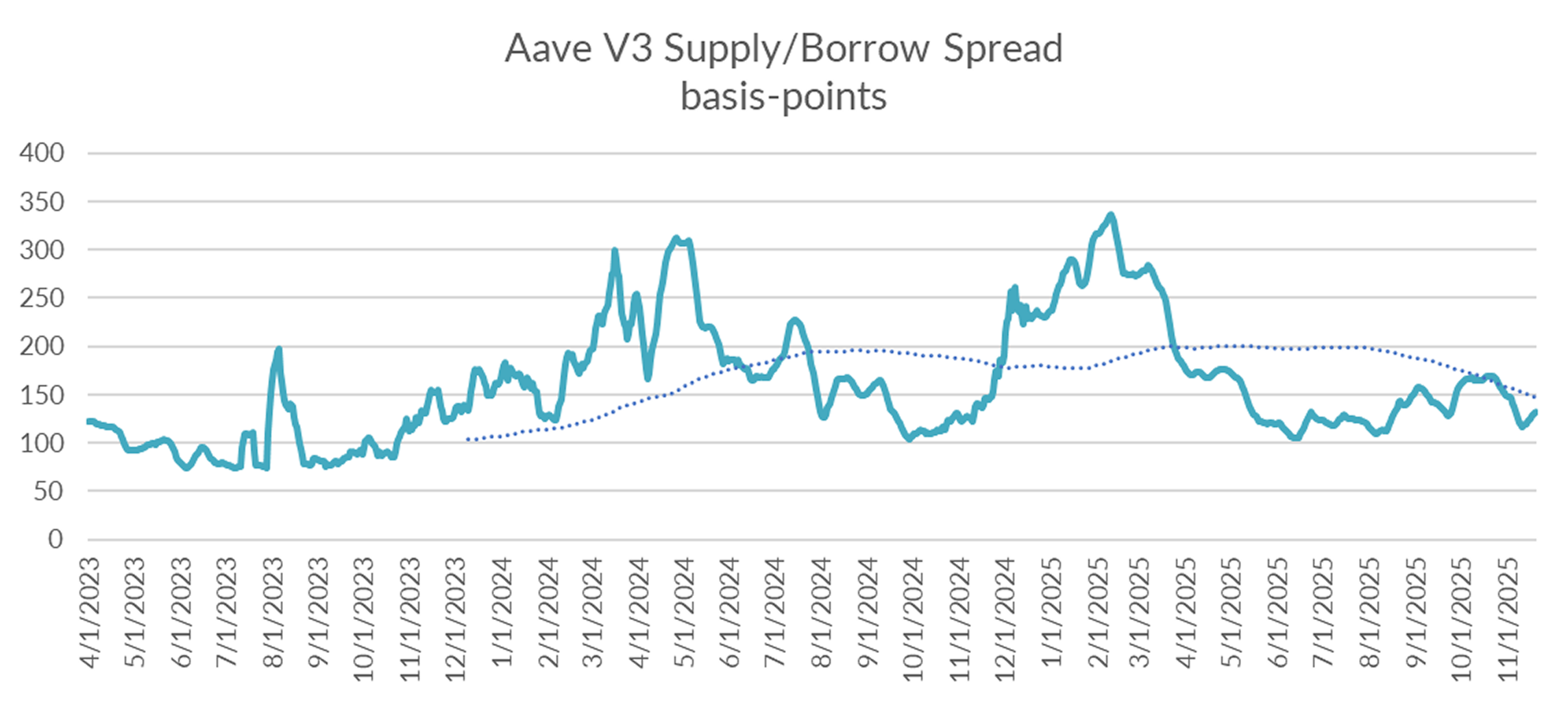

USDC Markets

Turning to DeFi variable rate markets, the 30-day trailing average closed roughly unchanged at 5.55% on a 30-day trailing basis. On a shorter lookback, USDC borrow rates averaged 5.48%, suggesting that rates are relatively stable at current levels.

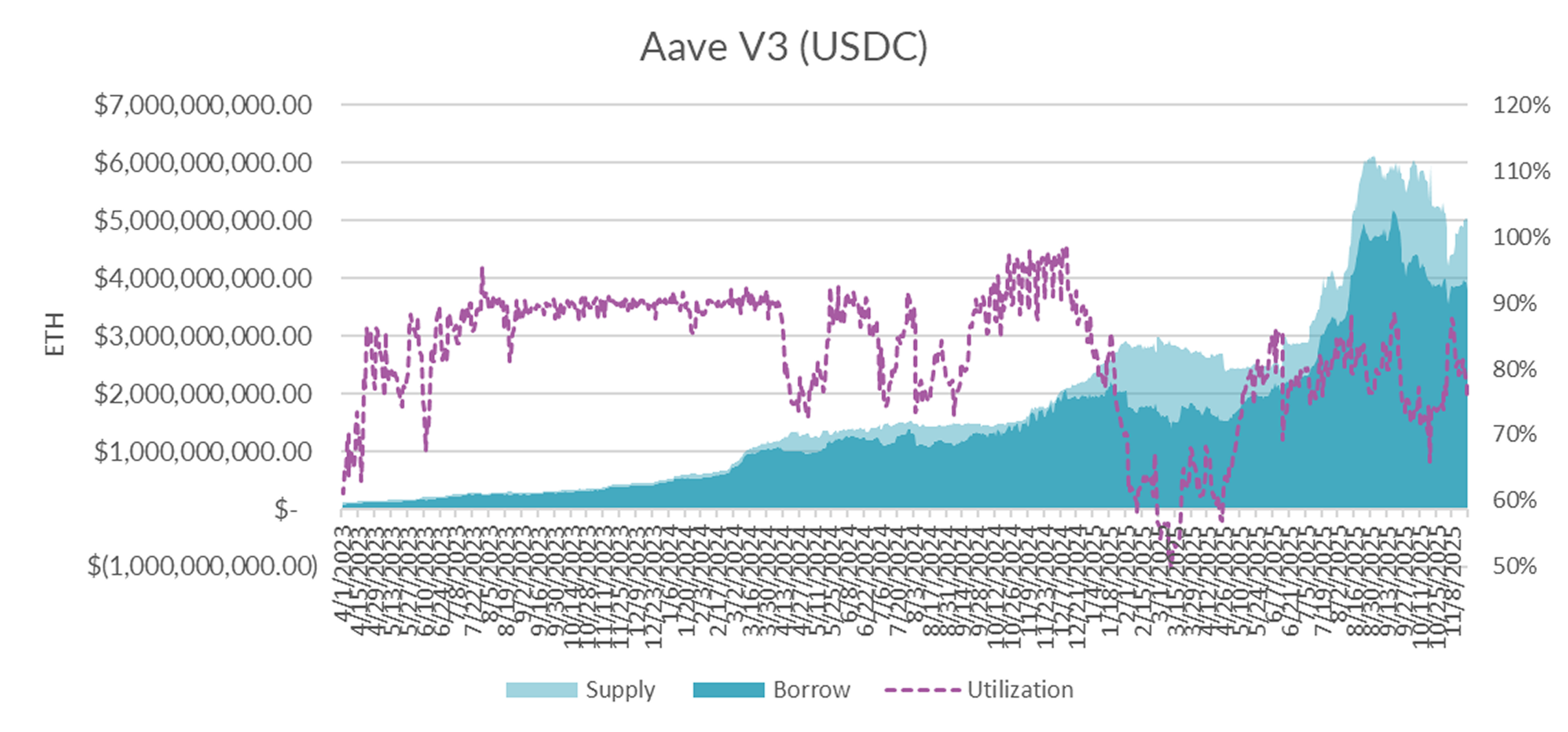

Diving into the microstructure of Aave's USDC markets, internal metrics show a dip in utilization back down to 76% driven by a mix of recovering supply (+133M) and lower demand (-69M).

With utilization back down to 81%, expect the supply/borrow spread to rise back toward historical averages of +150%.

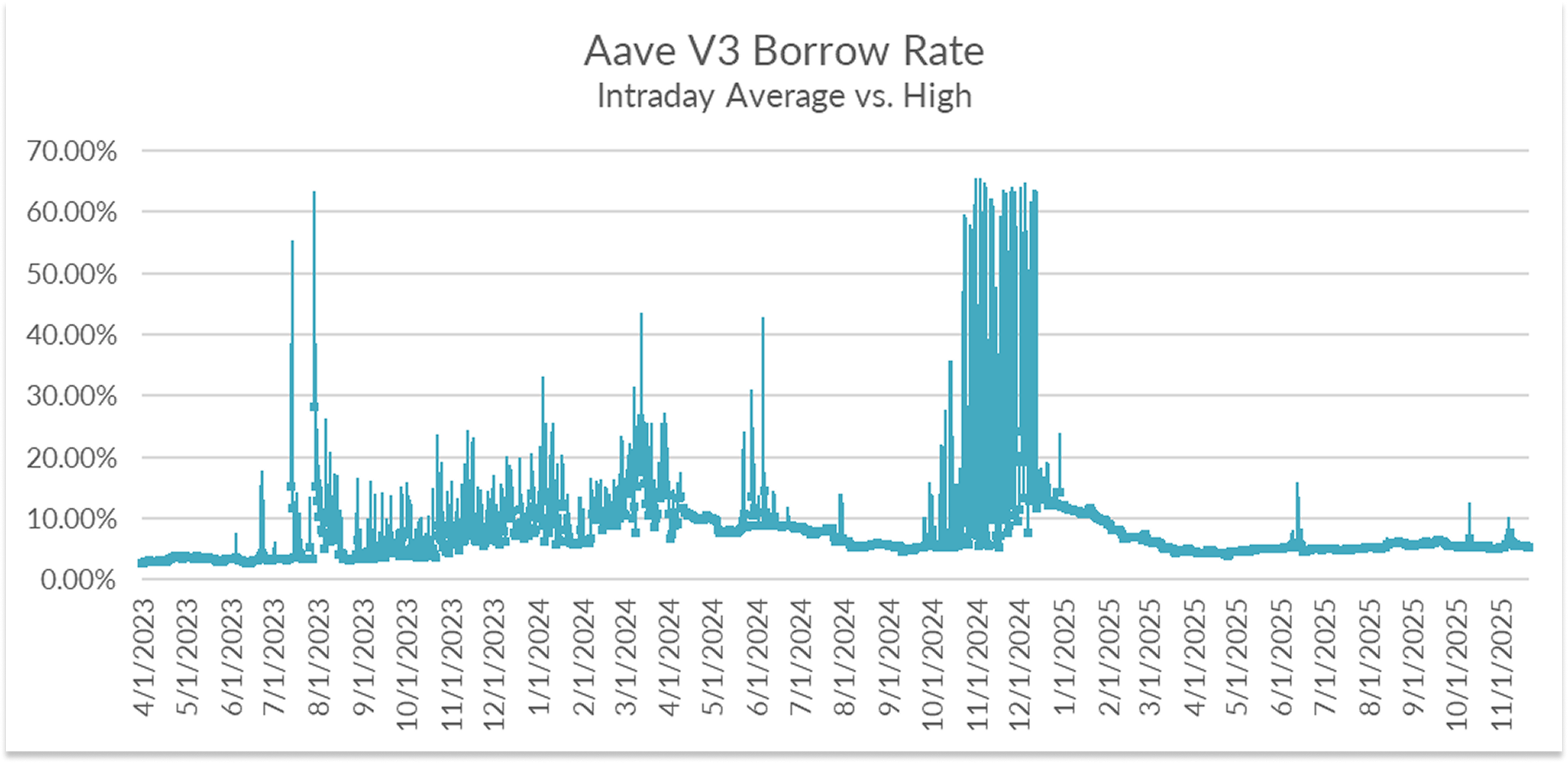

A glimpse into intraday rate dynamics show that the market remains liquid with no signs of any intraday squeeze over the past week.

In the near term, even if broader cryptoasset prices begin to stabilize, the absence of a strong catalyst makes a swift rebound unlikely. In the meantime, expect rates to remain stable and markets to stay risk-averse.

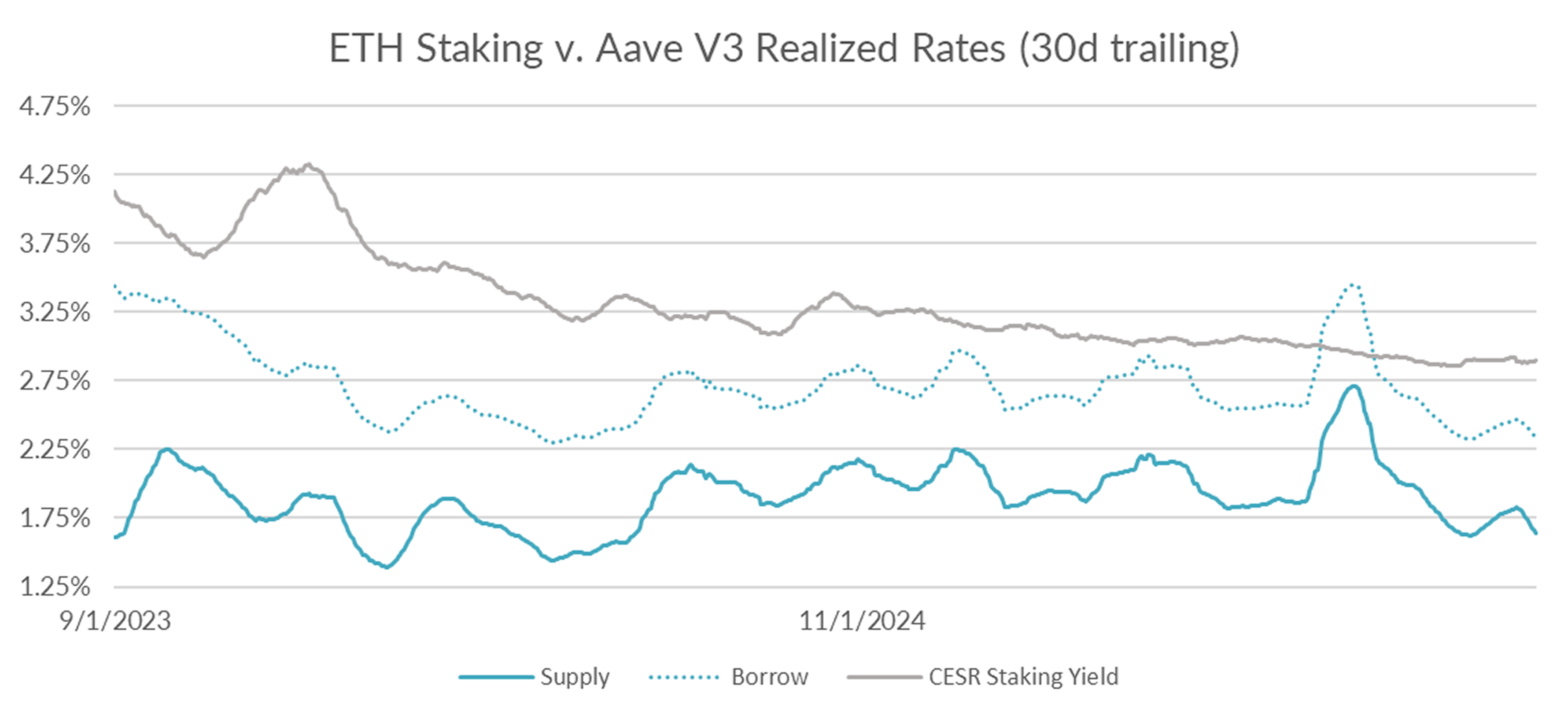

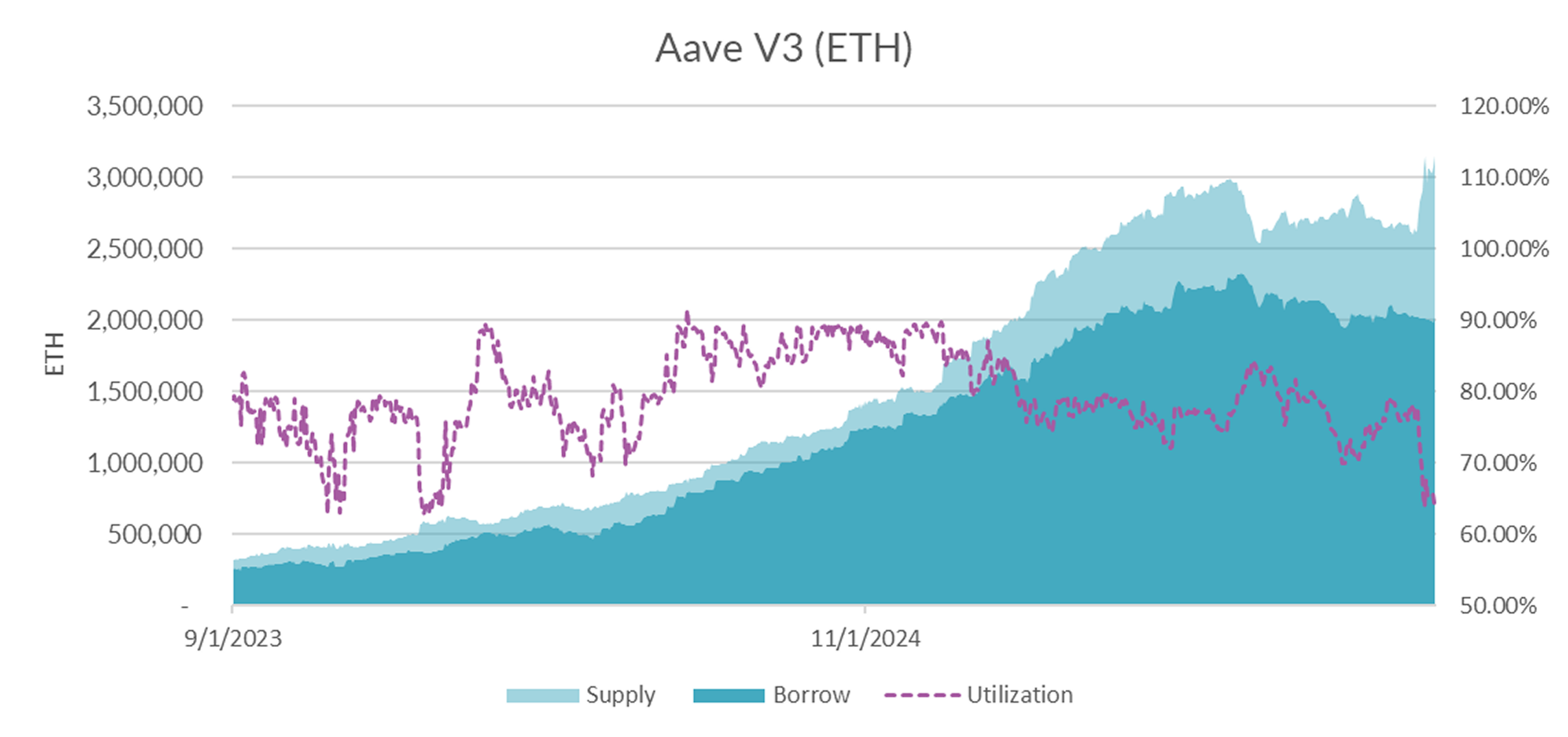

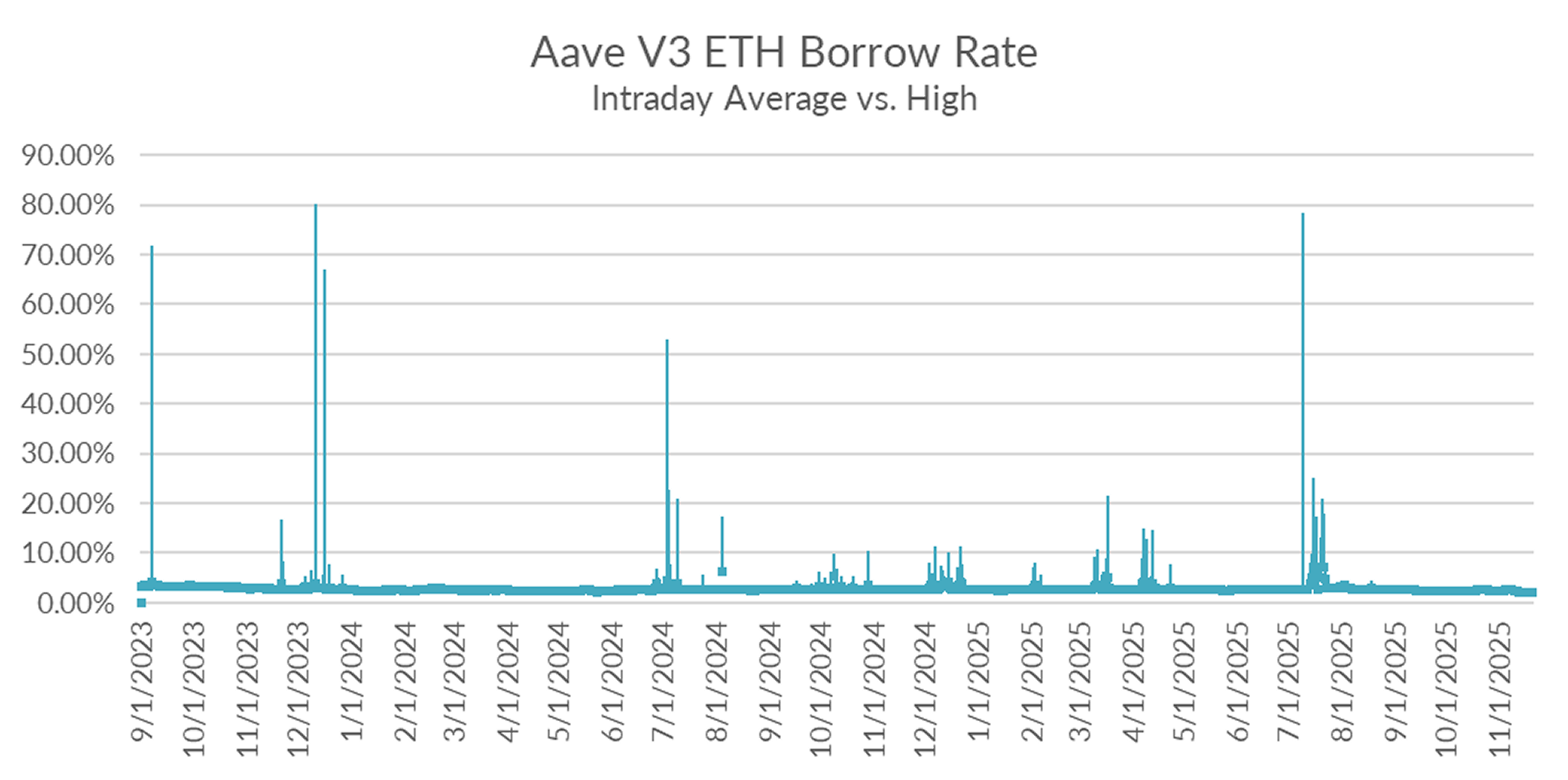

ETH Markets

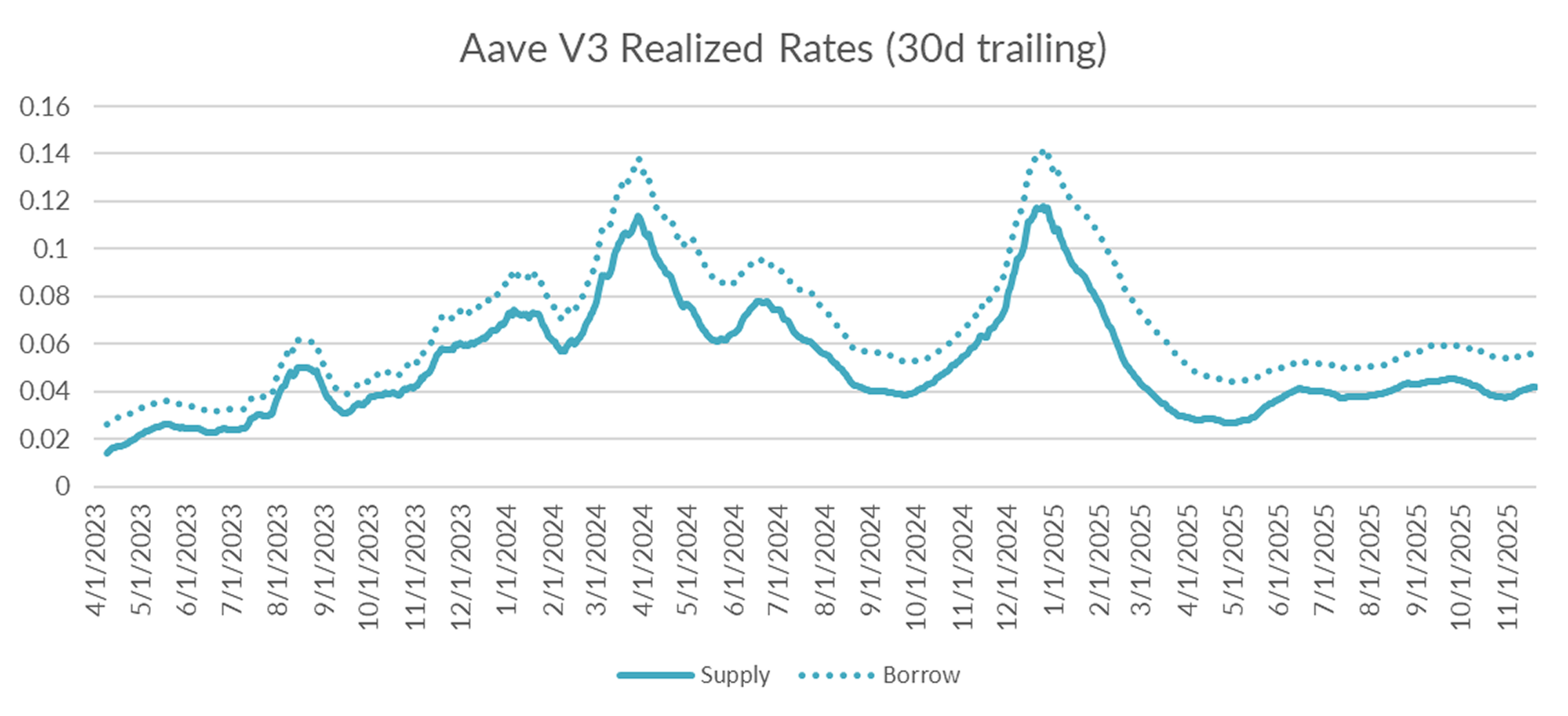

Turning now to ETH markets, ETH rates fell -10bps to 2.33% on a 30-day trailing basis over the past week. This decline was in stark contrast to the CESR staking index, which rose +1bp on the week to 2.89%.

Internal market microstructure shows that utilization remained low with little to no pickup in demand to absorb the +489K of ETH deposited the week prior.

Consistent with this picture, no sign of liquidity stress can be found in intraday charts.

Overall, absent a change in utilization over the next few weeks it may be time for a reset in the ETH kink-rate on Aave.

The market extended its slide this past week, with BTC closing below its 52 moving average. BTC and ETH fell -10.23% and -1082% this week, respectively, and both are now down double-digits year-to-date. While there appears to be some support at current levels, any pop in the near term is likely just a dead-cat bounce.