.png)

Volumes continue to be light this week as deleveraging continues in DeFi lending markets. On the stablecoin side, only blue-chip collateral markets cleared this week as lenders pulled back on providing liquidity to facilitate levered looping of exotic collateral. On the ETH side, high-yield farming positions were repaid, in some cases ahead of schedule.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

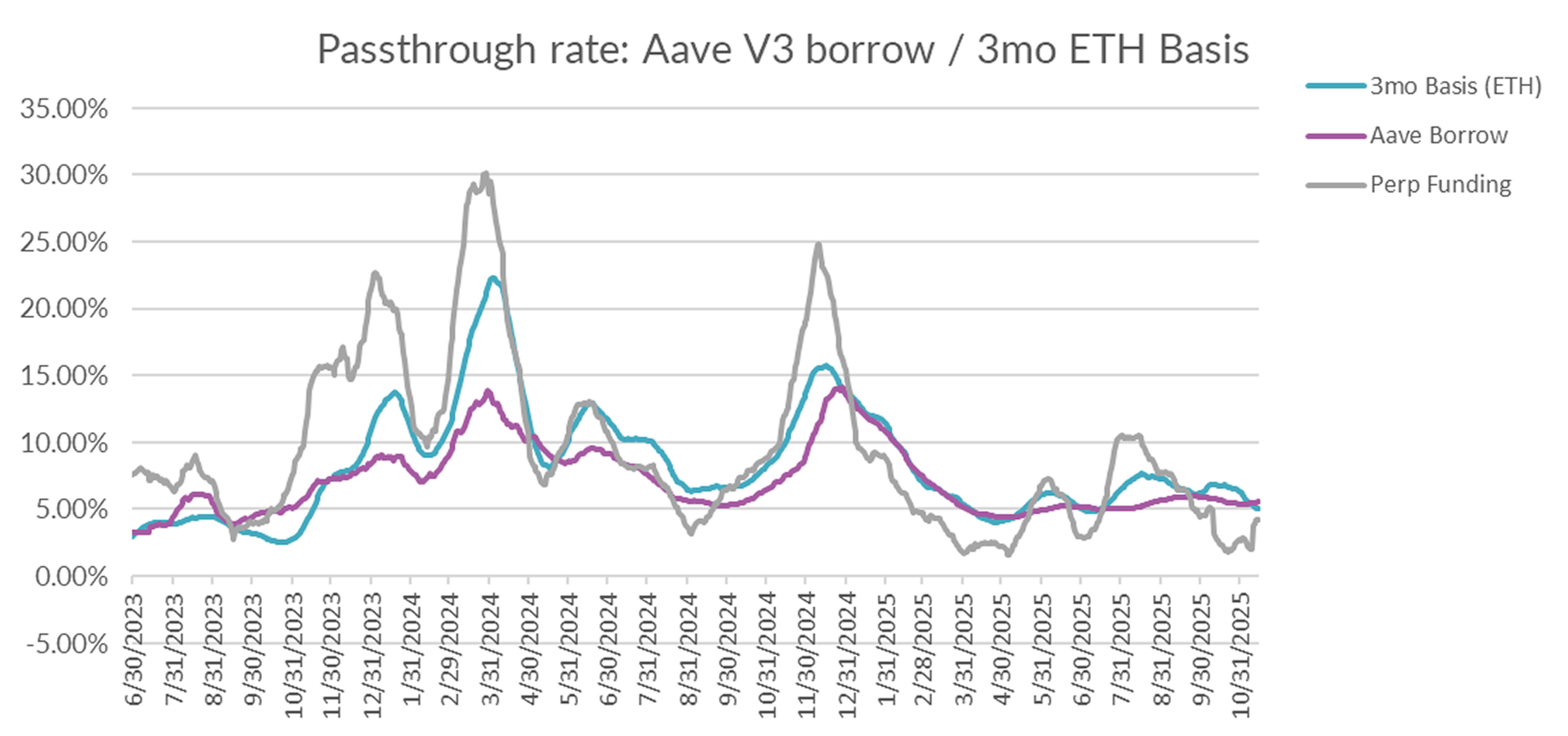

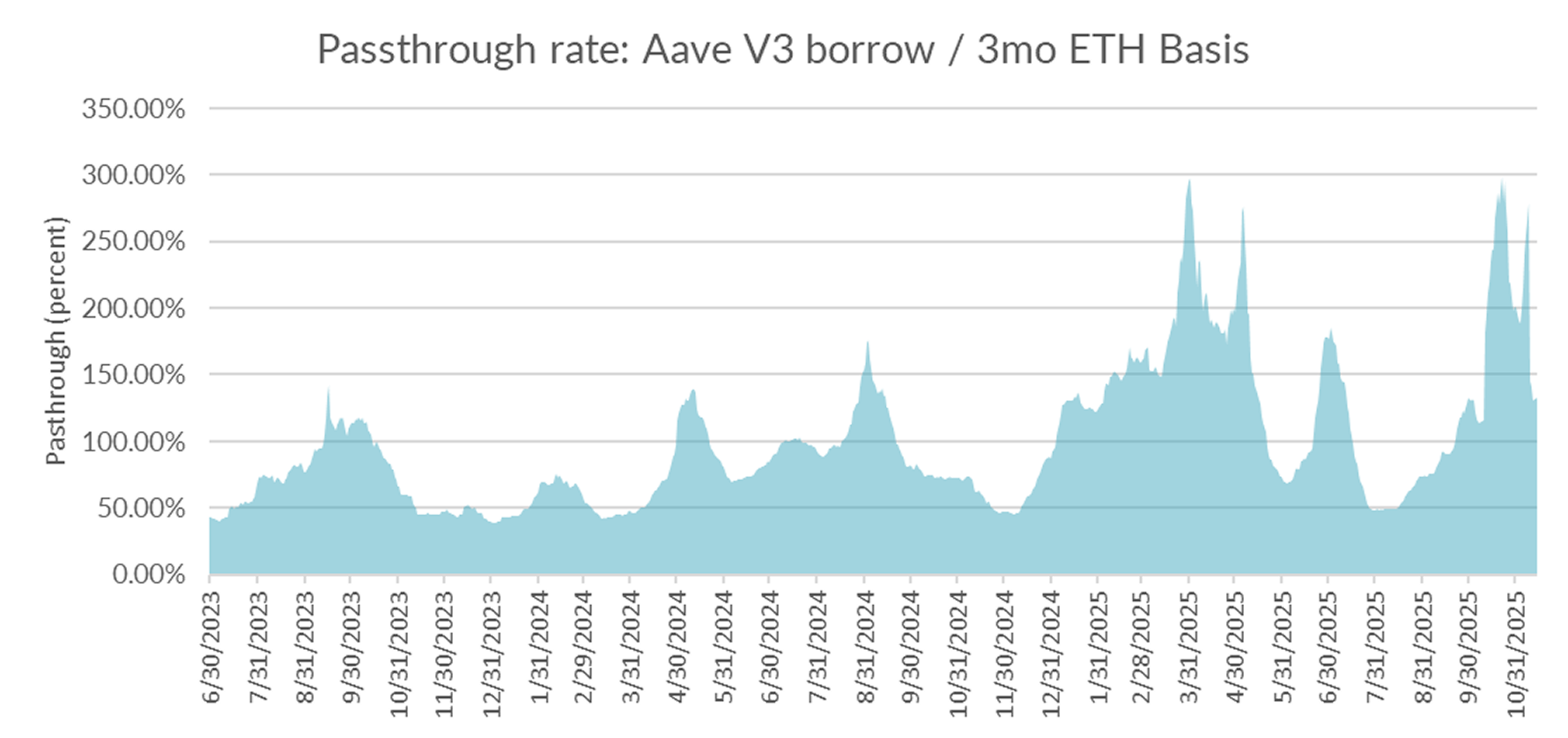

Basis and Perpetuals Markets

In derivatives markets, funding rates were mixed, with 3-month basis falling another -50bps to 5.01% and perpetual funding rates rising by +200bps to 4.19% on a 30-day trailing basis.

This reversal in perp funding rates normalized the spread between DeFi and CeFi rates back toward historical averages.

This rise in perp funding was particularly surprising given the bearish nature of the week, and suggests significant short covering just before the late week break in asset prices.

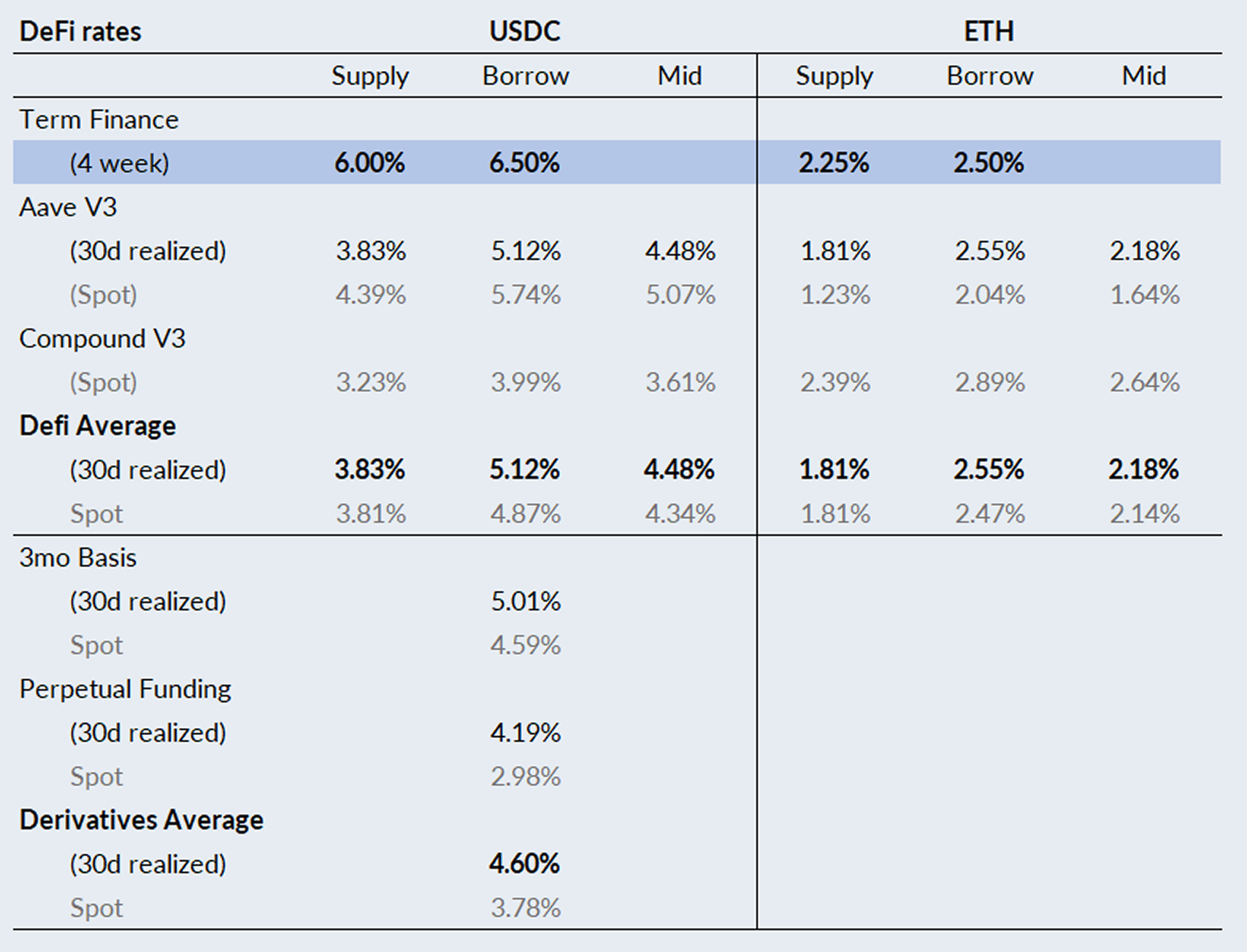

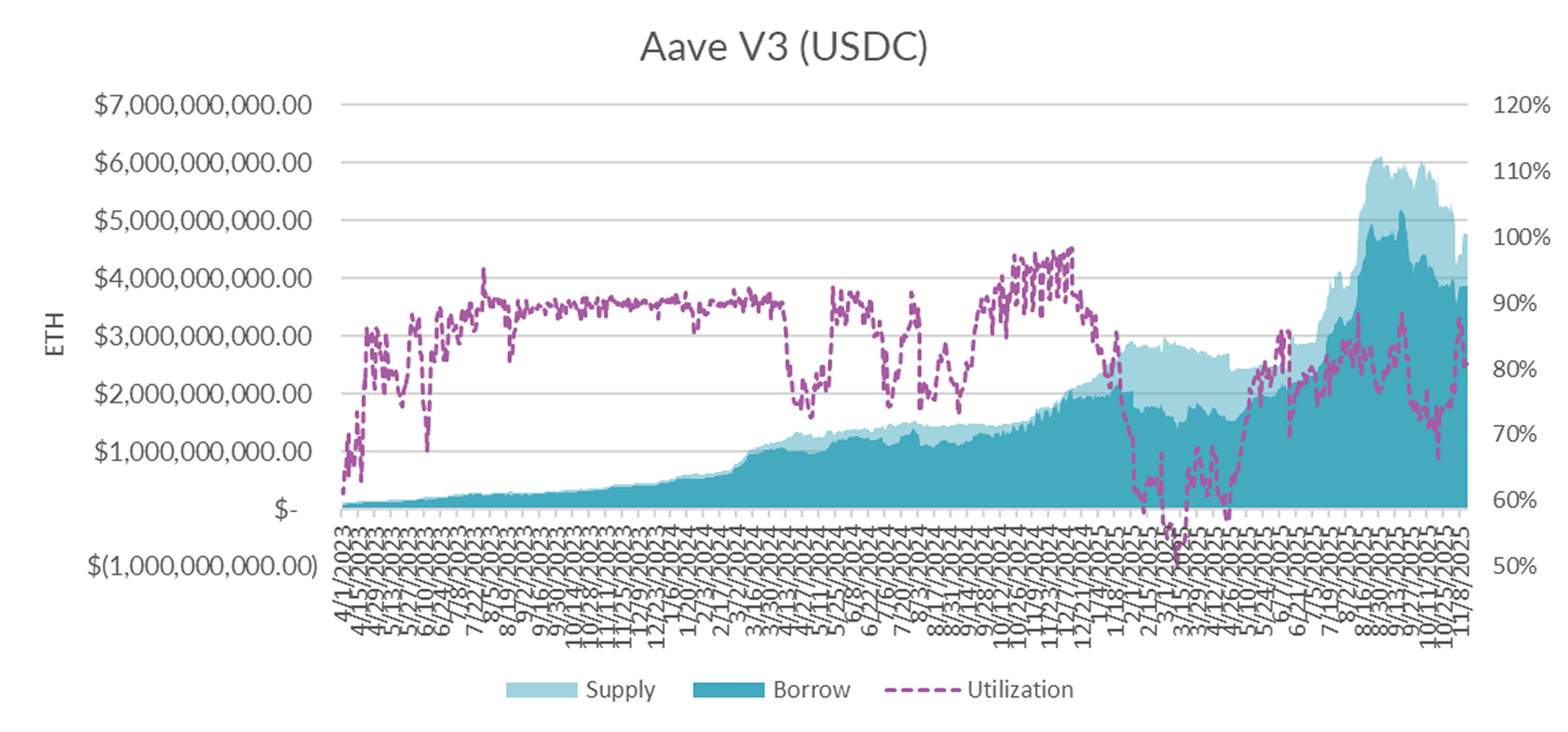

USDC Markets

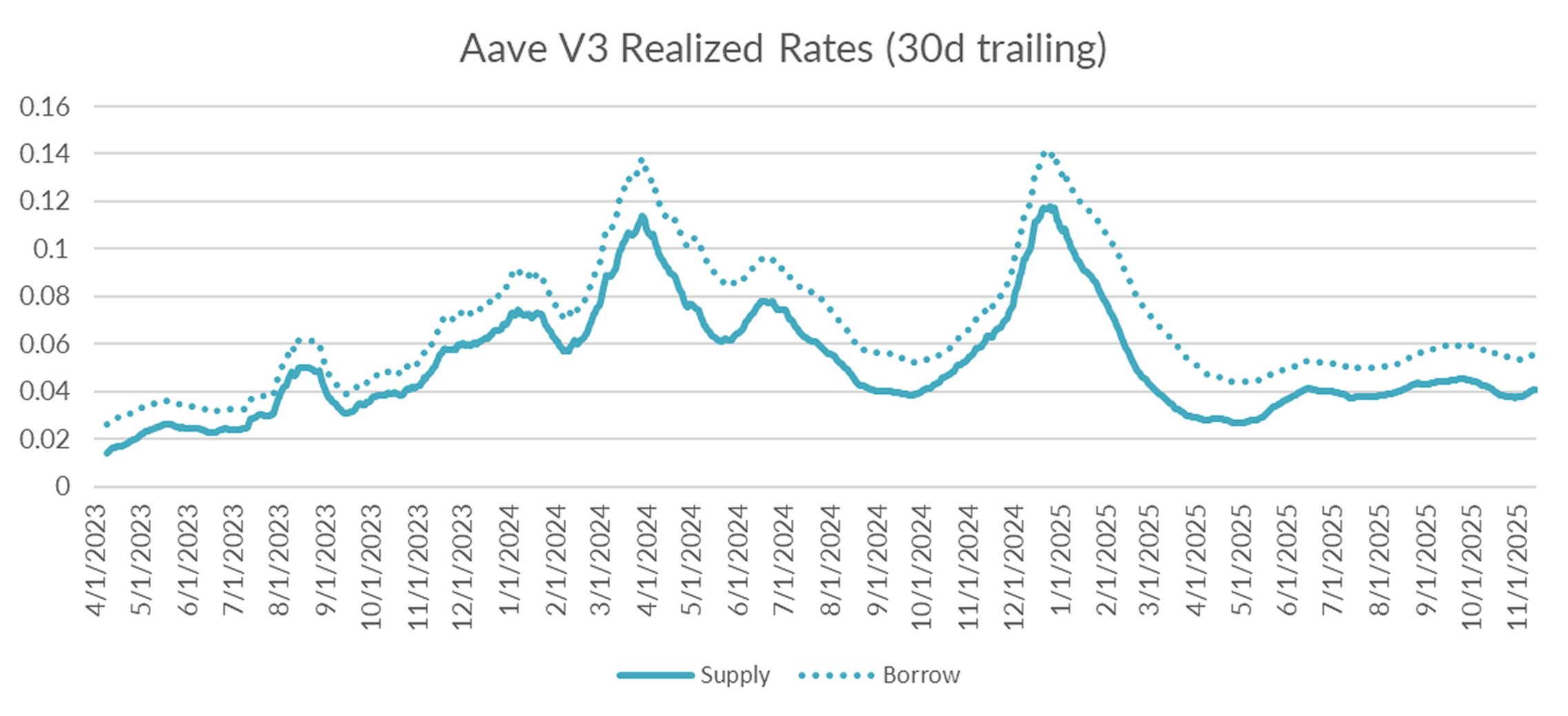

Turning to DeFi variable rate markets, the 30-day trailing average continued to rise by +11bps to 5.53% on a 30-day trailing basis. On a shorter lookback, USDC borrow rates averaged 6.05%, reflecting some residual pressure from last week’s liquidity crunch early in the week.

Diving into the microstructure of Aave's USDC markets, internal metrics show a normalization of utilization back down to 81% driven largely by deposits of +$369M over the past seven days, reversing in part the $1BN withdrawal the week prior.

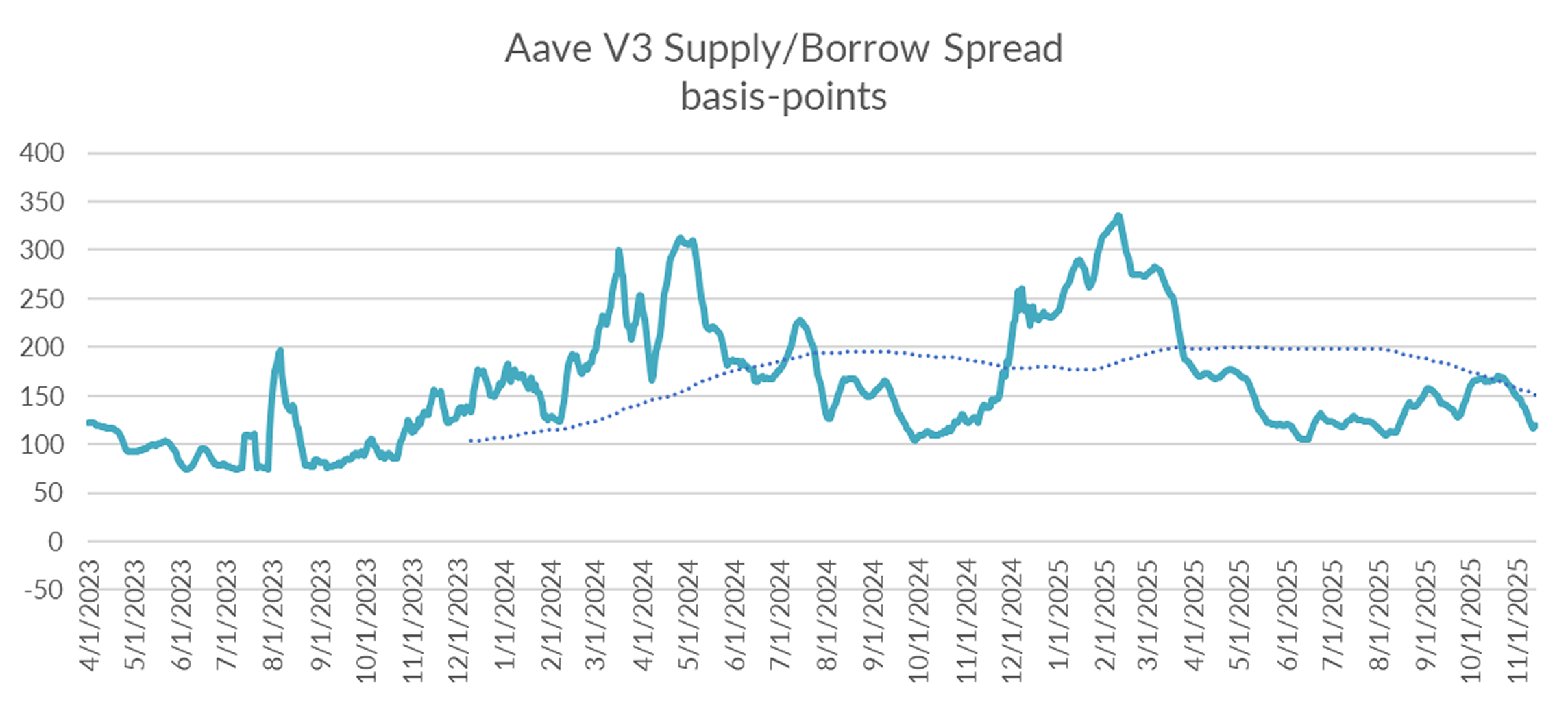

With utilization back down to 81%, expect the supply/borrow spread to rise back toward historical averages of +150%.

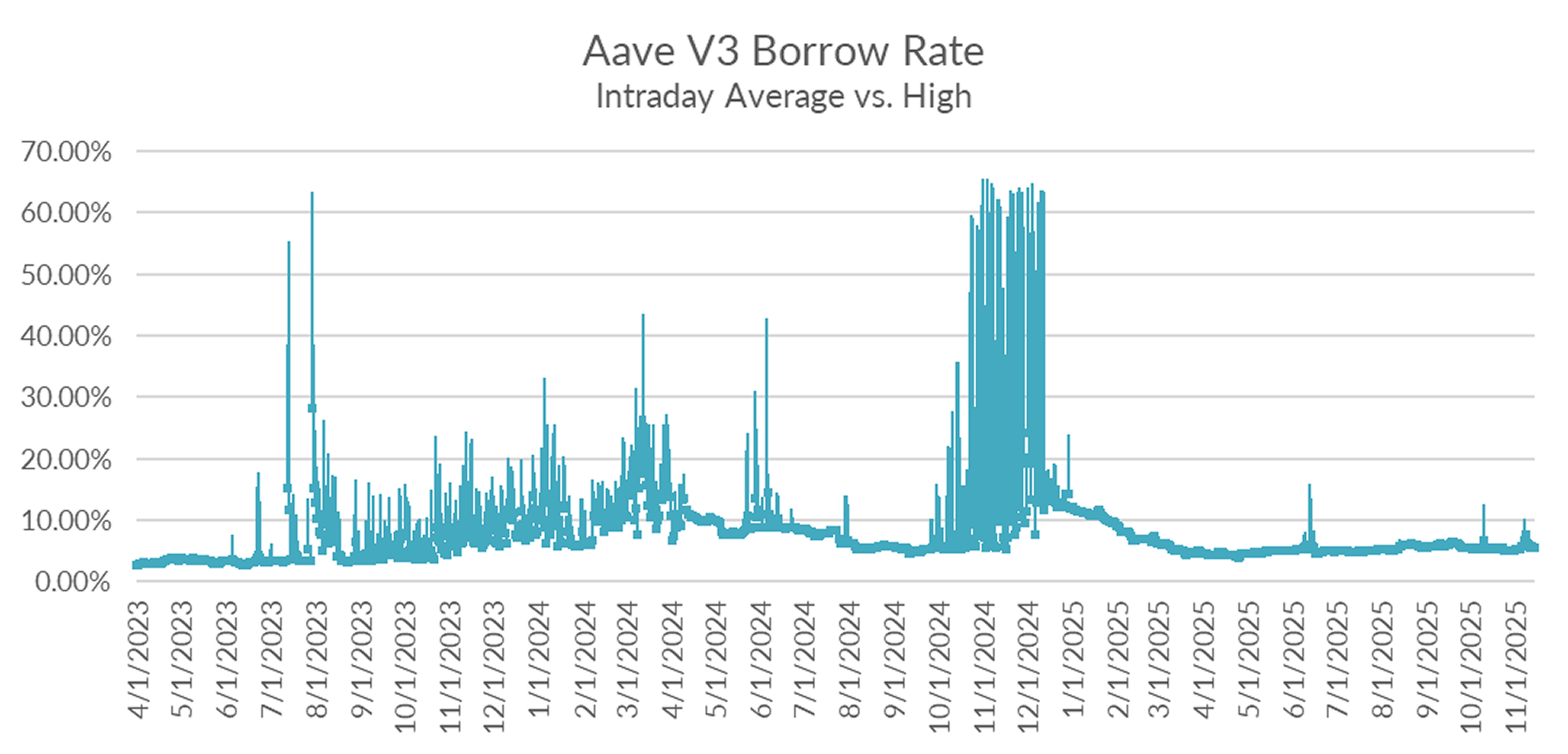

A glimpse into intraday rate dynamics show that the market has largely normalized with no signs of any intraday squeeze over the past week.

n the near term, the path for rates is highly uncertain. Falling asset prices are likely to trigger deleveraging—whether through forced liquidations or voluntary risk reduction—while lender skittishness continues to pull in the opposite direction. In the short run, rate conditions remain delicately balanced; sustained clarity will only emerge once deleveraging pressures and lender risk appetite converge toward a new equilibrium.

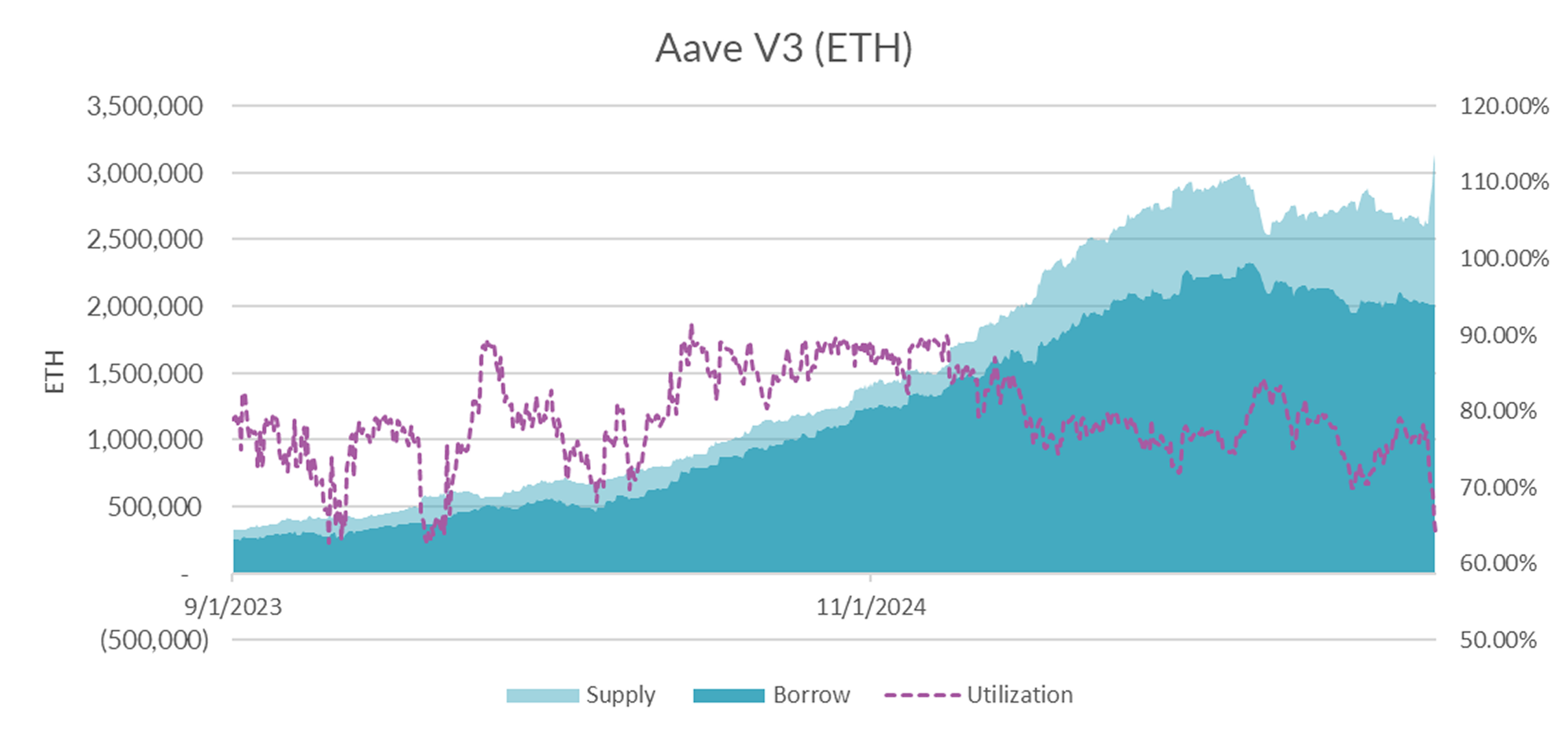

ETH Markets

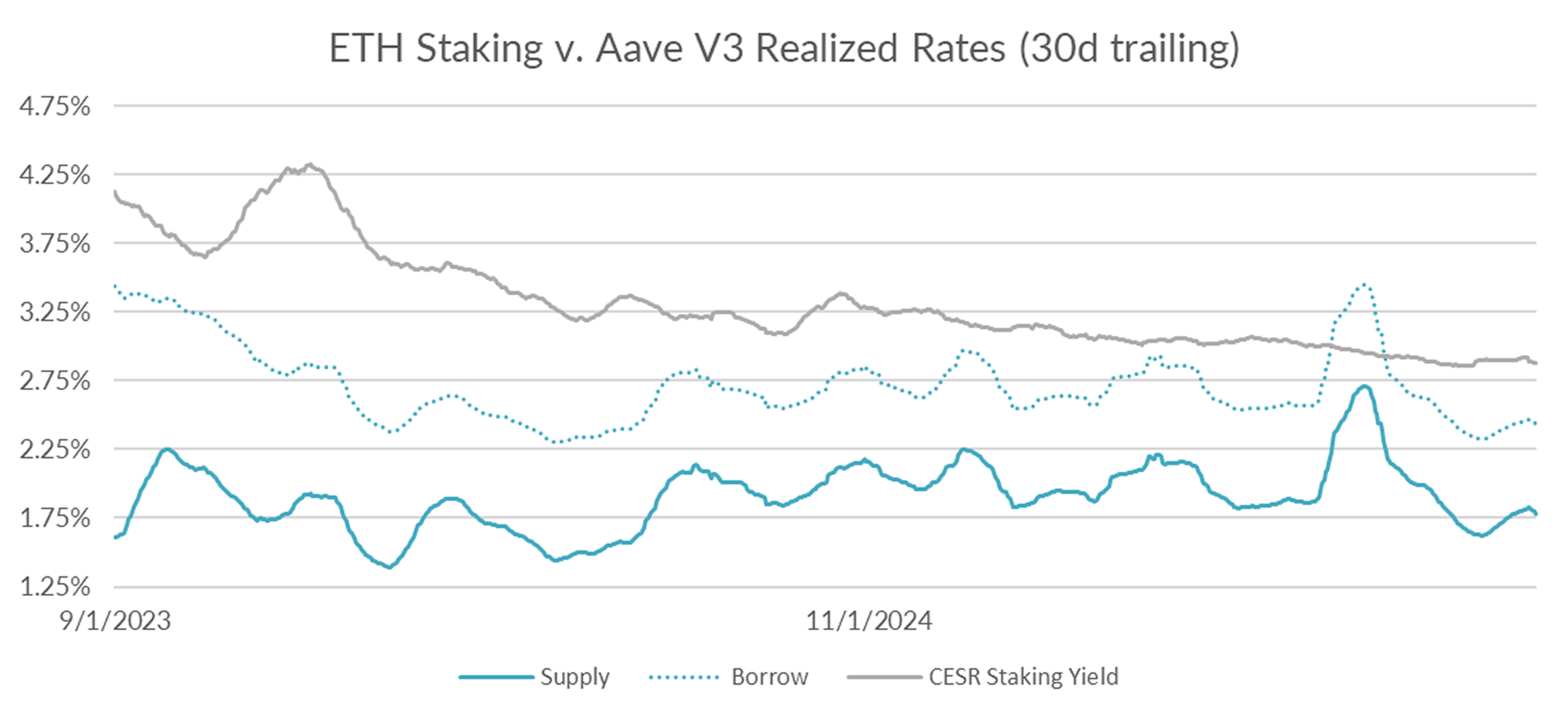

Turning now to ETH markets, ETH rates fell -2bps to 2.43% on a 30-day trailing basis over the past week. Likewise, the CESR staking index fell -3bps on the week to close at 2.88% consistent with DeFi lending markets.

Internal market microstructure shows that utilization dropped significantly, with +489K of ETH deposited over the past seven days, taking total supplied to all time highs.

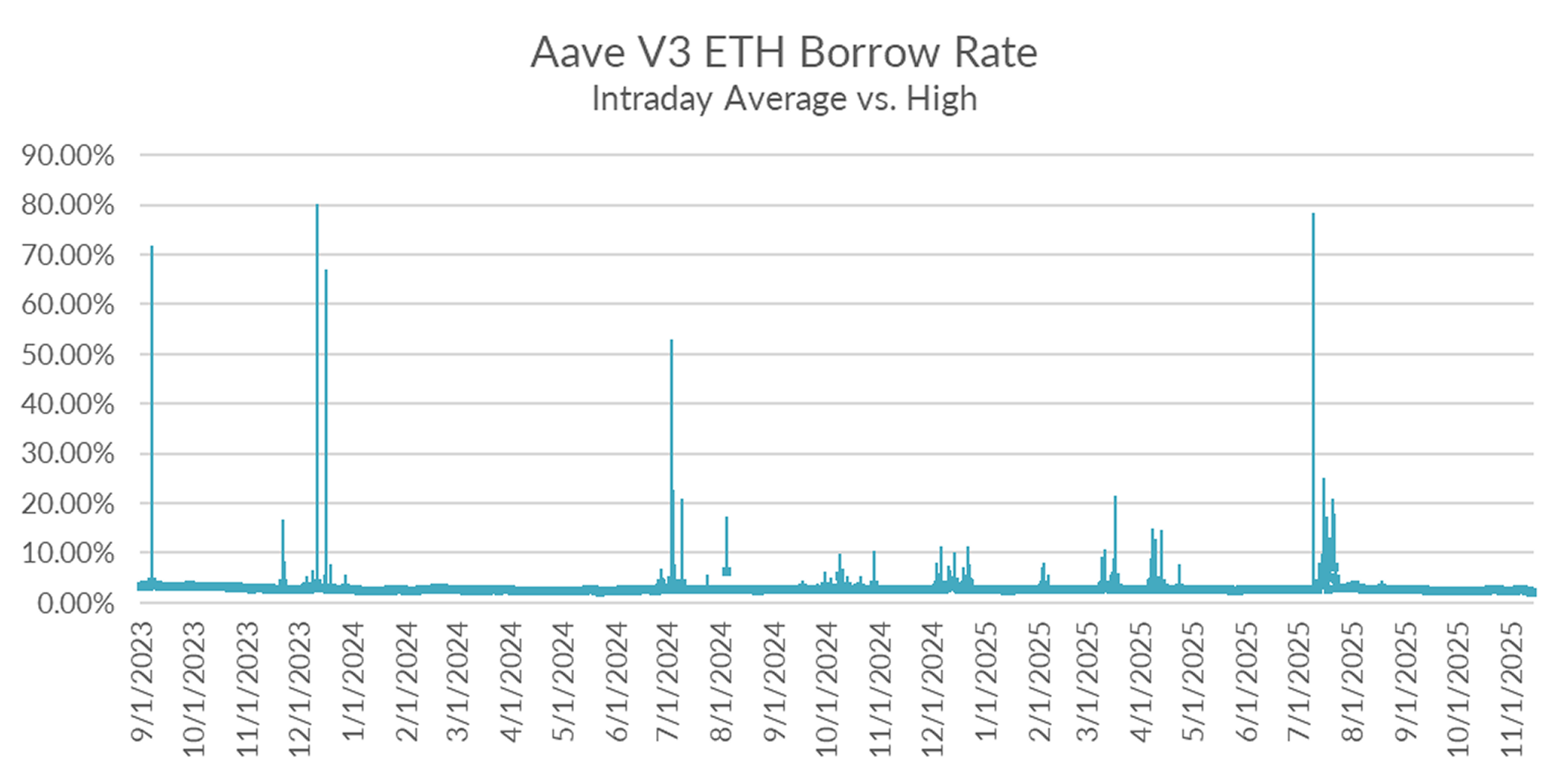

Consistent with this picture, no sign of liquidity stress can be found in intraday charts.

Overall, the sharp rise in ETH supply is suggestive of portfolio rebalancing either to top up loans against liquidation, rotation away from riskier ETH farming opportunities or both.

The market has turned decisively bearish, with BTC sliding back below 100k. BTC and ETH fell -7.83% and -7.5% this week, compounding last week’s declines of -5.5% and -9.94%. Year-to-date, BTC is barely positive at +1.93%, while ETH is now down -4.83%. Expect borrow demand to remain weak in the near term.