Stablecoin lending markets experienced a flight to safety following the insolvency of the Stream Protocol, which came to light amid concerns over excessive leverage and self-dealing.

On-chain analysis and the subsequent fallout revealed extensive backroom arrangements and circular TVL flows across multiple protocols, creating significant ripple effects. Fears of contagion—and echoes of 2022—prompted widespread liquidity withdrawals across lending platforms, particularly those backed by exotic assets.

These mass redemptions underscored a fundamental weakness of open-ended, variable-rate lending: liquidity is available on demand—until it’s not. In the absence of defined maturity dates, lenders that failed to withdraw early may at best endure extended illiquidity and at worst suffer losses from borrower defaults.

Term was fortunate to avoid any bad debt during the past week. No Term loans were collateralized by Stream or Elixir assets. The fixed-term structure of Term loans also ensures that the liquidity profile of depositors remains clearly defined.

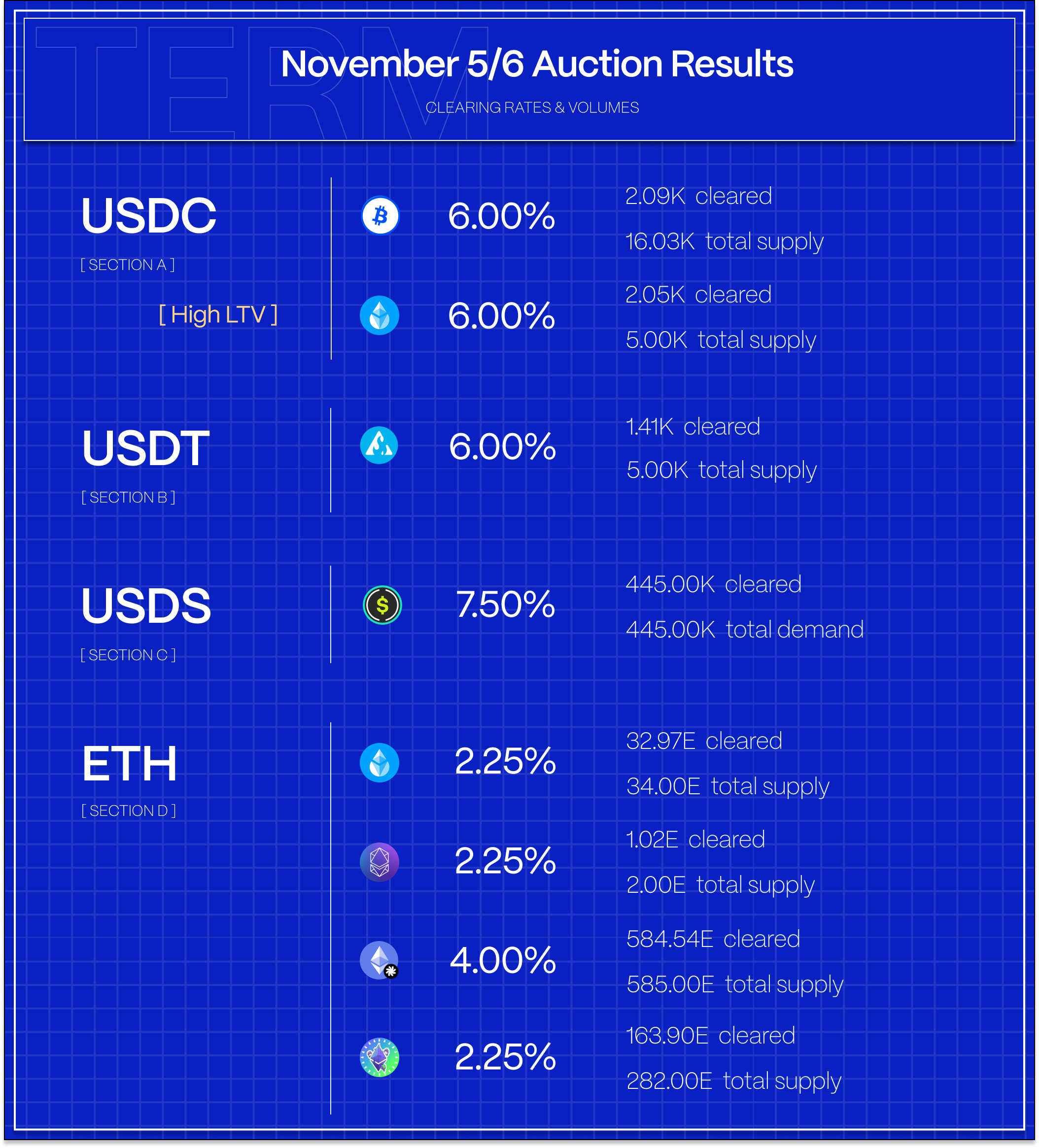

On the auction side, borrow demand dried up consistent with stablecoin borrow demand across all of DeFi as participants shored up risk. Borrow demand on the ETH side, on the other hand, remained steady and consistent with recent history.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

Basis and Perpetuals Markets

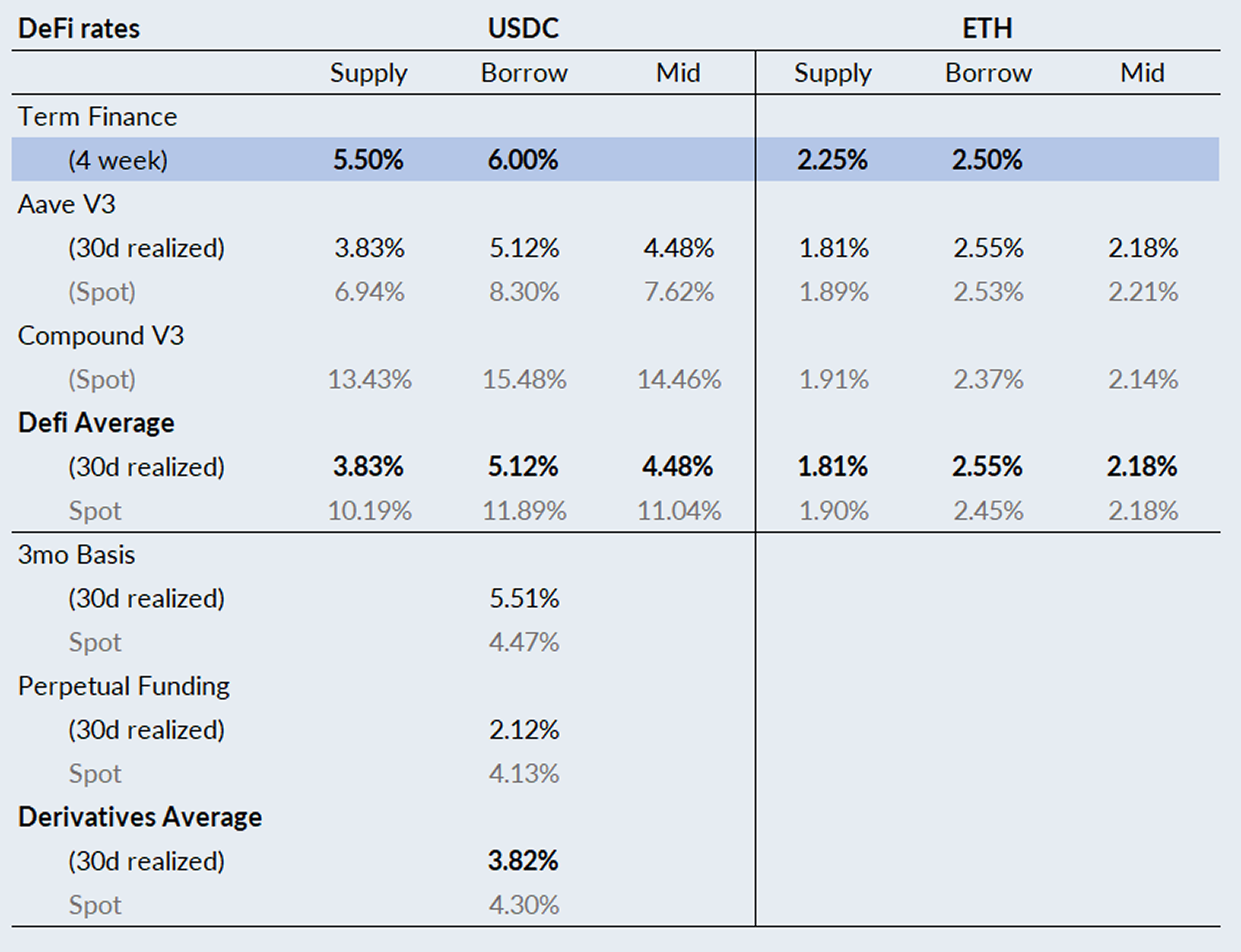

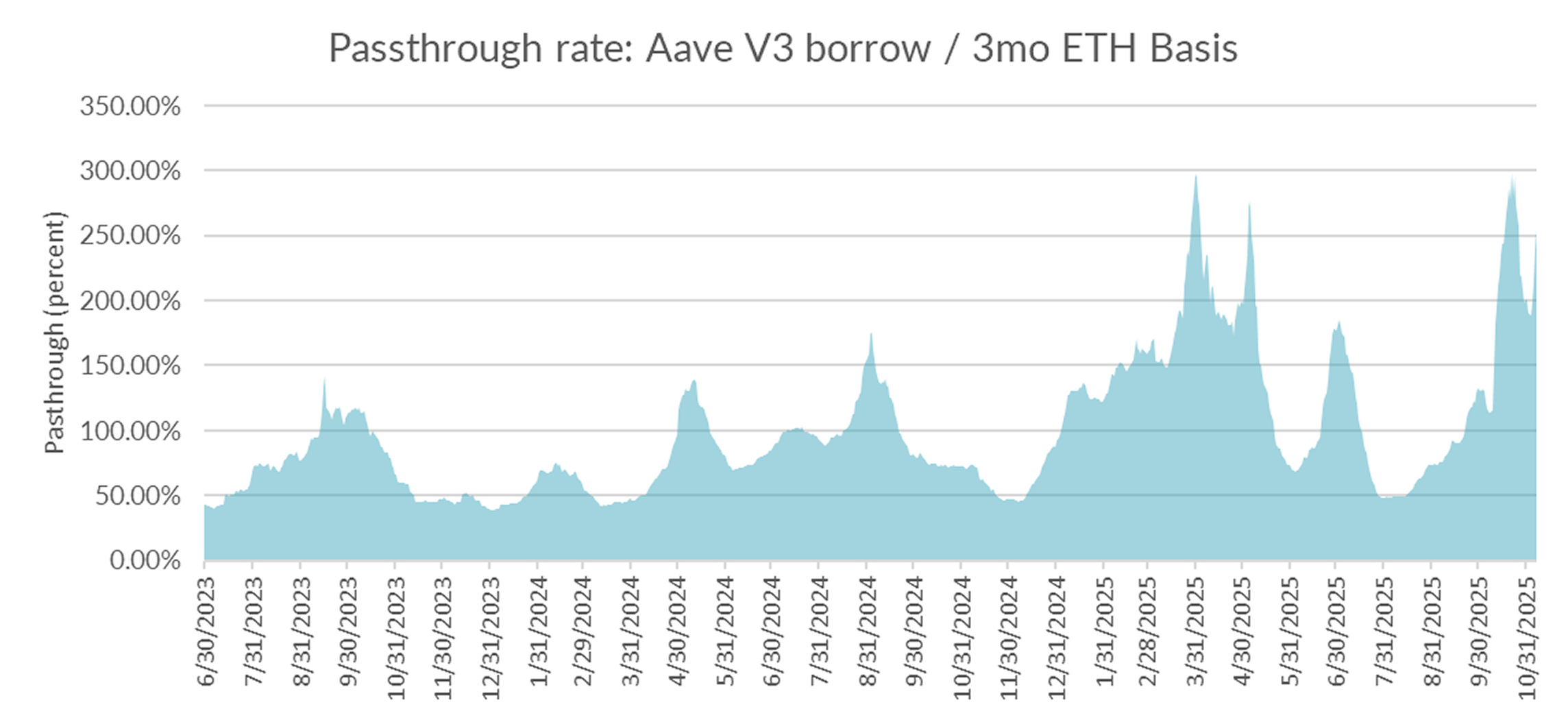

In derivatives markets, funding rates dropped precipitously, with 3-month basis falling -76bps to 5.51% and perpetual funding rates declining by -55bps to 2.12% on a 30-day trailing basis.

The continued slide in basis rates was in stark contrast to the flight to liquidity trade seen in DeFi that took DeFi rates up sharply towards the end of the week.

Overall, DeFi and derivatives markets are diverging with DeFi facing a liquidity crunch and rising rates while CeFi derivatives markets continue to slide downward.

USDC Markets

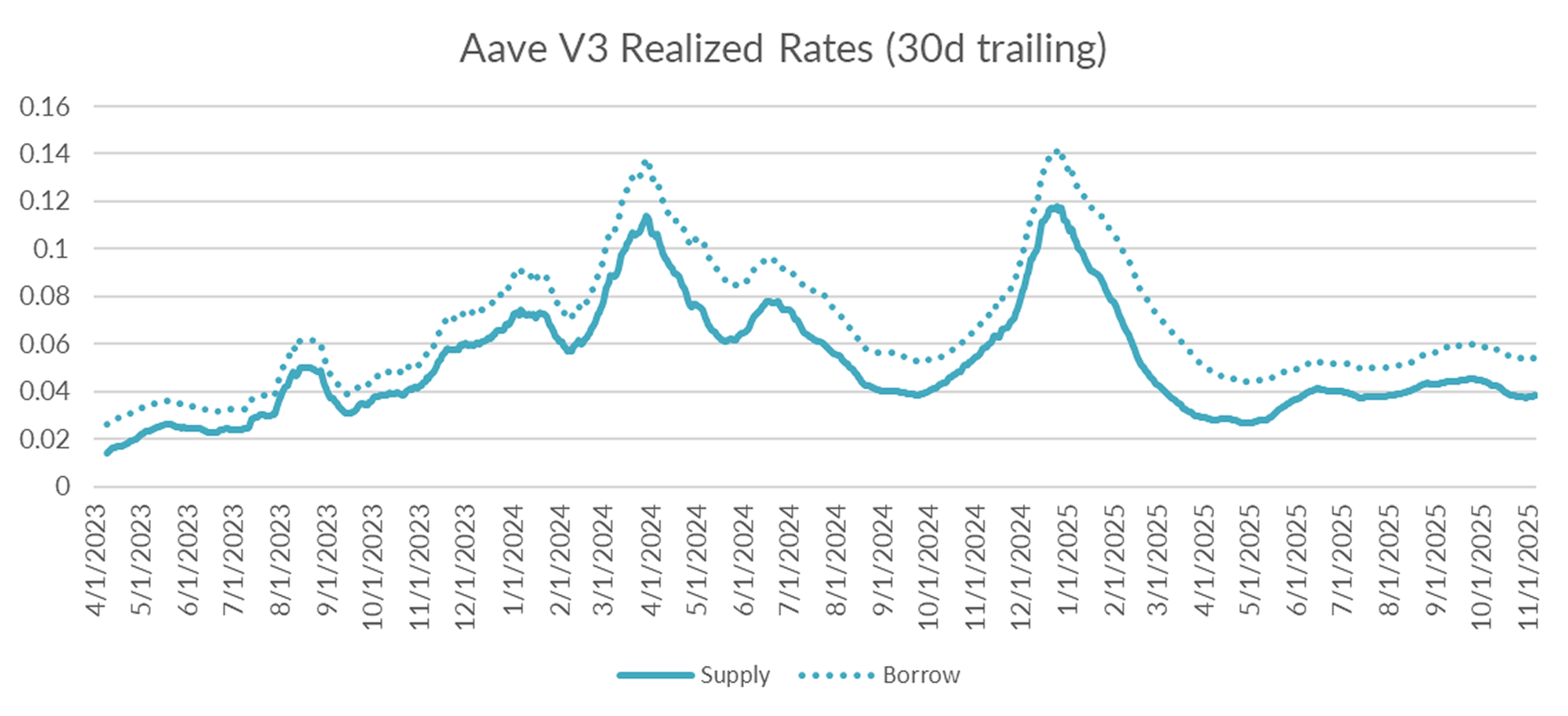

Honing in on DeFi variable rate markets, the 30-day trailing average stabilized, rising by +3bps to 5.41% on a 30-day trailing basis. On a shorter lookback period, USDC borrow rates averaged 5.58% reflecting the on-chain liquidity crunch previously mentioned above.

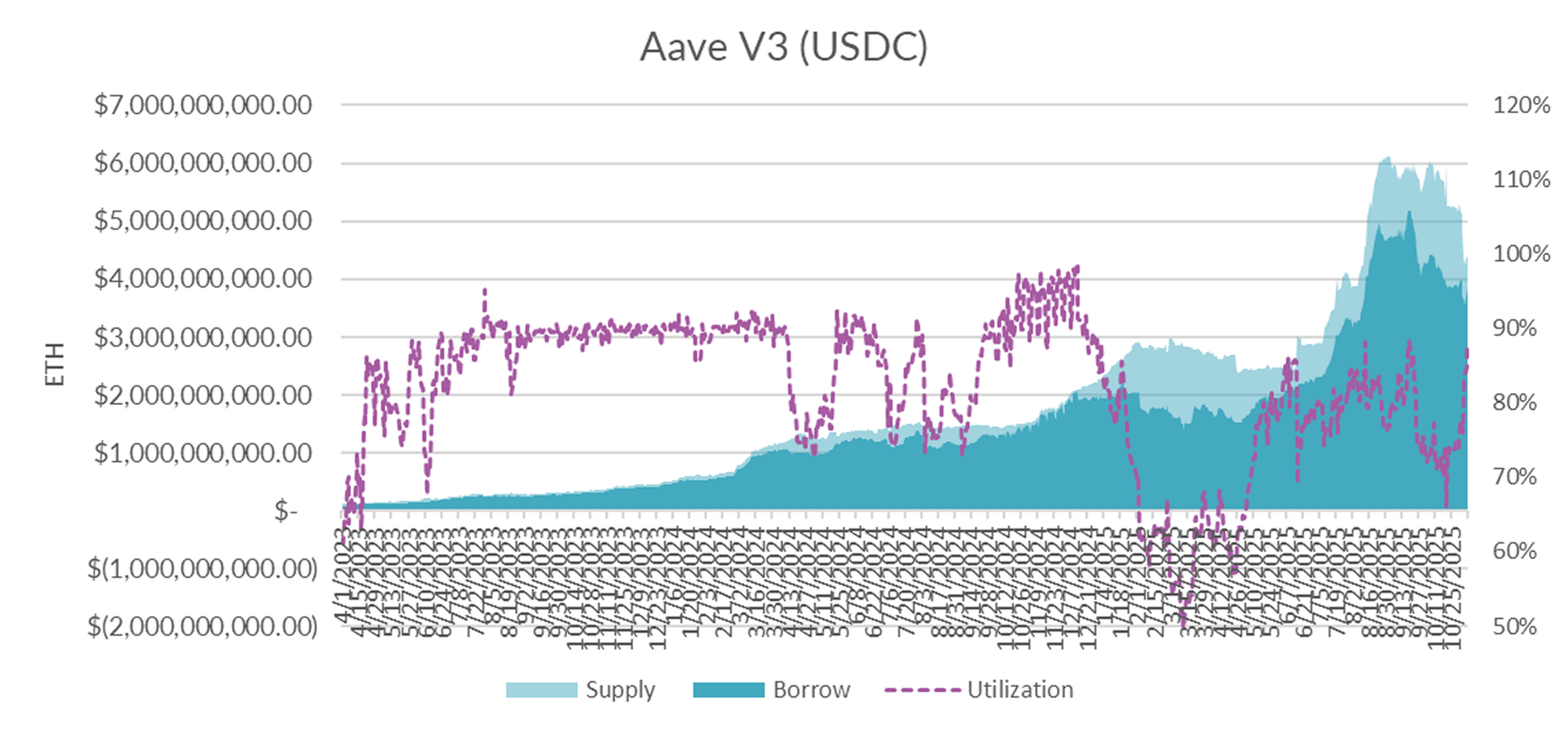

Diving into the microstructure of Aave's USDC markets, internal metrics show a sharp uptick in utilization, closing the week at 88% driven largely by large withdrawal from Aave V3. Close to -$1 billion in USDC deposits were withdrawn over the past seven days.

In line with sharpyl rising utilization rates, the spread between supply and borrow rates are beginning to decline from local highs.

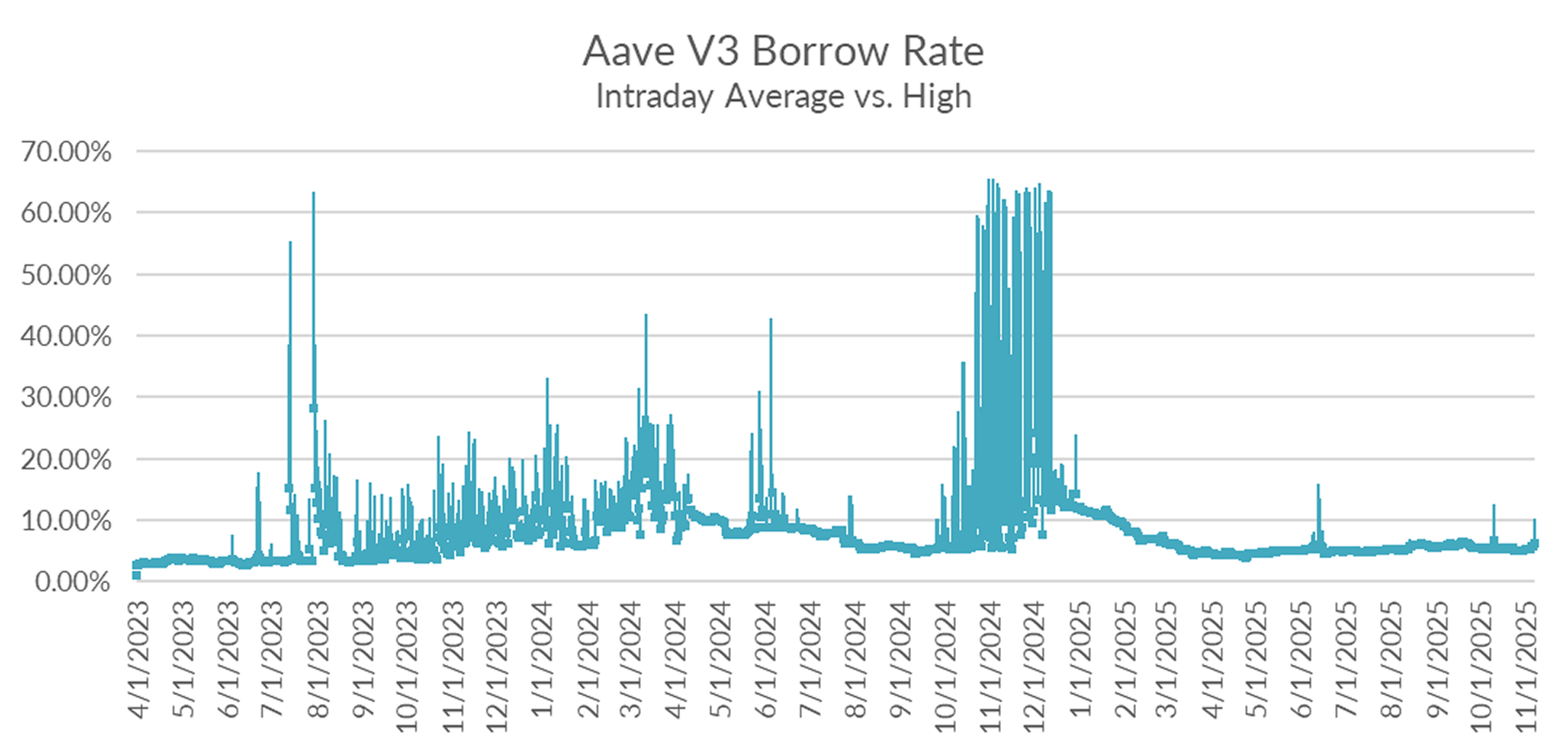

A glimpse into intraday rate dynamics show that utilization is beginning to hit the kink, with intraday rates spiking as high as 10.21% on Friday, November 6, 2025.

With the market in risk-off mode, expect liquidity to remain tight in the near and medium term.

ETH Markets

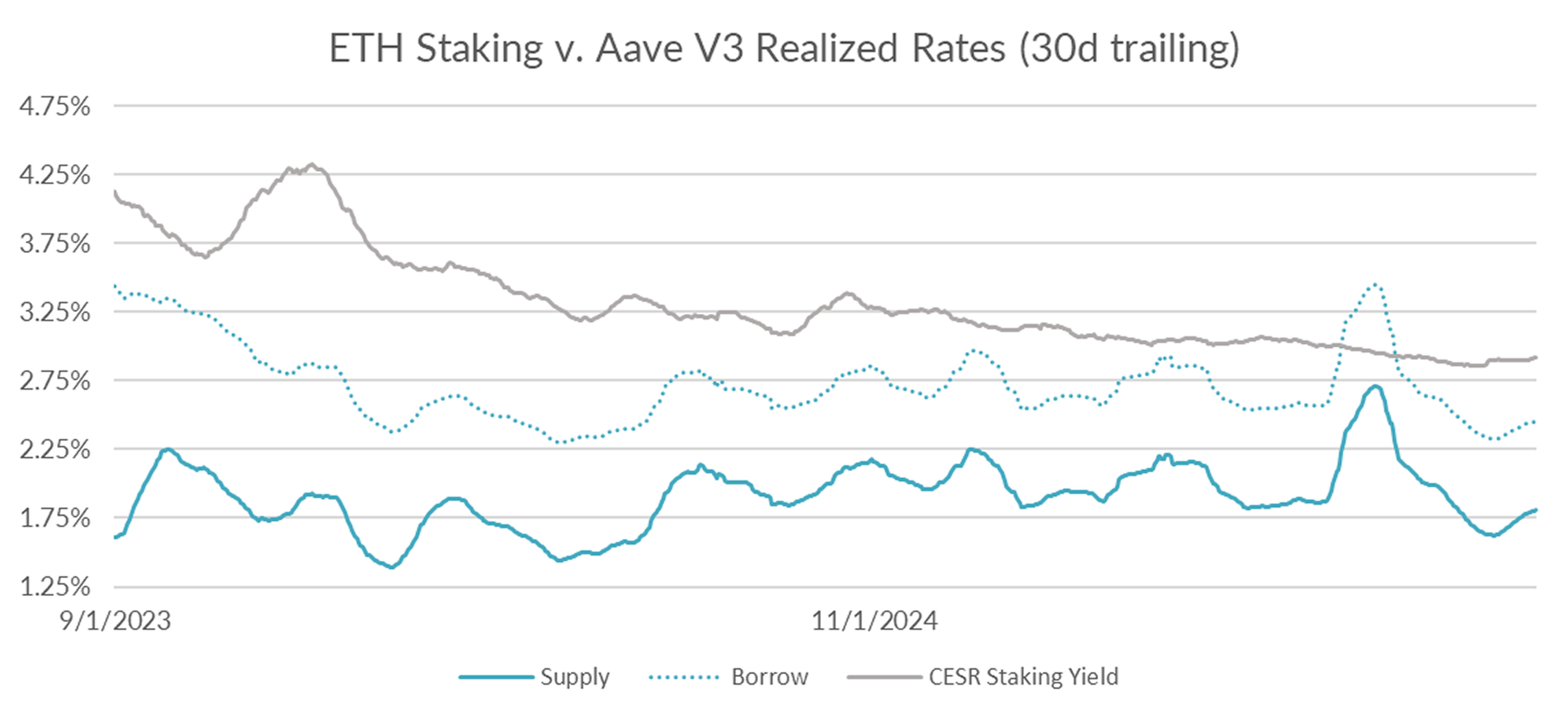

Turning now to ETH markets, ETH rates rose +3bps to 2.45% on a 30-day trailing basis over the past week. The CESR staking index, likewise rose +2bps on the week to close at 2.92% consistent with DeFi lending markets.

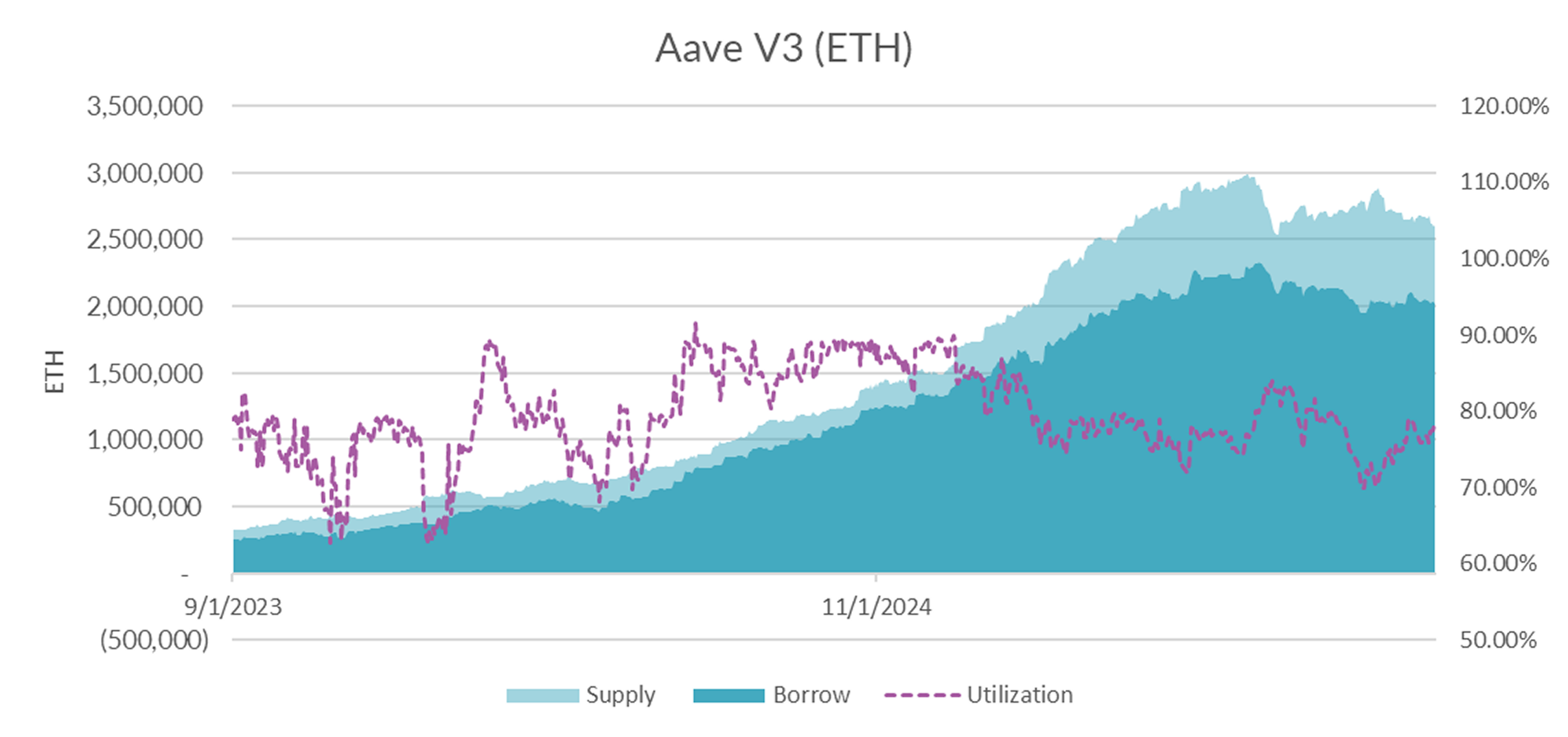

Internal market microstructure shows that supply and demand dynamics remain relatively steady and balanced, though supply (-66k ETH) did retreat slightly more than demand (-26k ETH) but not by much.

Consistent with this picture, no sign of liquidity stress can be found in intraday charts.

Overall, ETH markets remain stable and remain relatively isolated from the turmoil in stablecoin lending markets. Expect markets to remain relatively stable in the near term.

BTC and ETH close down -5.5% and -9.94% on the week, but this masks significantly deeper drawdowns intra-week that broke through significant support levels and reports of large liquidations on exchange. The fact that this occurred despite no obvious catalyst is a warning sign that this bull market is getting long in the tooth. Indeed, languishing derivatives rates indicates that there is little to no long-interest amongst fast money traders. While its hard to say whether this is merely a correction or a major inflection point, odds are that stablecoin lending markets will remain tepid in the near and medium term.