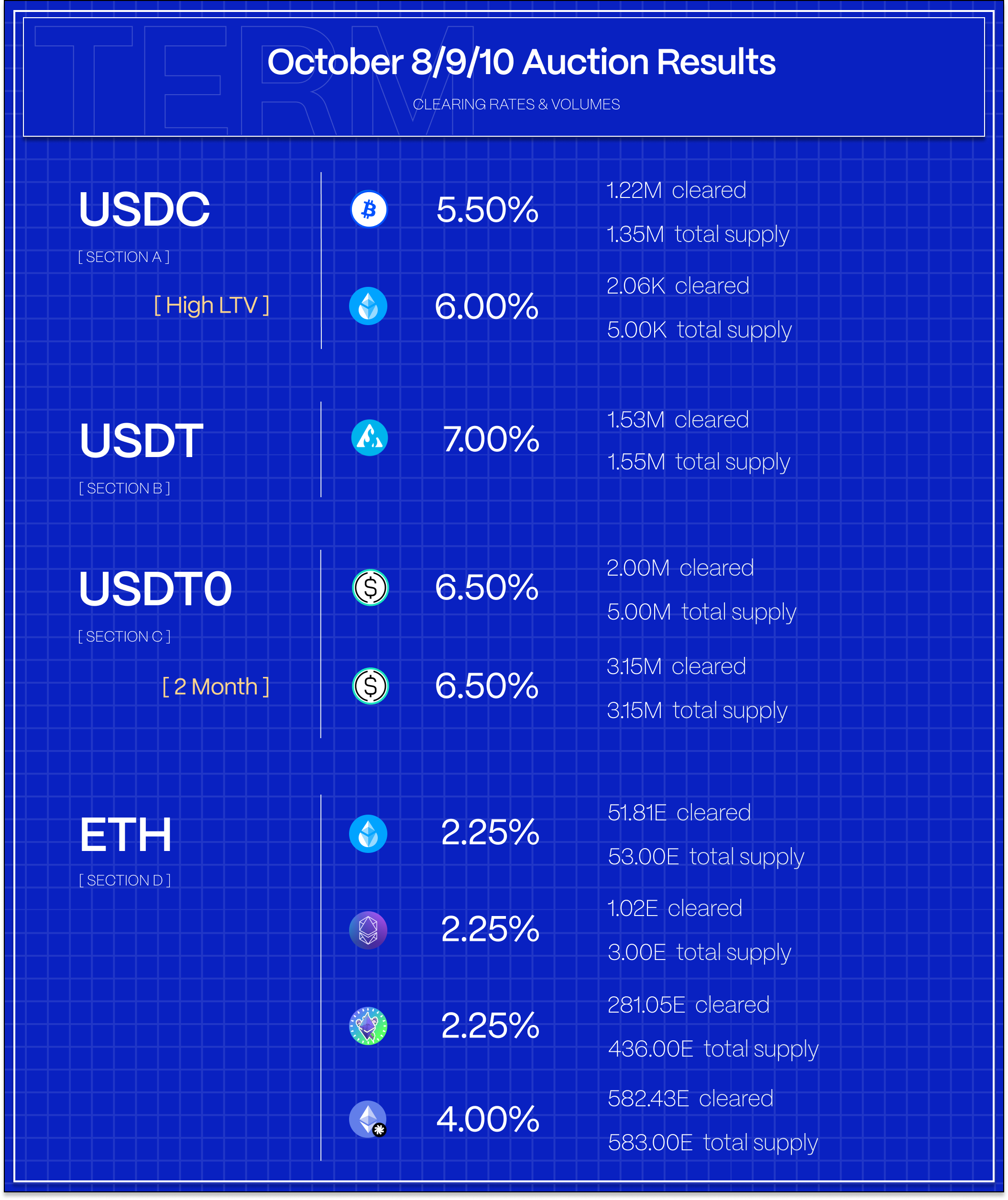

Term cleared ~11M in stablecoin loans and over 900 ETH this week — a record for Term. On the stablecoin side, Term cleared over 8M against PT-sUSDE on Plasma with the remainder split between Mainnet and Avalanche against blue-chip collateral. On the ETH side, a sizeable chunk of superETH loans rolled at 4.00% offering strong risk-adjusted APRs in excess of the ETH staking rate.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

Basis and Perpetuals Markets

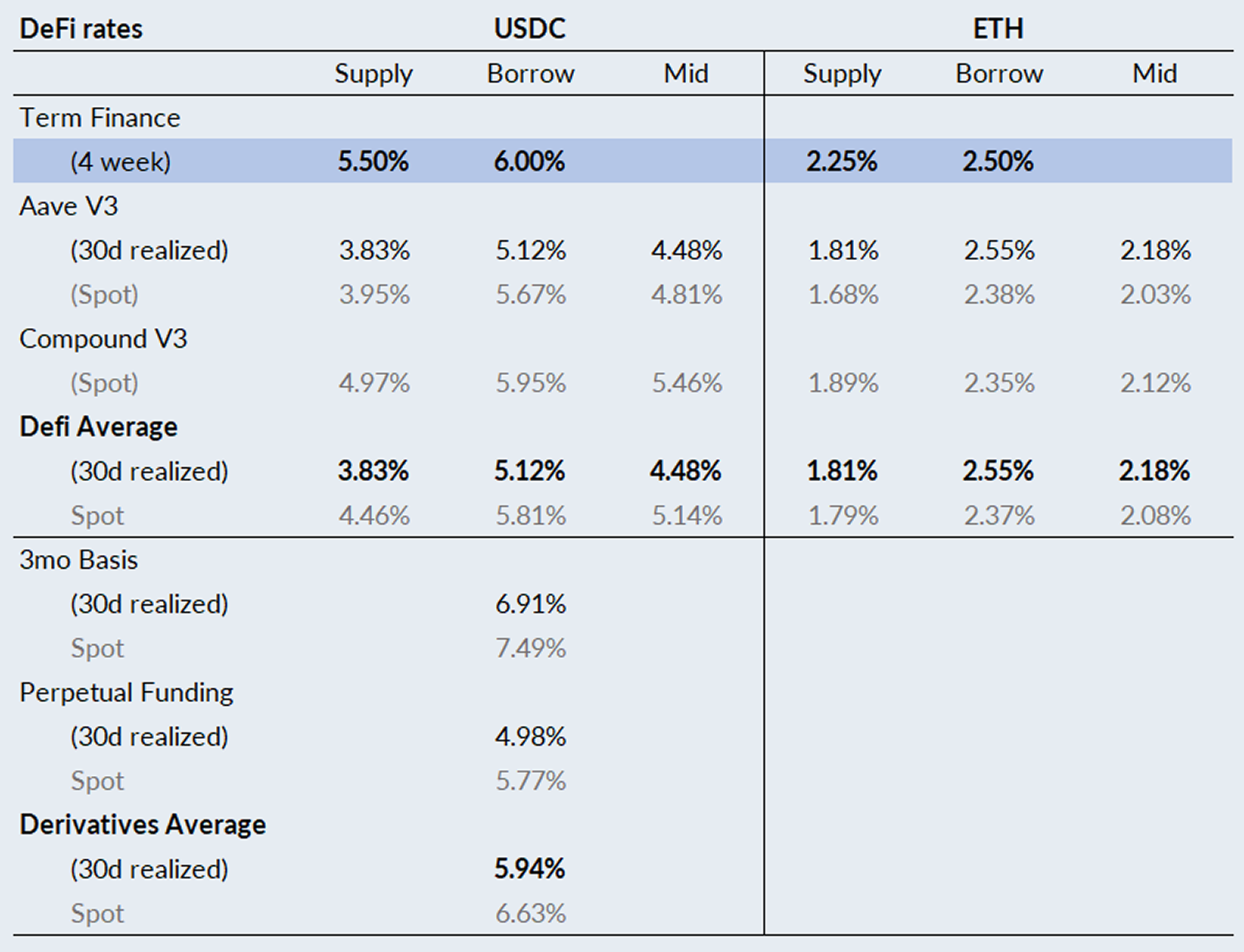

In derivatives markets, funding rates bounced back from the previous two week decline, with 3-month basis rising +57bps to 6.91% and perpetual funding rates up +50bps to 4.98% on a 30-day trailing basis.

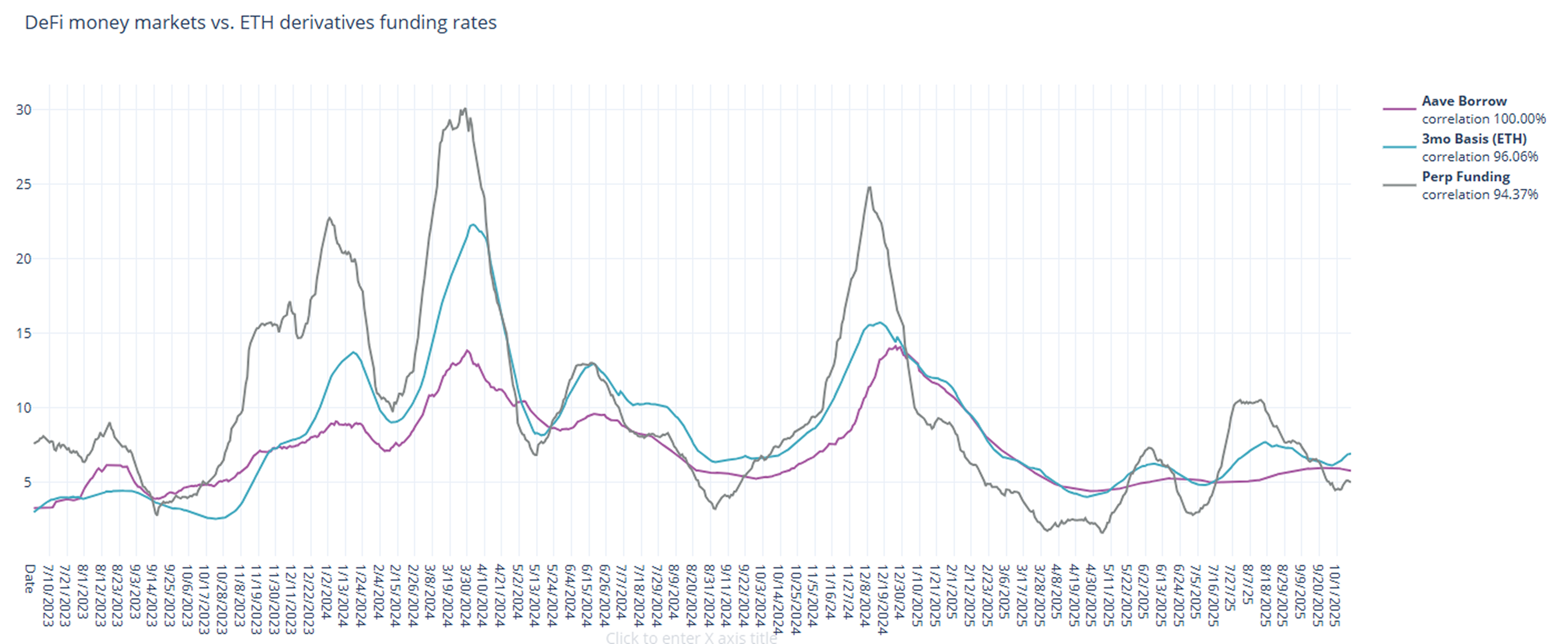

With derivatives funding rates on the mend, the ratio between DeFi and derivatives funding holds steady near historical averages.

Despite this week’s positive price action, crypto and risk assets close the week down on late week headlines of rising trade tensions between the Trump administration and China. These developments are negative for crypto and funding rates in the near term.

USDC Markets

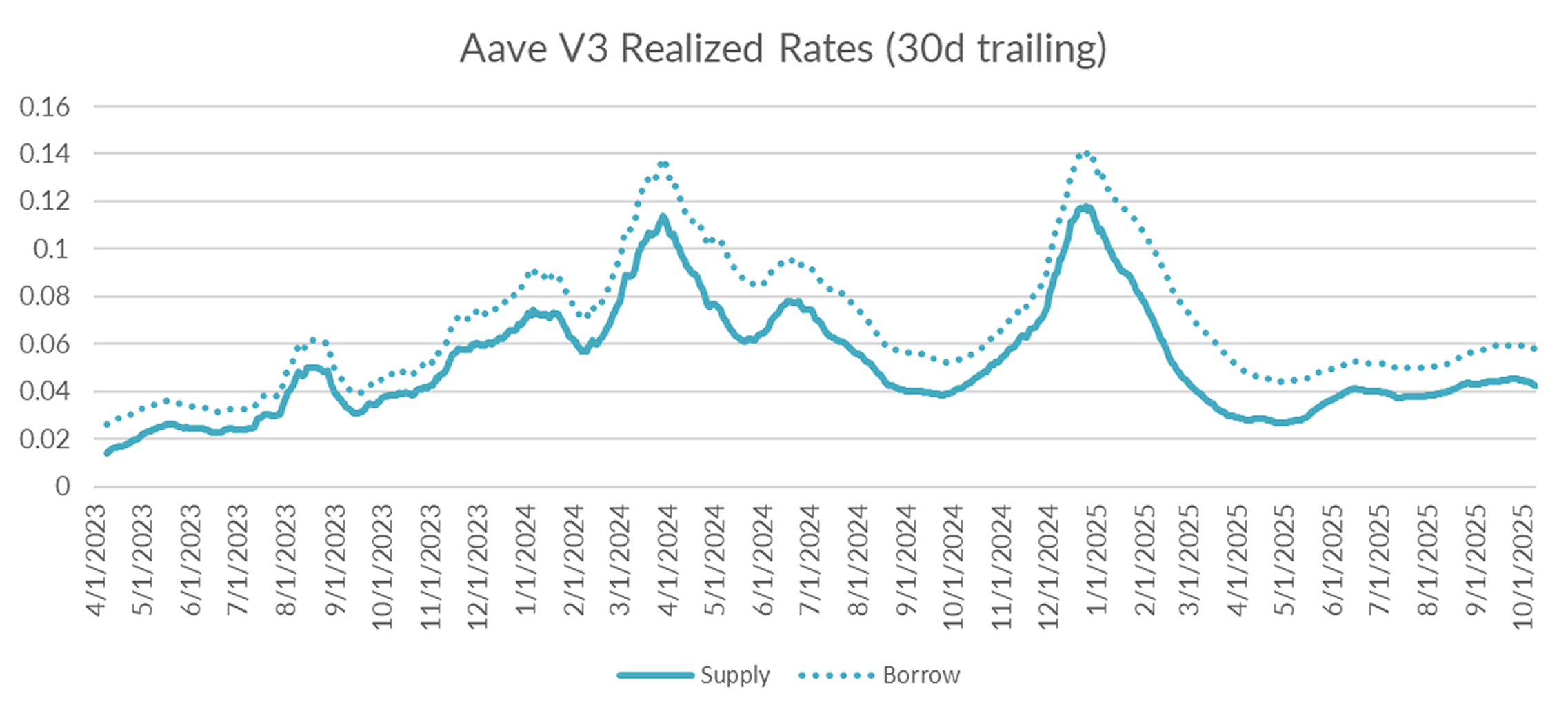

Turning to DeFi variable rate markets, the 30-day trailing average fell -14bps to 5.76% on a 30-day trailing basis. On a shorter lookback period, USDC borrow rates averaged just 5.42% suggesting further declines ahead.

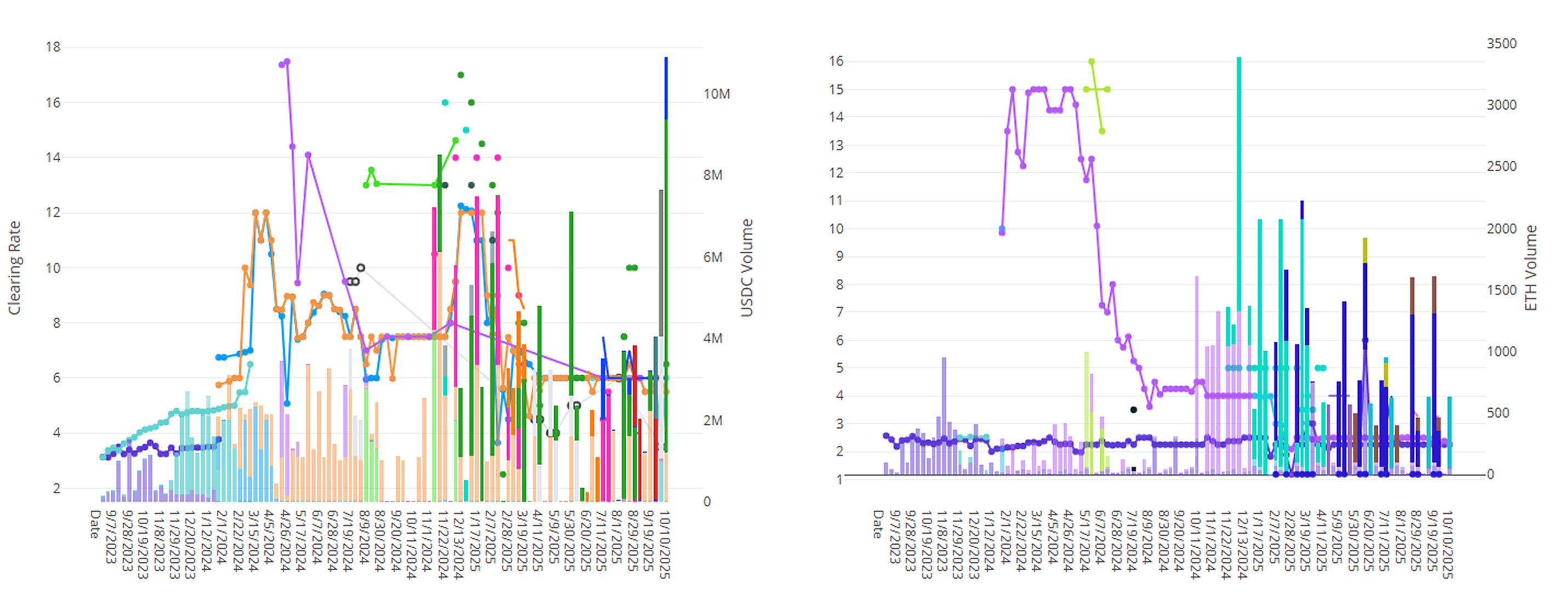

Diving into the microstructure of Aave's USDC markets, USDC supply rose +56M while borrows rose by +190M over the same period, keeping utilization steady in the mid 70s.

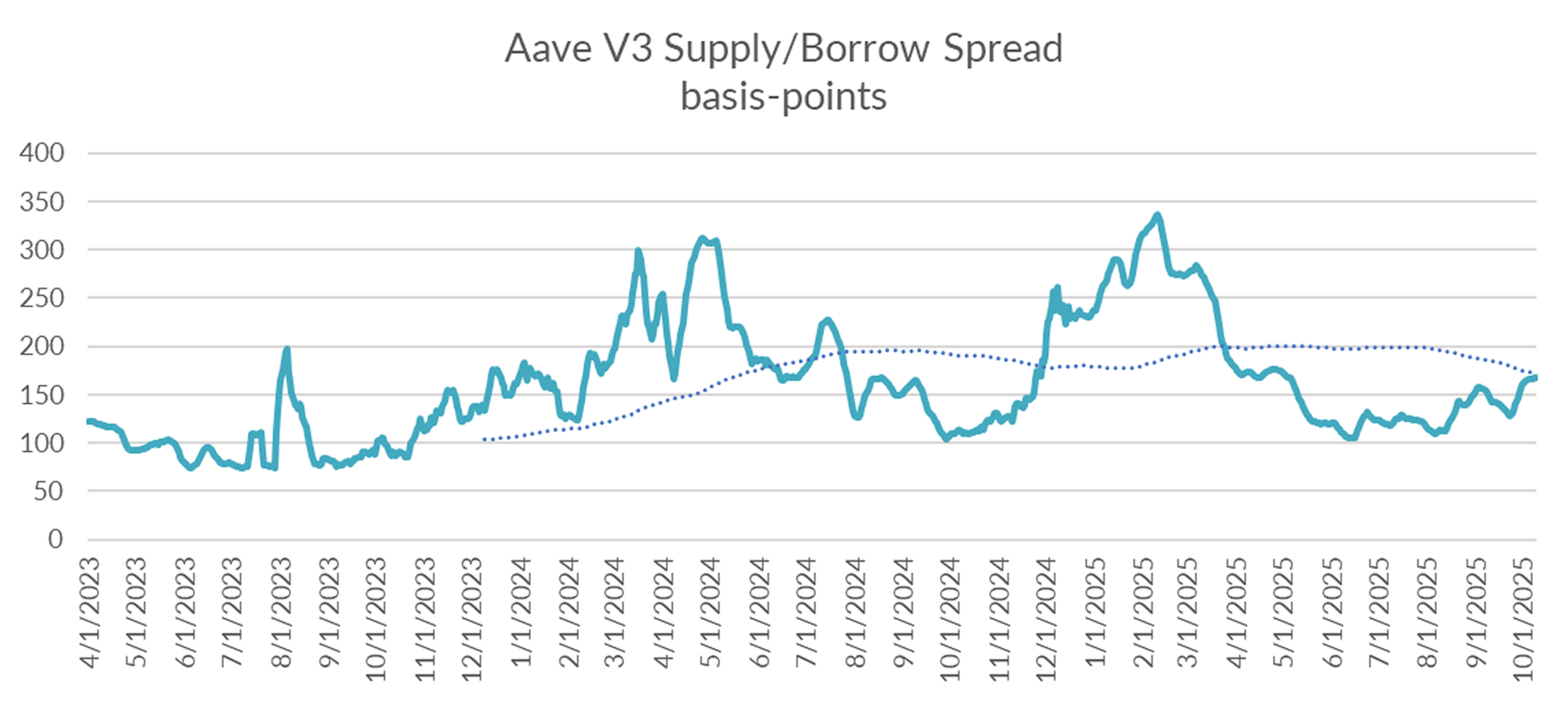

Despite this increase in borrows, overall utilization is down month-over-month causing borrow/lend spreads to creep up in recent days.

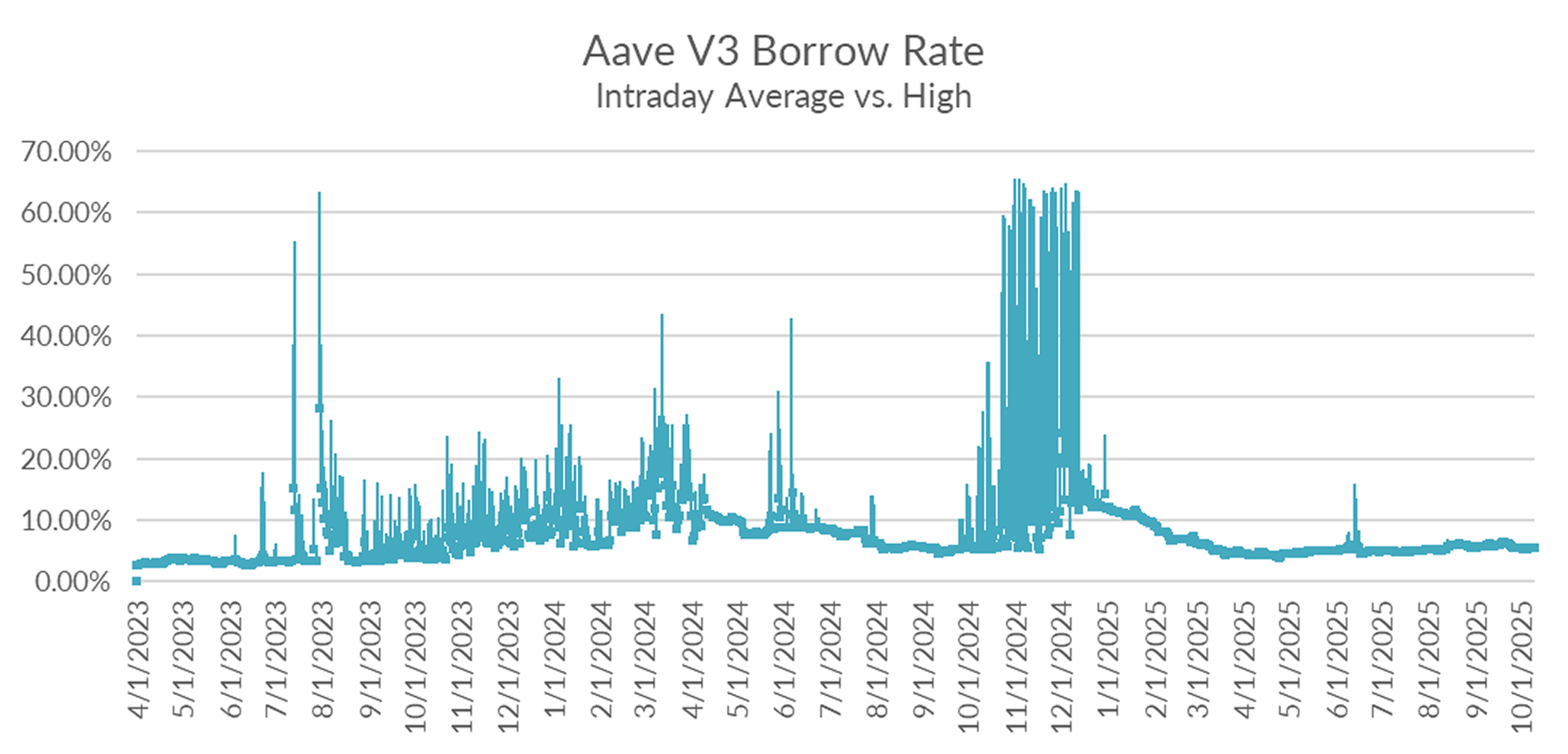

Until BTC gets past the 125k price ceiling, expect borrow demand to remain muted in the near term.

With no clear positive catalyst on the horizon, expect rates to remain subdued and perhaps continue to decline in the near and medium term.

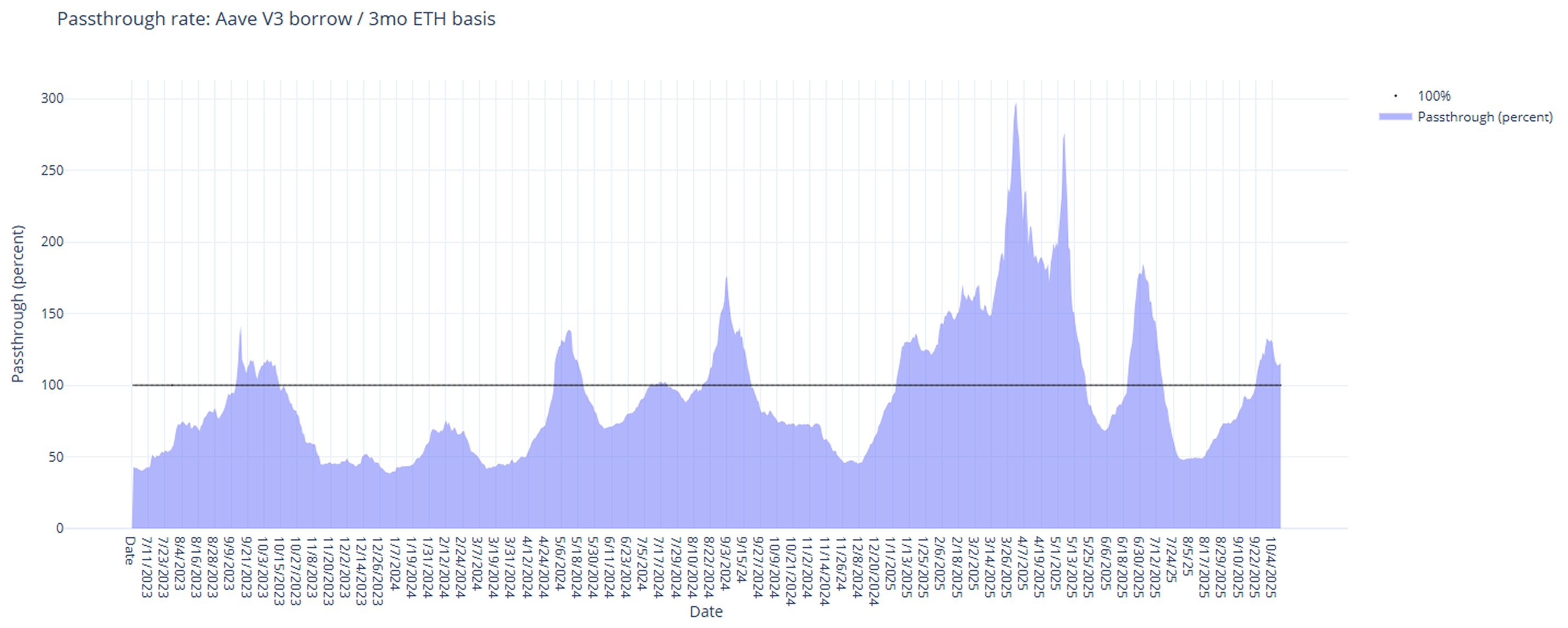

ETH Markets

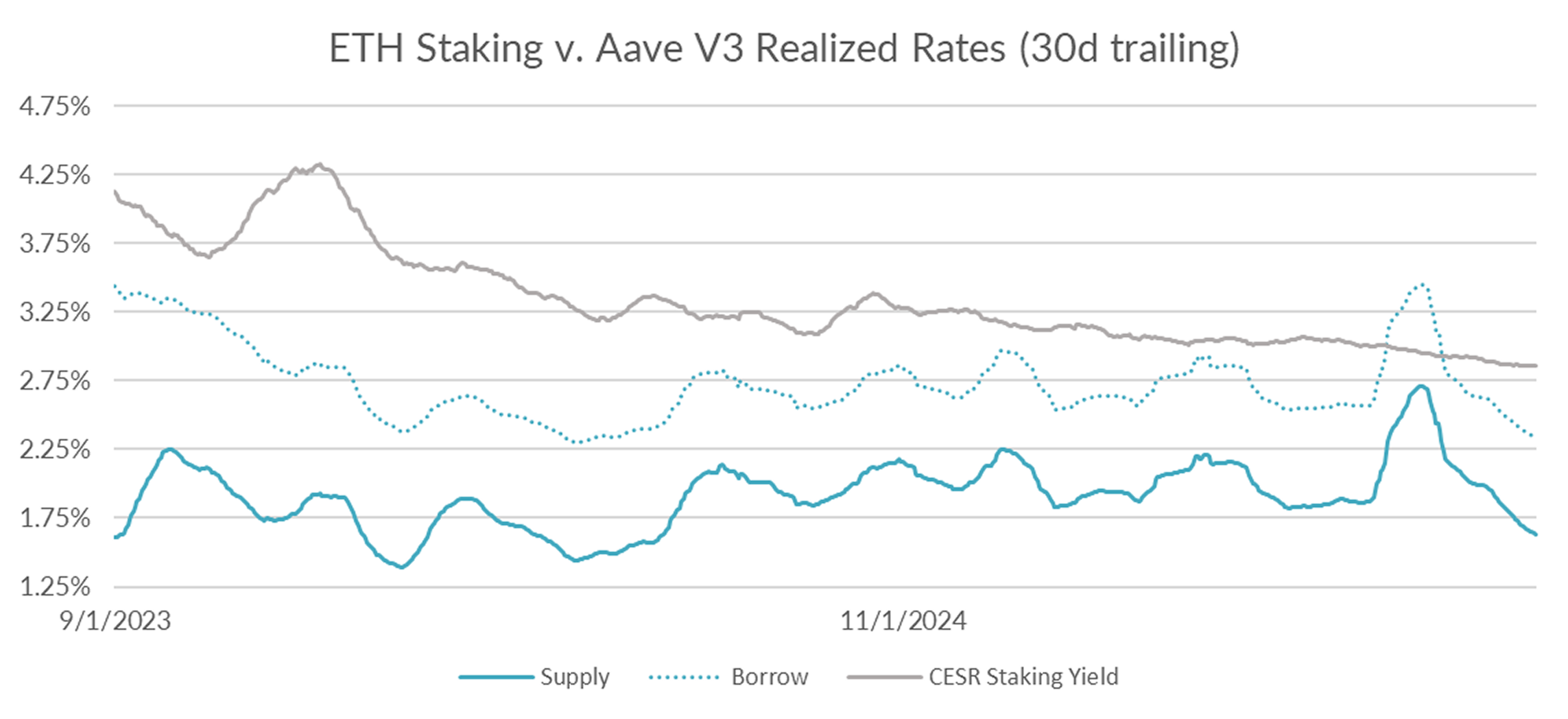

Turning now to ETH markets, ETH rates fell -1bps to 2.34% on a 30-day trailing basis over the past week. The CESR staking index, similarly, closed flat on the week at 2.86%, keeping the spread steady at around 50bp wide.

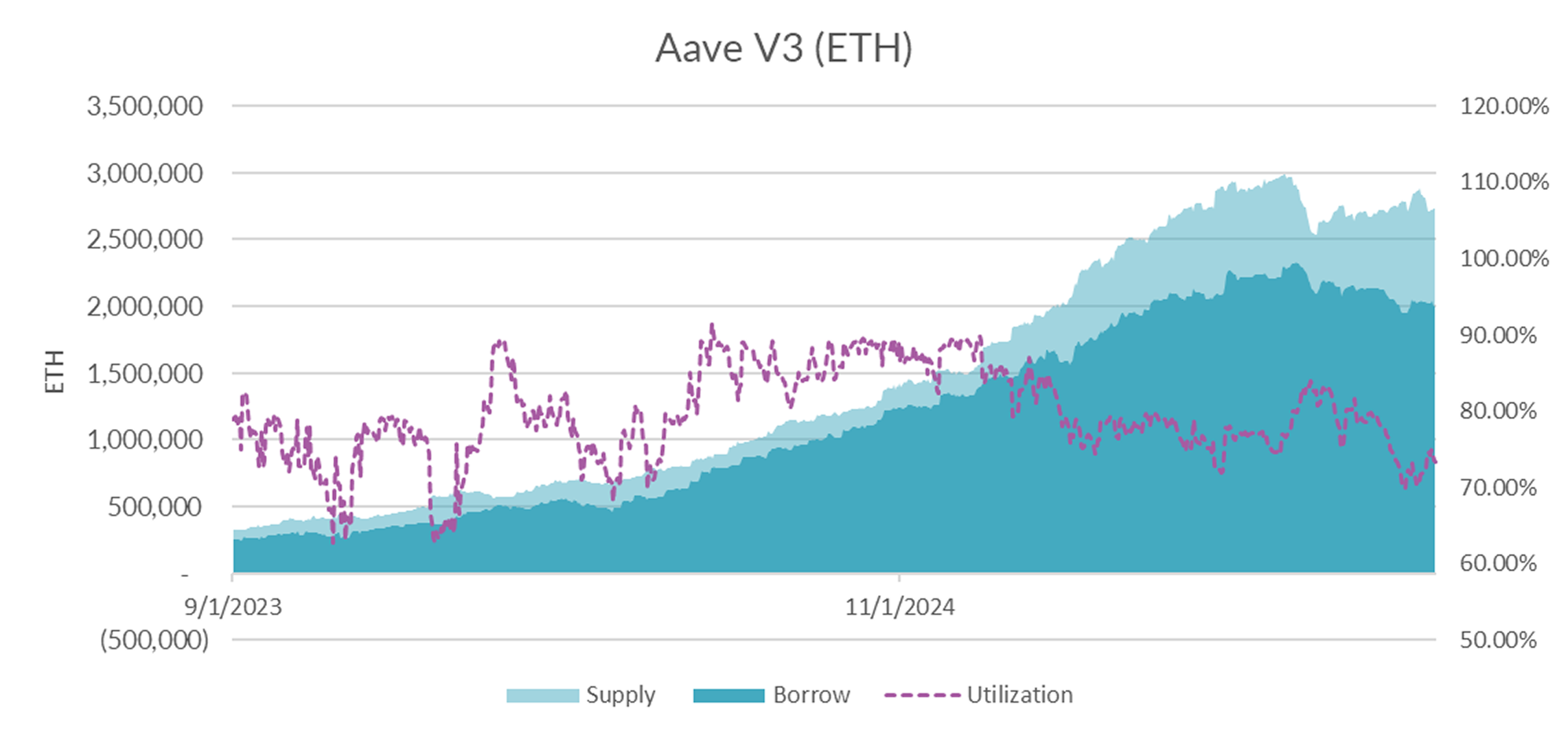

In terms of market microstructure, total supply/demand and utilization has remained surprisingly steady over the past few weeks.

And with utilization in the low 70s, near term risk of interest rate spikes is subdued.

With the spread between staking and Aave borrow rates creeping back up to 50bp for the first time since June, expect a floor to set in keep Aave rates bid in the near term around 2.3%.

Risk on sentiment in the first half of the week that took BTC back towards all-time highs quickly reversed on Friday as rising trade tensions surfaced via a social media post from Trump threatening new tariff’s on China. Equities saw the worst single-day drop since April and crypto-assets followed suit. Given rising volatility due to trade uncertainty, expect markets to delever and funding rates to decline in the near term.