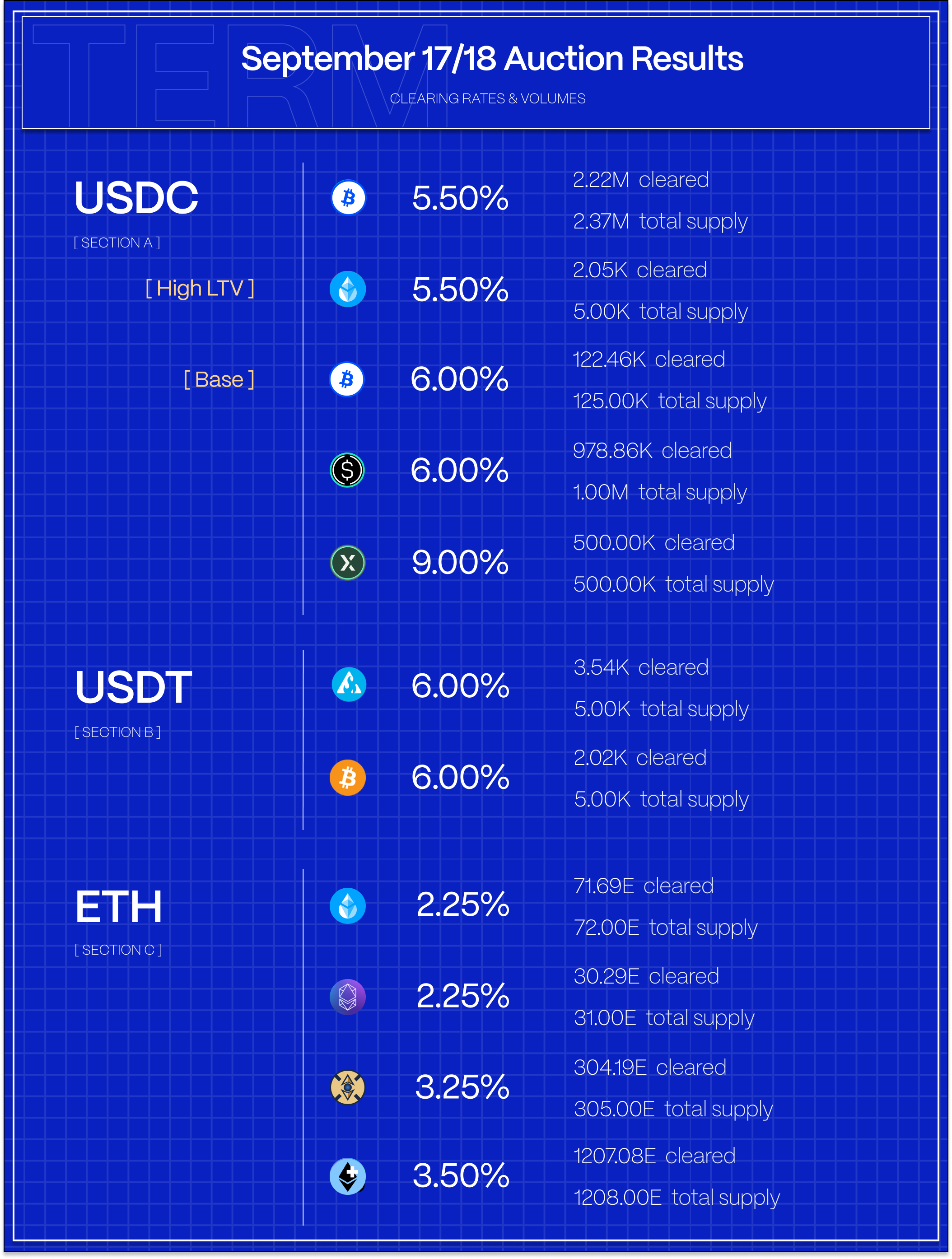

Term cleared ~4M in stablecoin loans and over 1500 ETH this week. On the stablecoin side, Term cleared the first fixed-rate loan backed by FalconX’s RWA credit strategy. On the ETH side, a sizeable chunk of ETH+ loans rolled at 3.50% offering strong risk-adjusted APRs in excess of the ETH staking rate.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

Basis and Perpetuals Markets

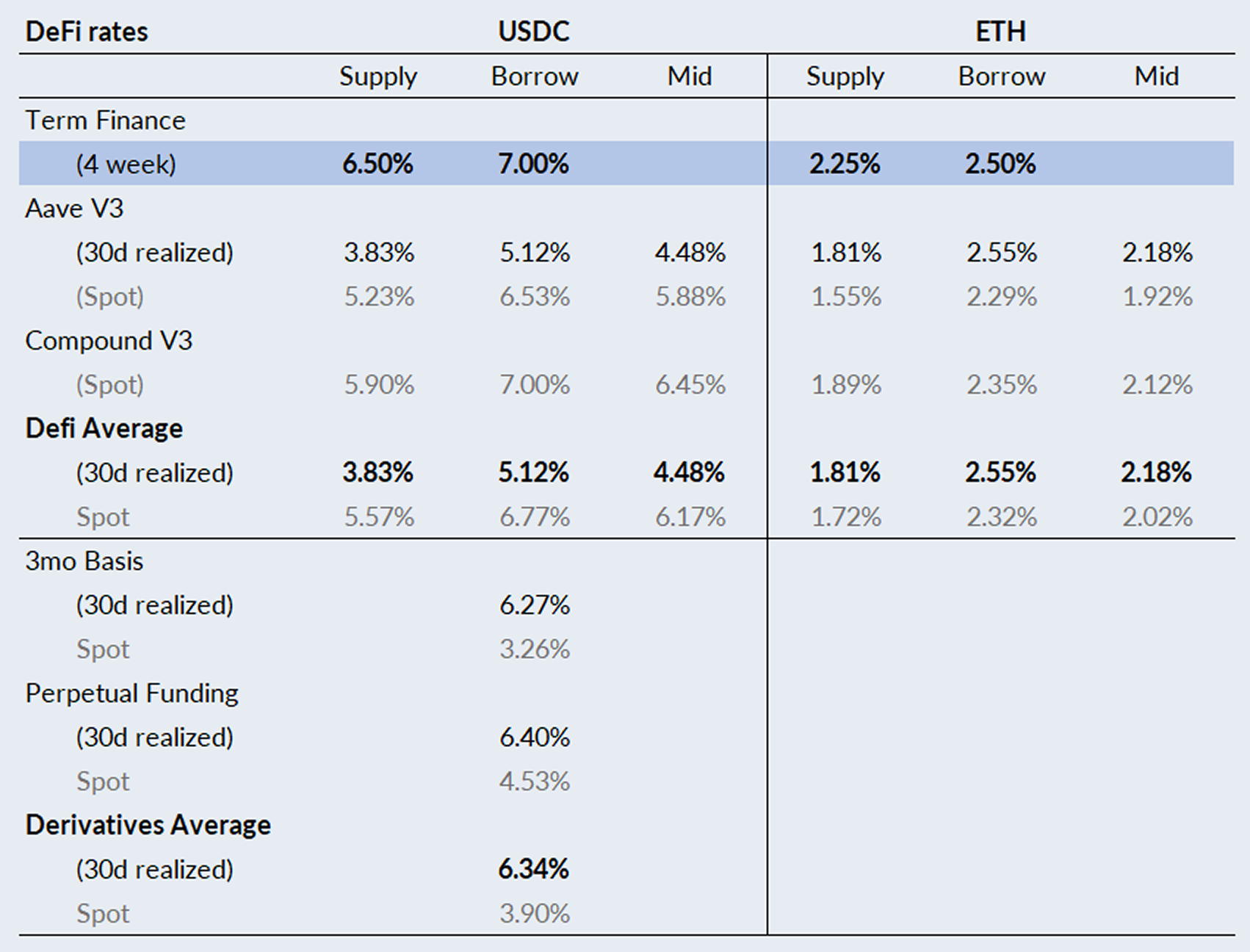

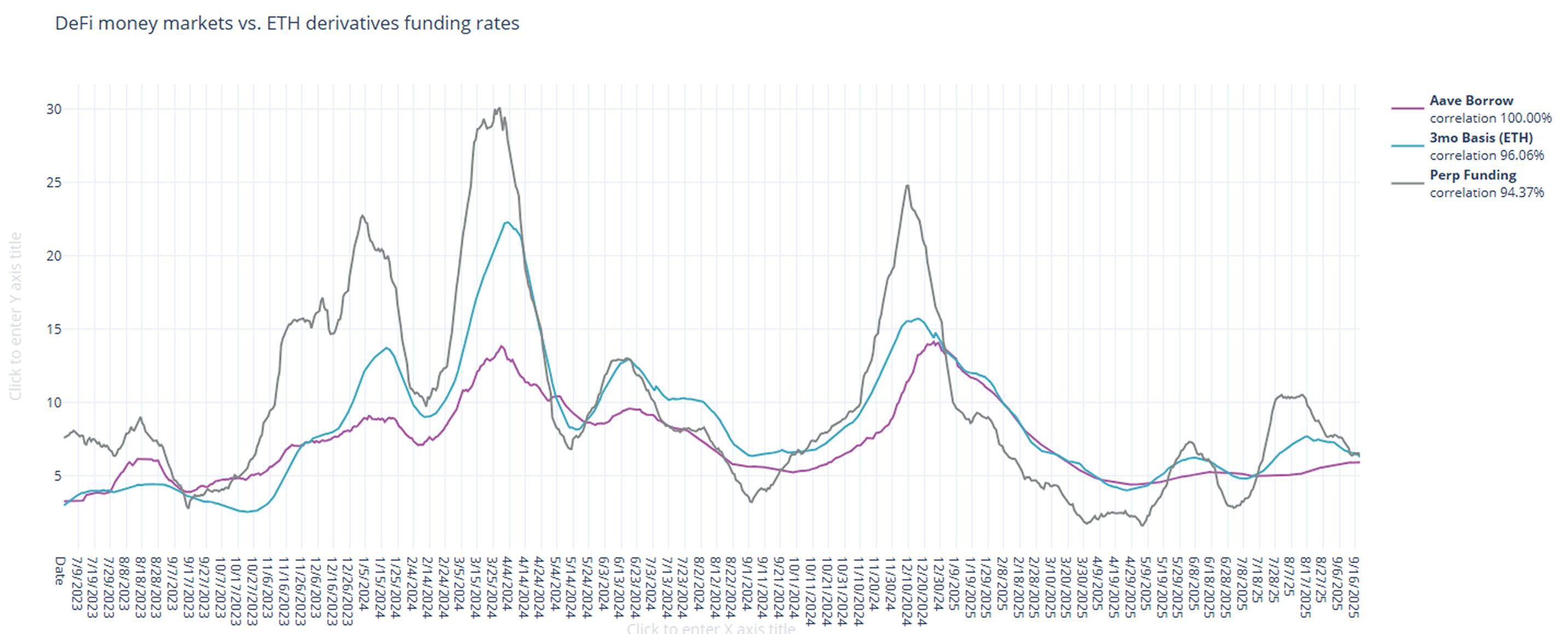

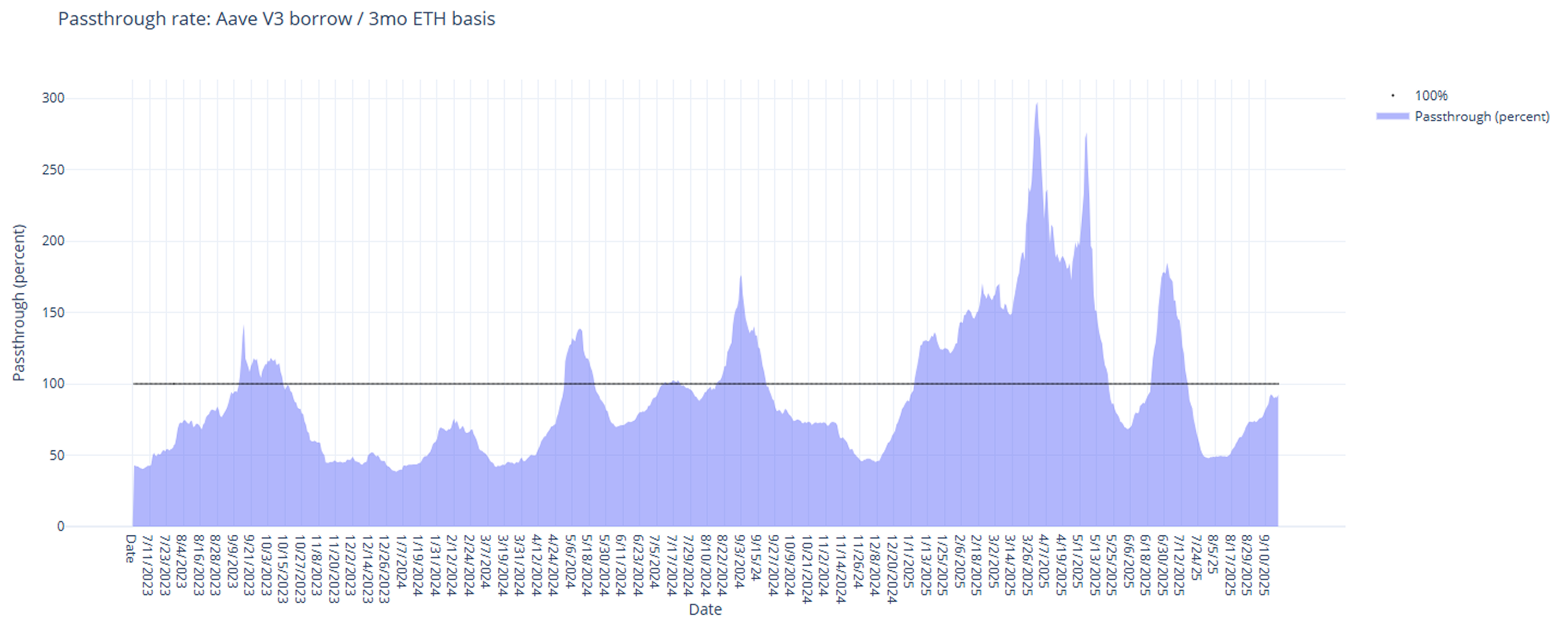

In derivatives markets, funding rates continued to drop, with 3-month basis falling -31bps to 6.27% and perpetual funding rates down -46bps to 6.40% on a 30-day trailing basis.

With derivatives funding rates on the decline, the ratio between DeFi and derivatives funding continues to normalize back towards parity.

With the 25bp cut from the Fed this week highly anticipated, risk assets (including crypto) saw very little follow-through on the cut. In the near term expect funding rates to continue to decline absent something unexpected.

USDC Markets

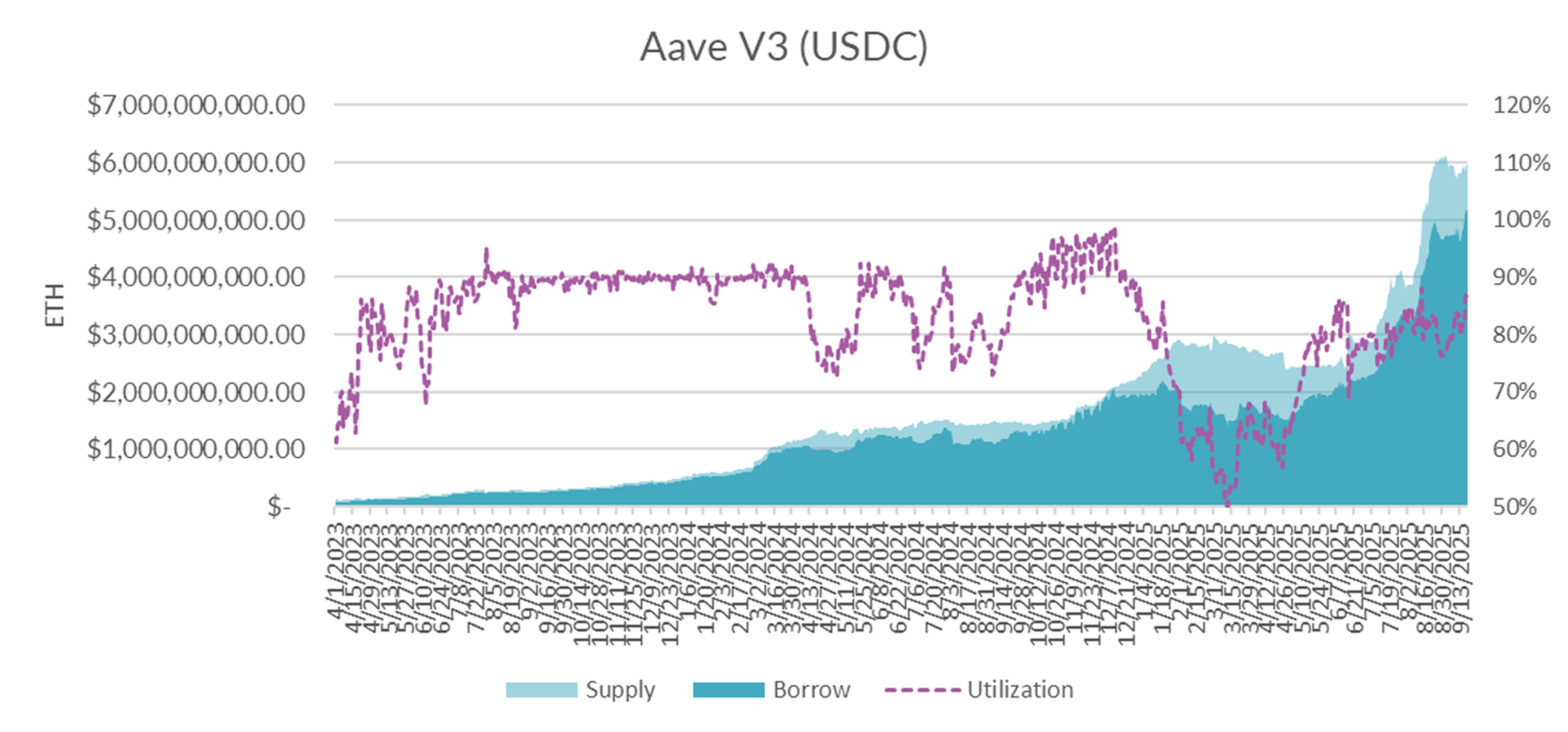

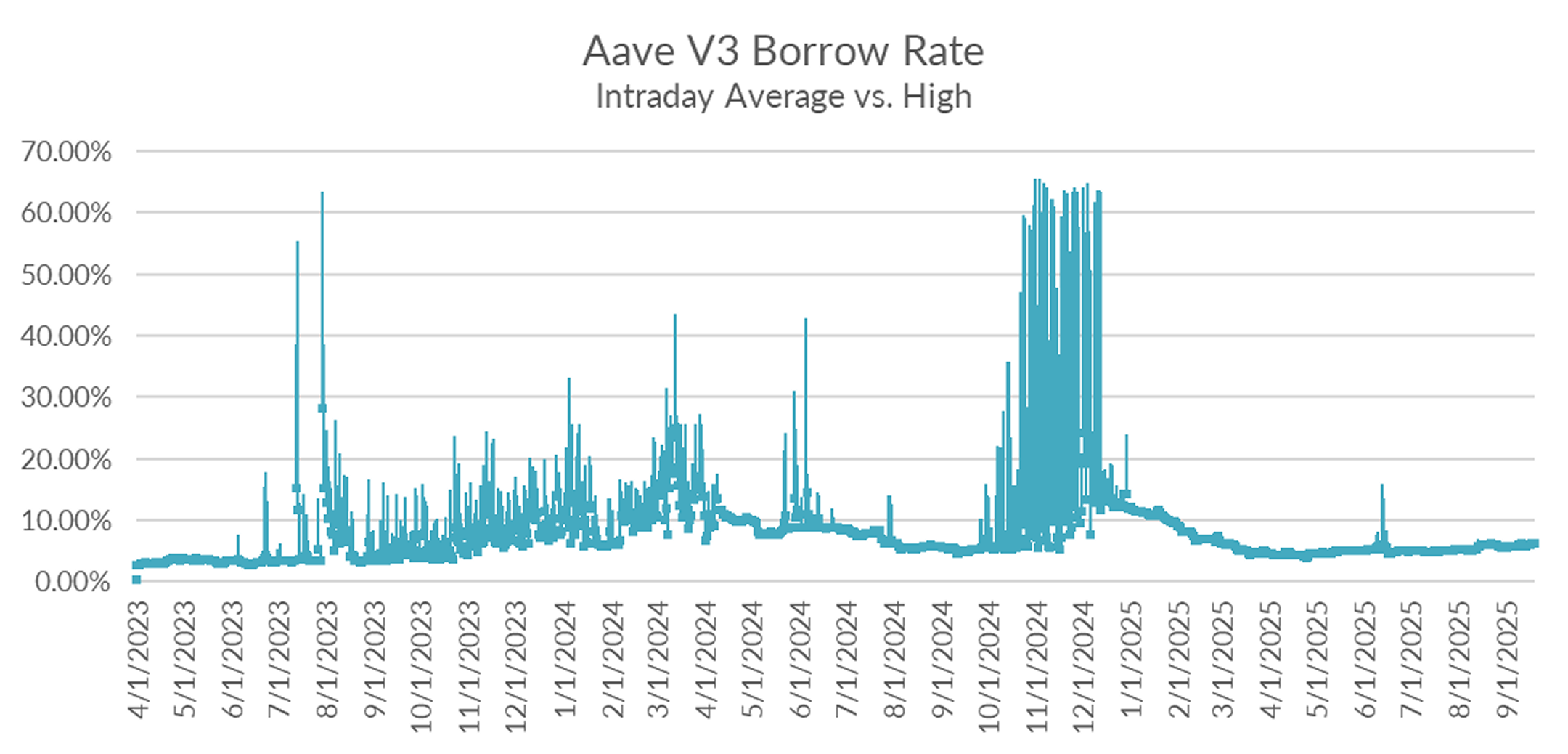

Turning to DeFi variable rate markets, the 30-day trailing average rose +2bps to 5.91% on a 30-day trailing basis. On a shorter lookback period, USDC borrow rates averaged 6.08% suggesting further gains ahead.

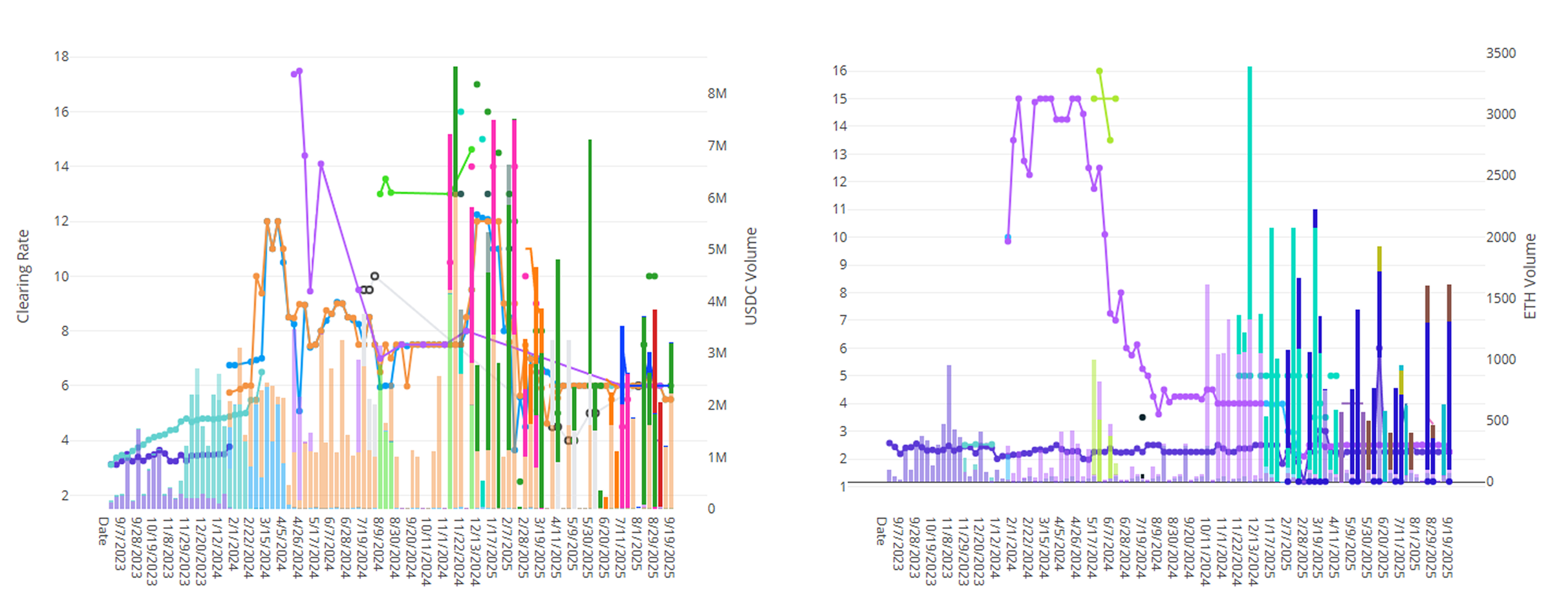

Diving into the microstructure of Aave's USDC markets, USDC supply rose +148M while borrows declined just +310M over the same period, taking utilization into the high 80s, and close to the interest rate kink.

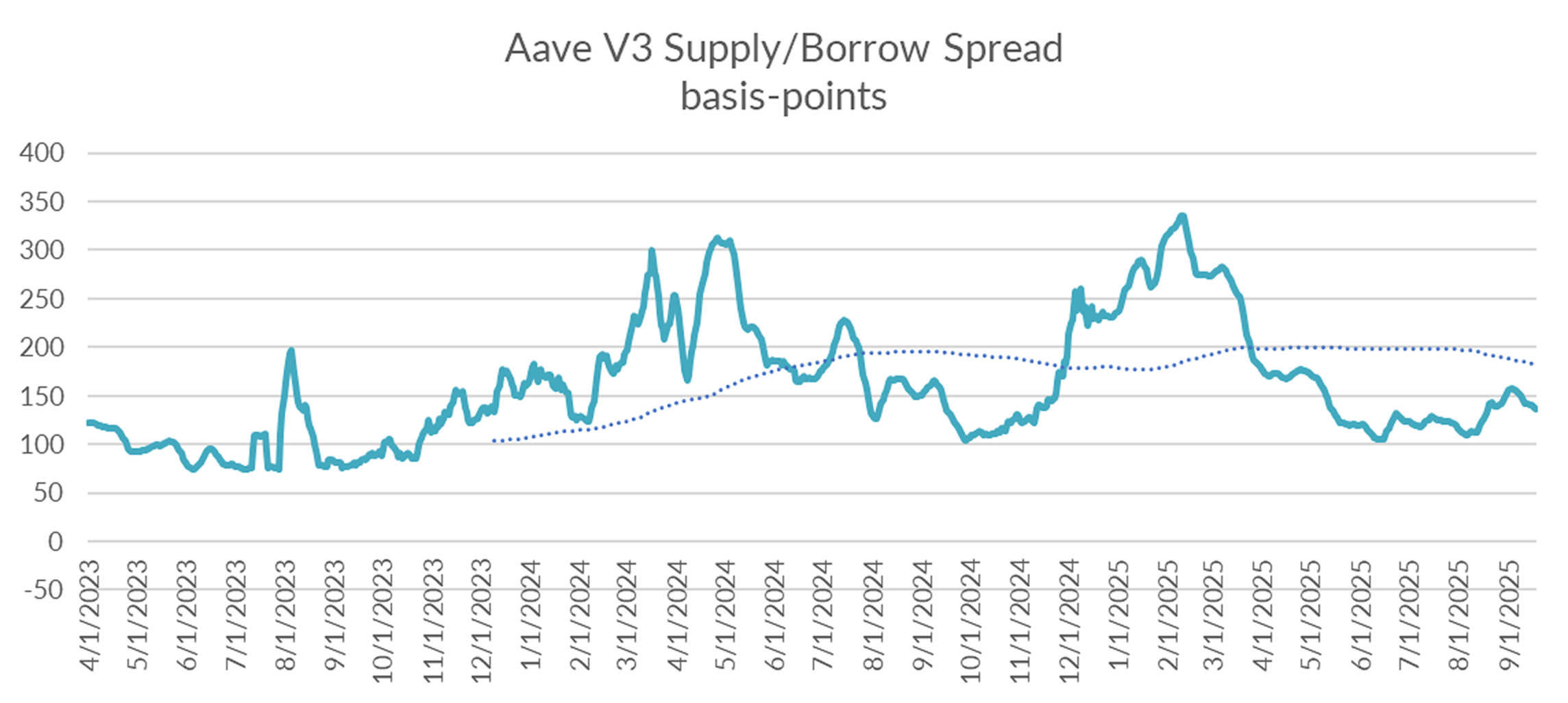

And with rising utilization, supply/borrow spreads on Aave are continued to tighten.

As we’ve seen throughout the year, intraday volatility on Aave has remained subdued. But with utilization approaching the kink for the first time since Q4 of 2024, things might start to get interesting.

At current levels, USDC on Aave is just a few hundred million off the kink where borrow rates start to get volatile. Risk leans towards higher stable borrow rates in the near term.

ETH Markets

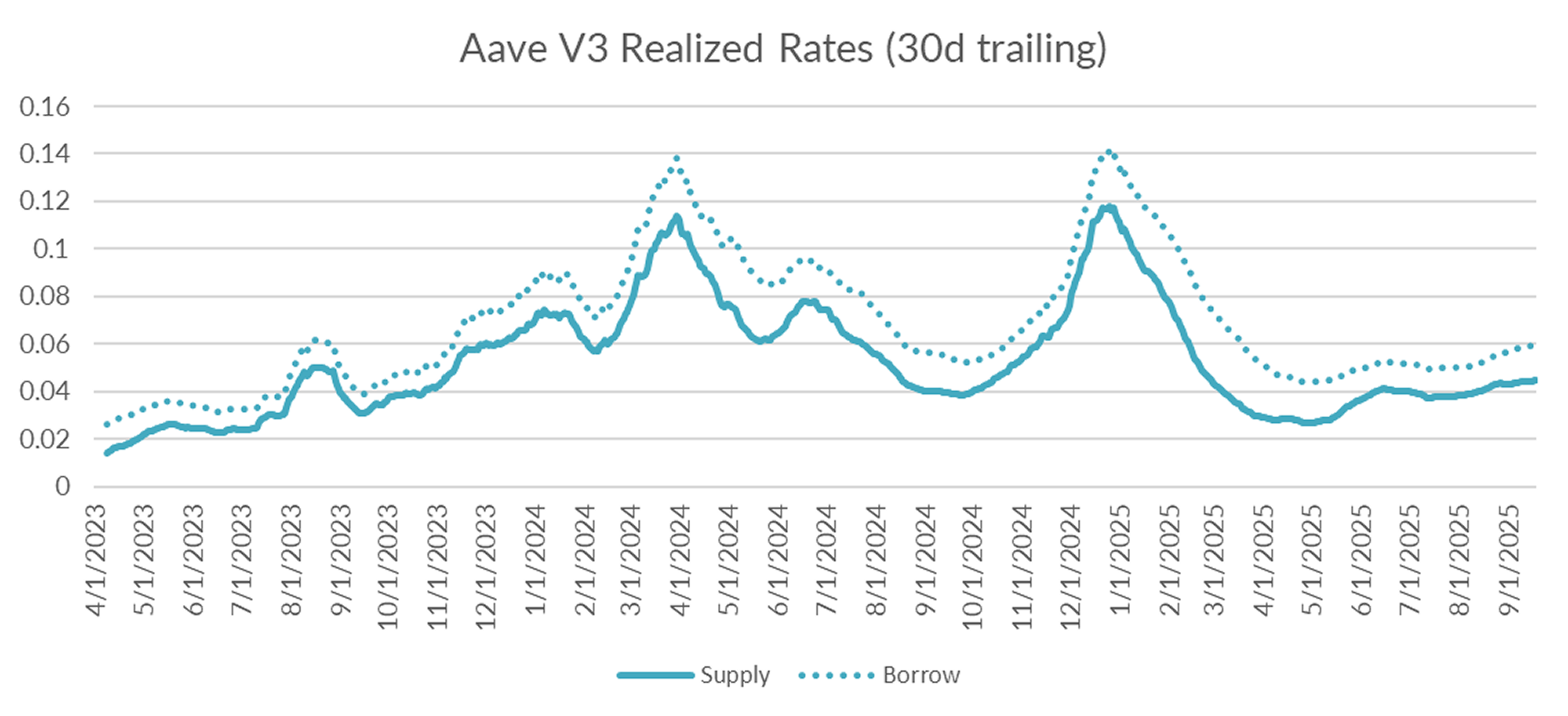

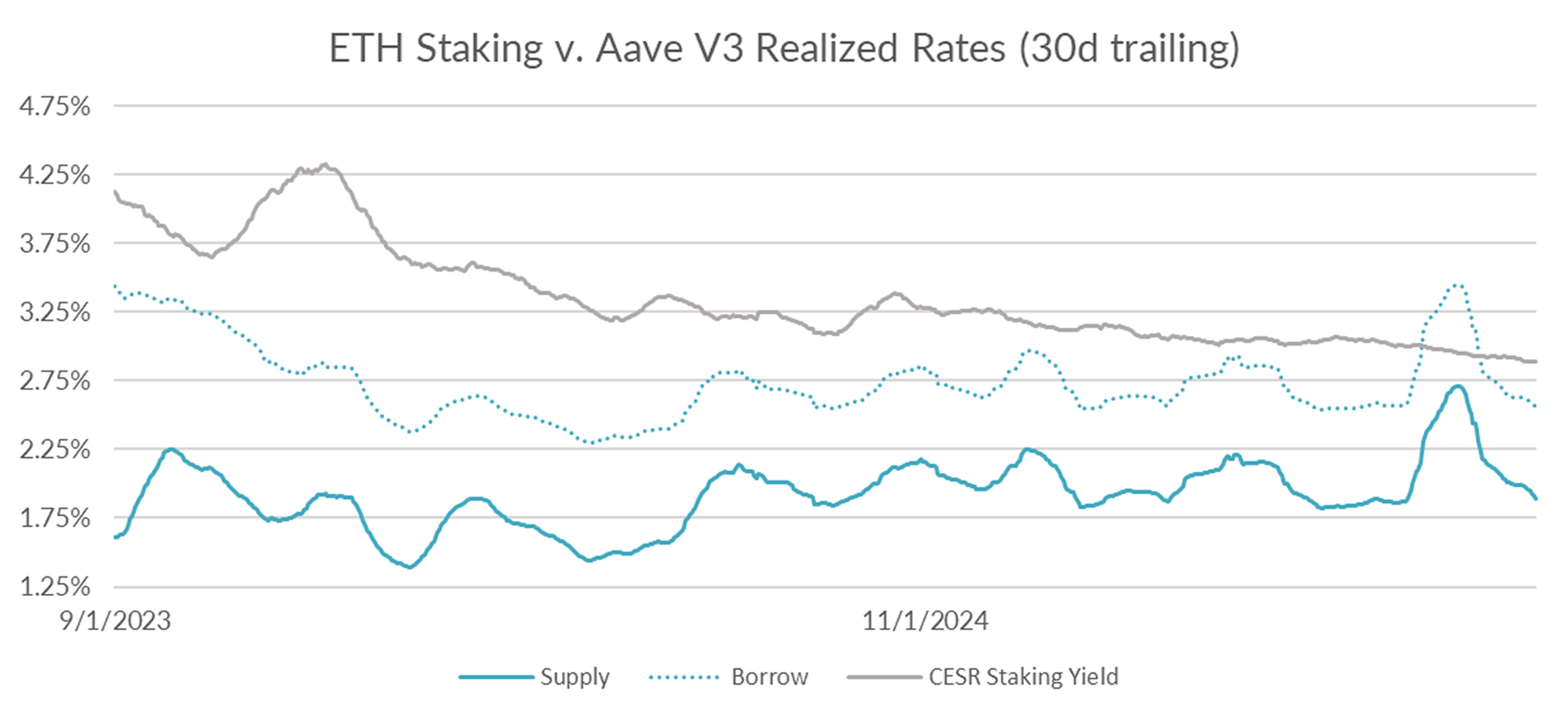

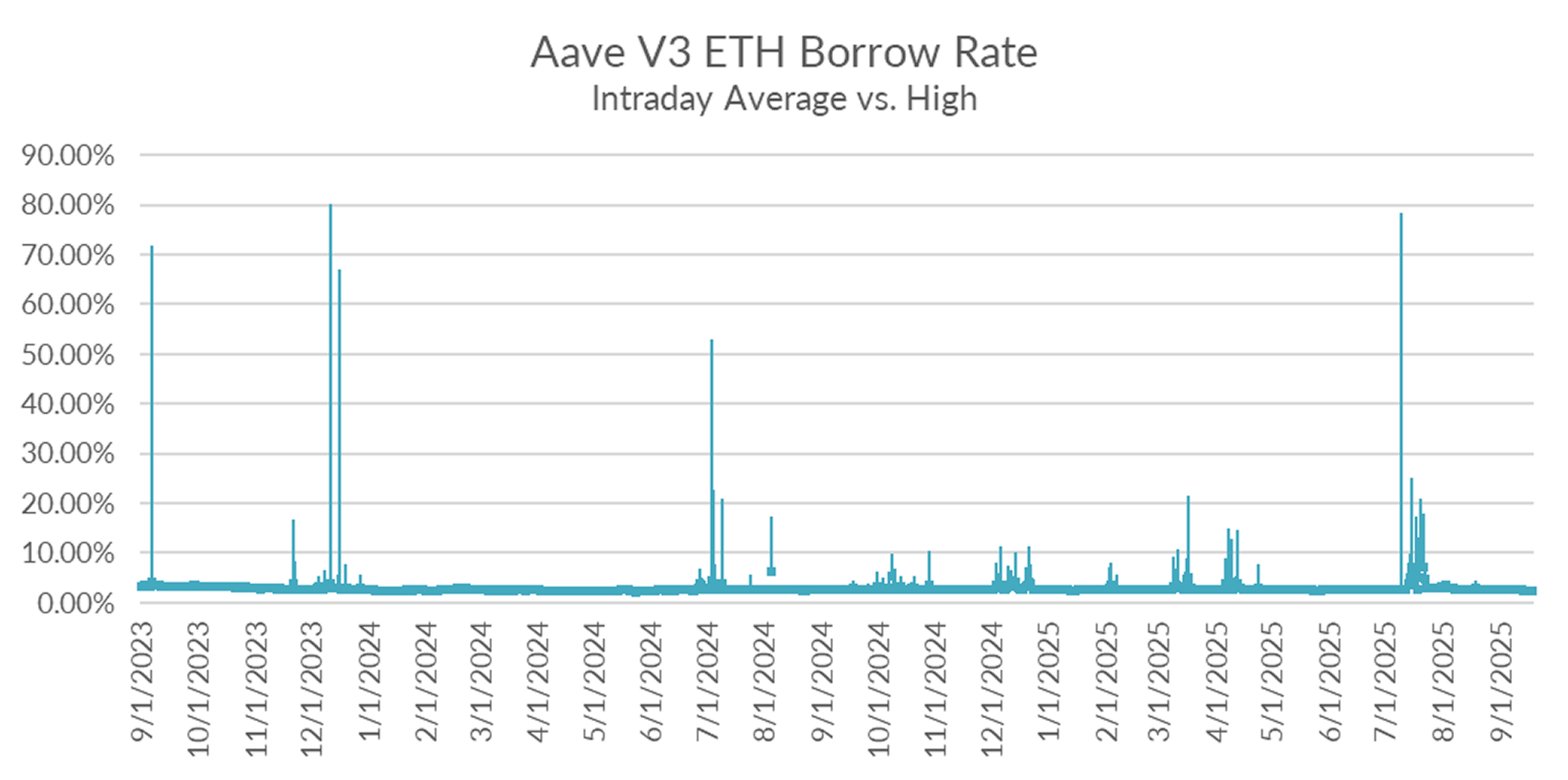

Turning now to ETH markets, ETH rates fell -8bps to 2.55% on a 30-day trailing basis over the past week. The CESR staking index, closed down a more subdued -1bp on the week at 2.88%, widening the spread by a slight margin.

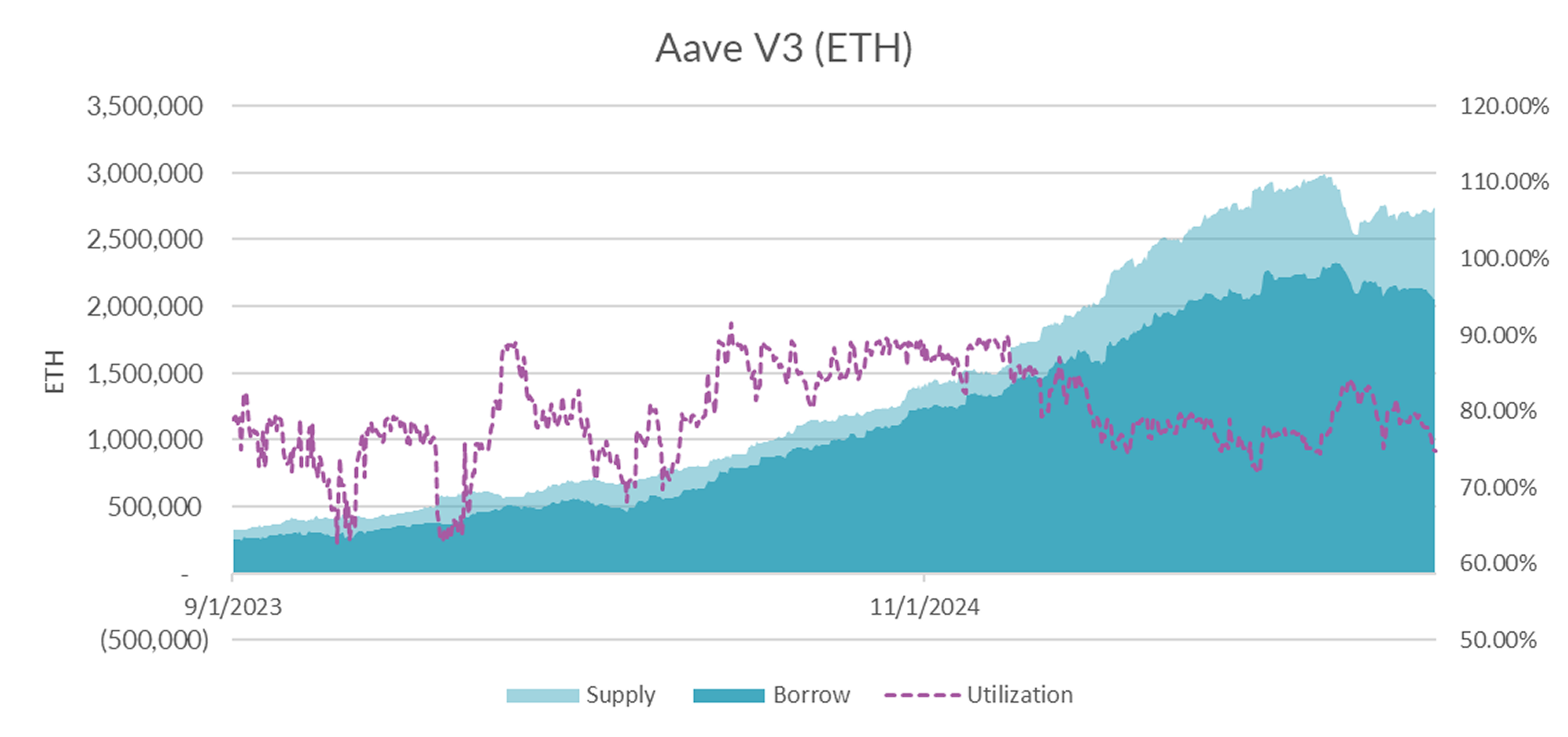

In terms of market microstructure, overall ETH supply appears to be stabilizing around 2.7M ETH with borrows continuing to decline at a relatively rapid rate.

And with utilization in the low 70s, near term risk of interest rate spikes is subdued.

As long as ETH staking rates continue to decline expect ETH borrow rates to stay low in the near term.

The Fed delivered on a -25bps cut this week, which was highly anticipated by markets. Focus now turns back to the debt ceiling on October 1, where the Democrats are expected to put up a bigger fight than the last time around. Expect volatility to be elevated and leverage pared back to reduce risk of liquidations. Basis is likely decline over the next few weeks and overall DeFi yields along with it.