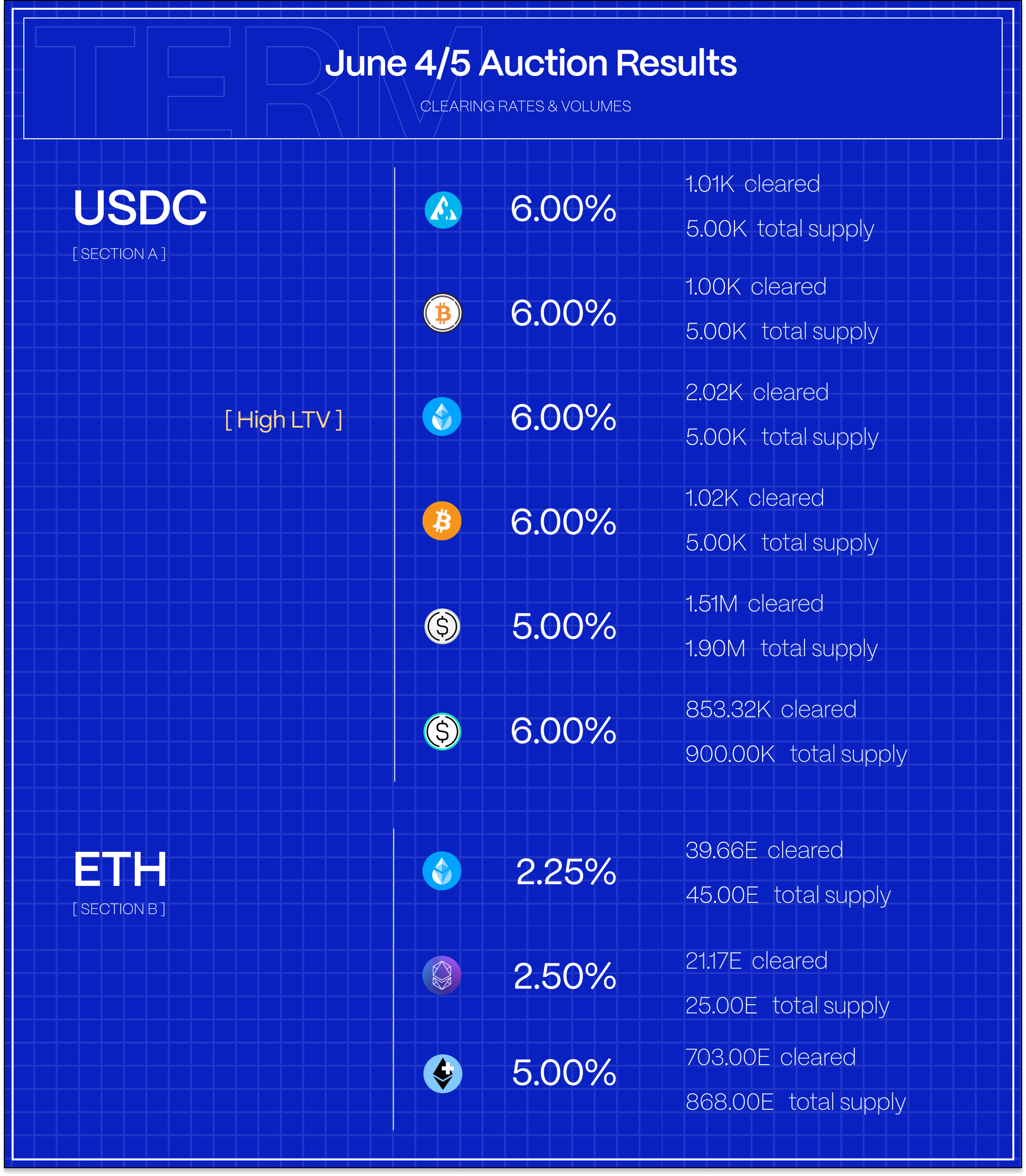

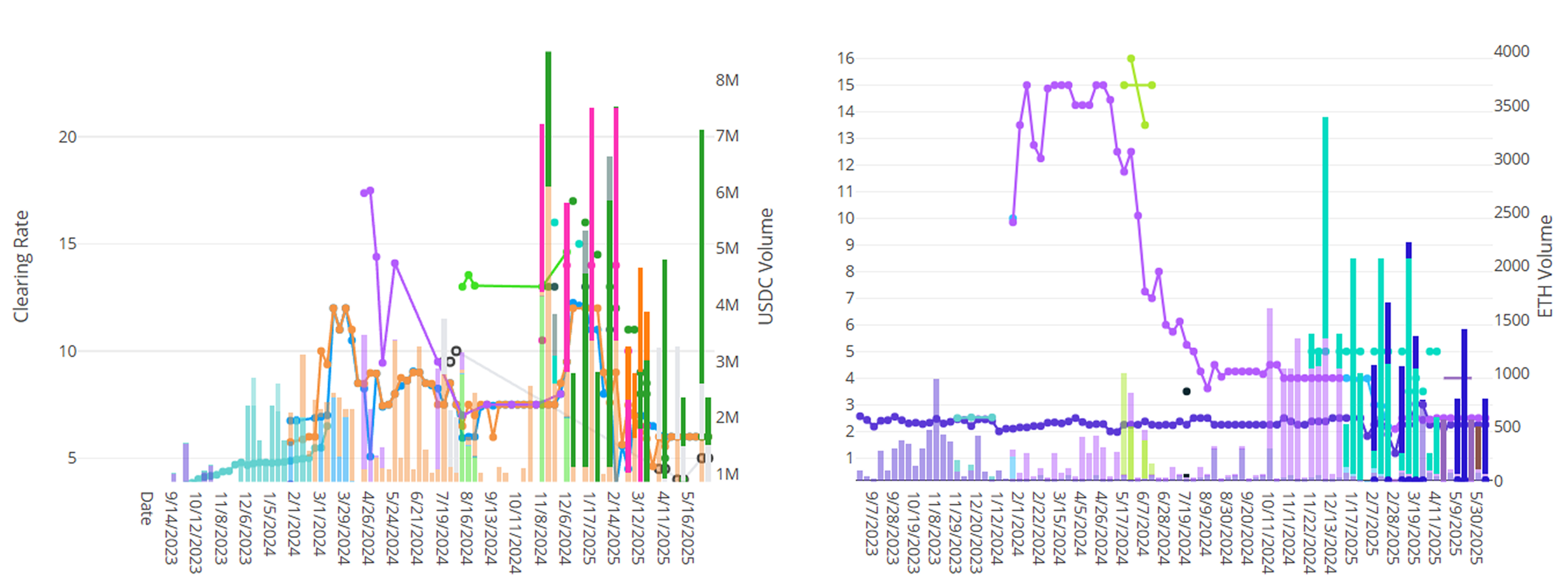

Rates on Term were relatively steady this week across the board. Demand to borrow on Term continues to center around exotic collateral like Ethena’s PT-sUSDE and Reserve’s ETH+. Over $3M was cleared across all auctions this week.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

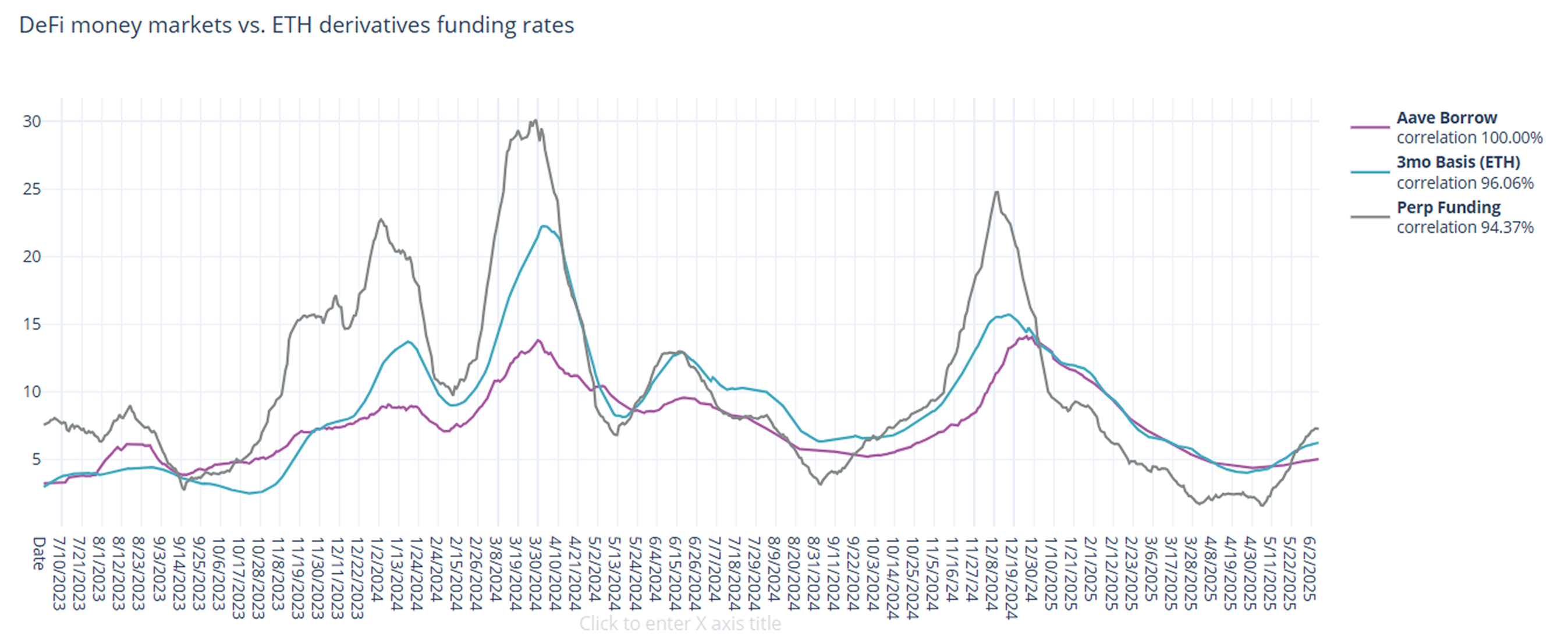

In derivatives markets, funding rates continue to rise. On a 30-day trailing basis, 3-month basis rose by +25bps to 6.25% and perpetual funding rates rose to 7.25%, up +56bps from the week prior.

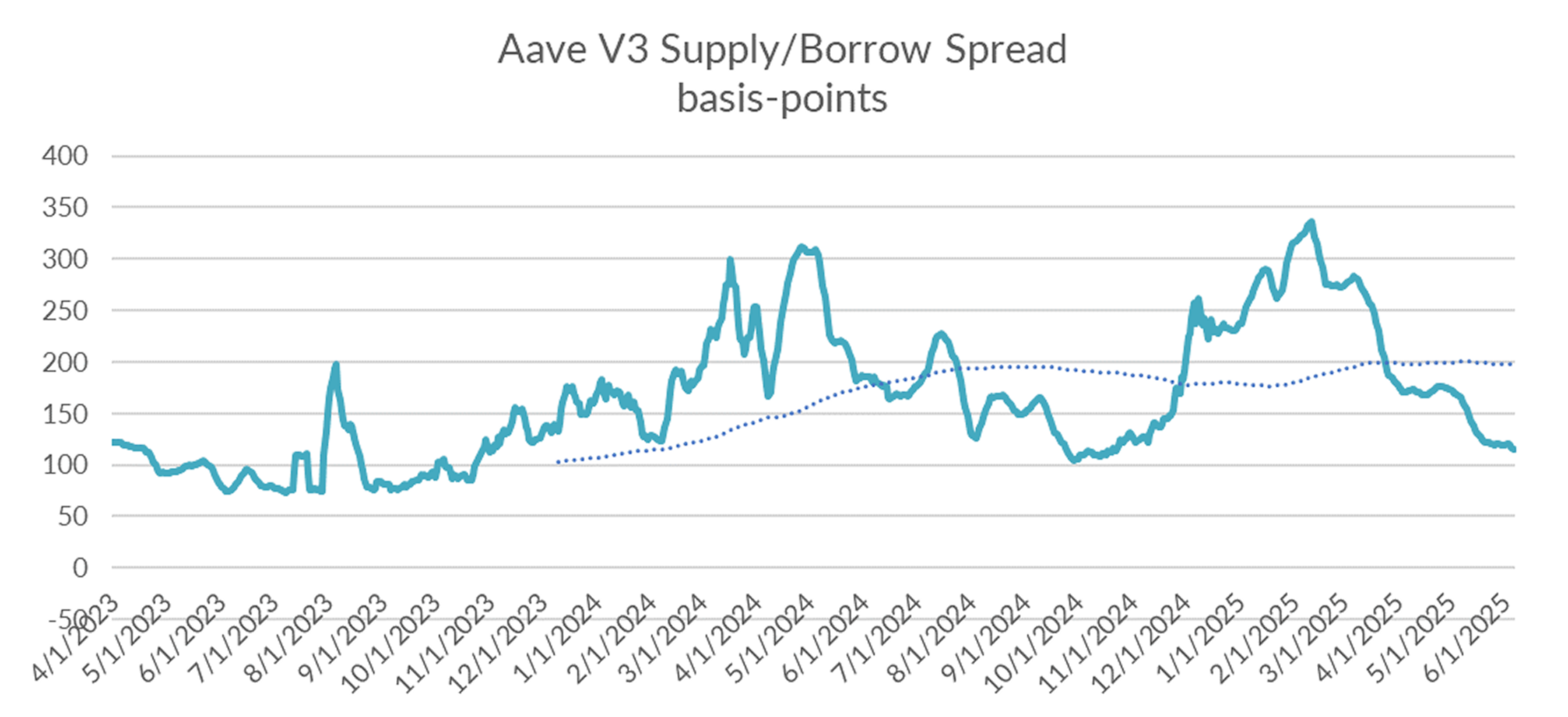

DeFi rates also rose, but at a much slower pace, causing the spread between DeFi and derivatives to continue to narrow back toward historical norms.

Zooming in on price action over the past week, derivatives rates fell for the second week in a row, suggesting that the flurry of excitement of the past few weeks is beginning to dwindle.

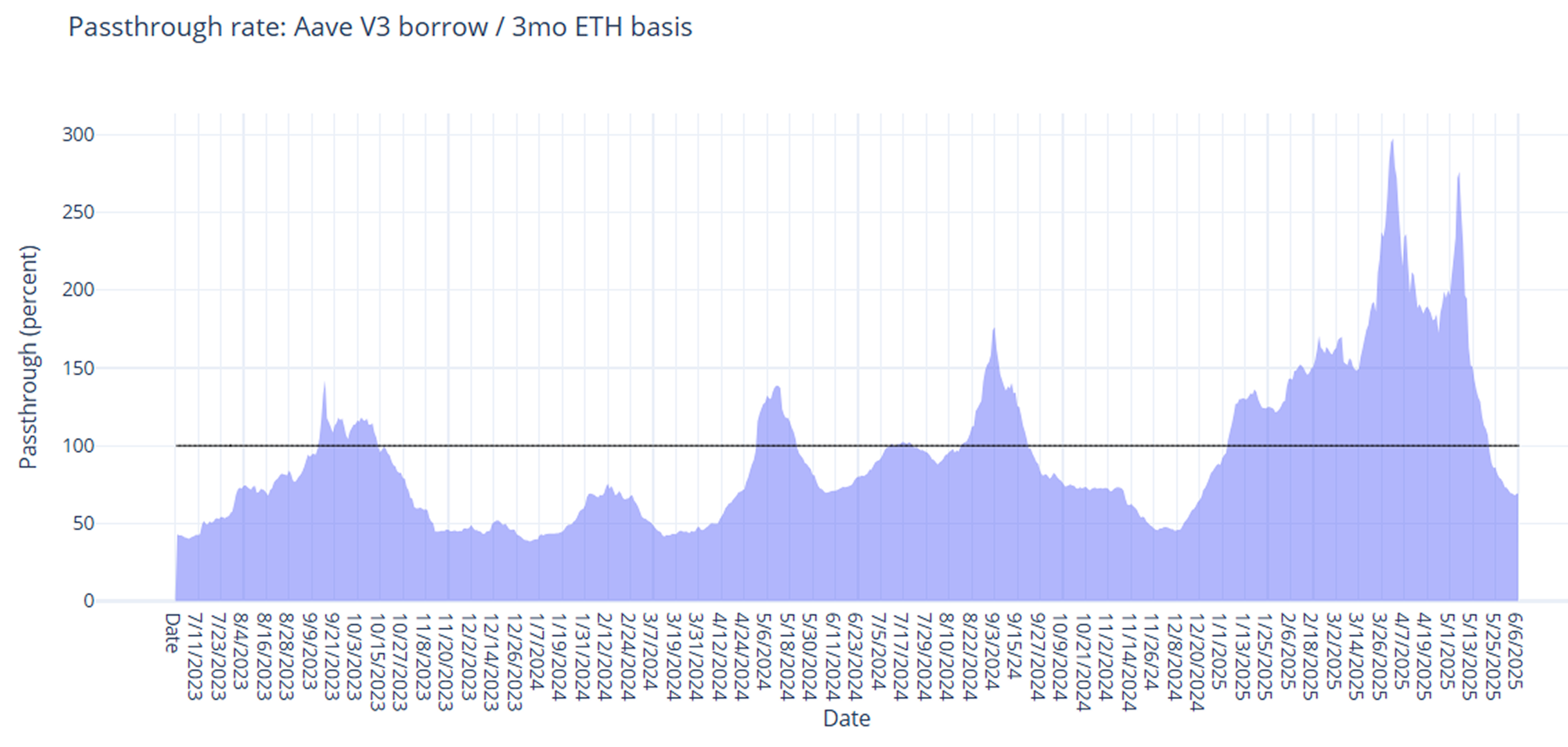

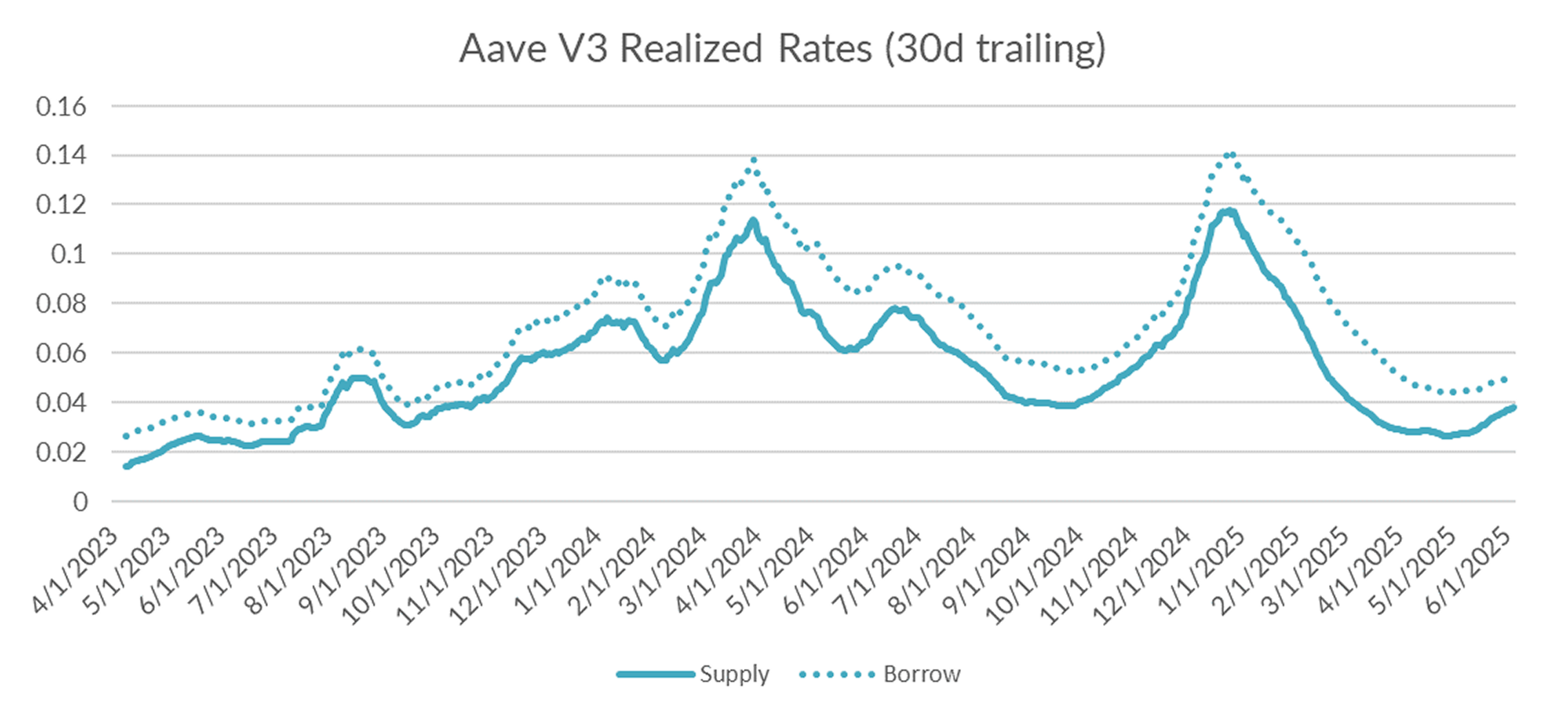

Turning to DeFi variable rate markets, the 30-day trailing average rose +13bps on the week to 5.04%. Over a shorter lookback period (just seven days), Aave borrow rates averaged 5.22% on the week, suggesting further gains ahead.

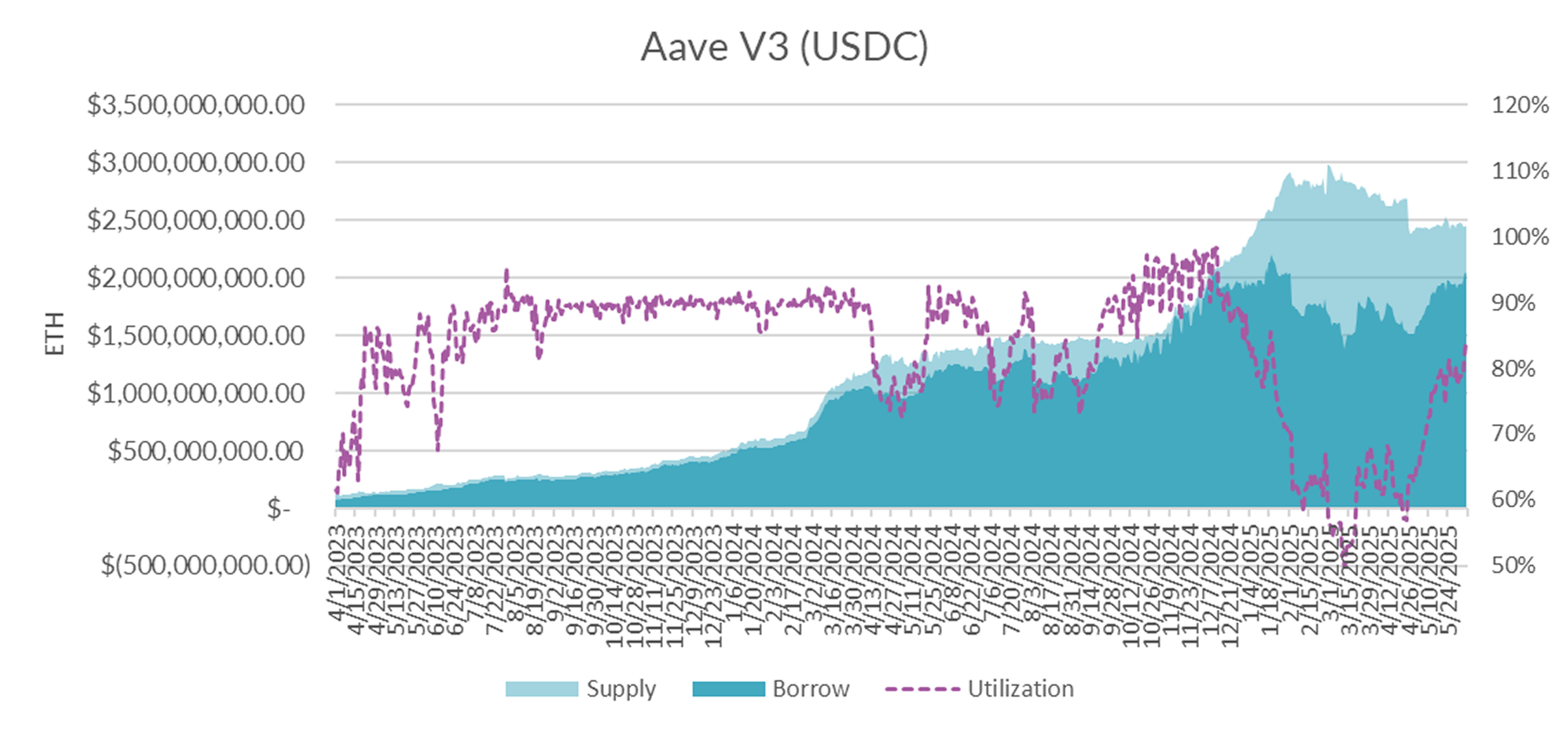

Diving into the microstructure of Aave's USDC markets, utilization rose into the mid 80s, with elevated utilization largely driven by a surge in total demand by around +132M USDC.

With this newfound bump in demand, utilization on Aave is now within stones-throw of the 90% kink.

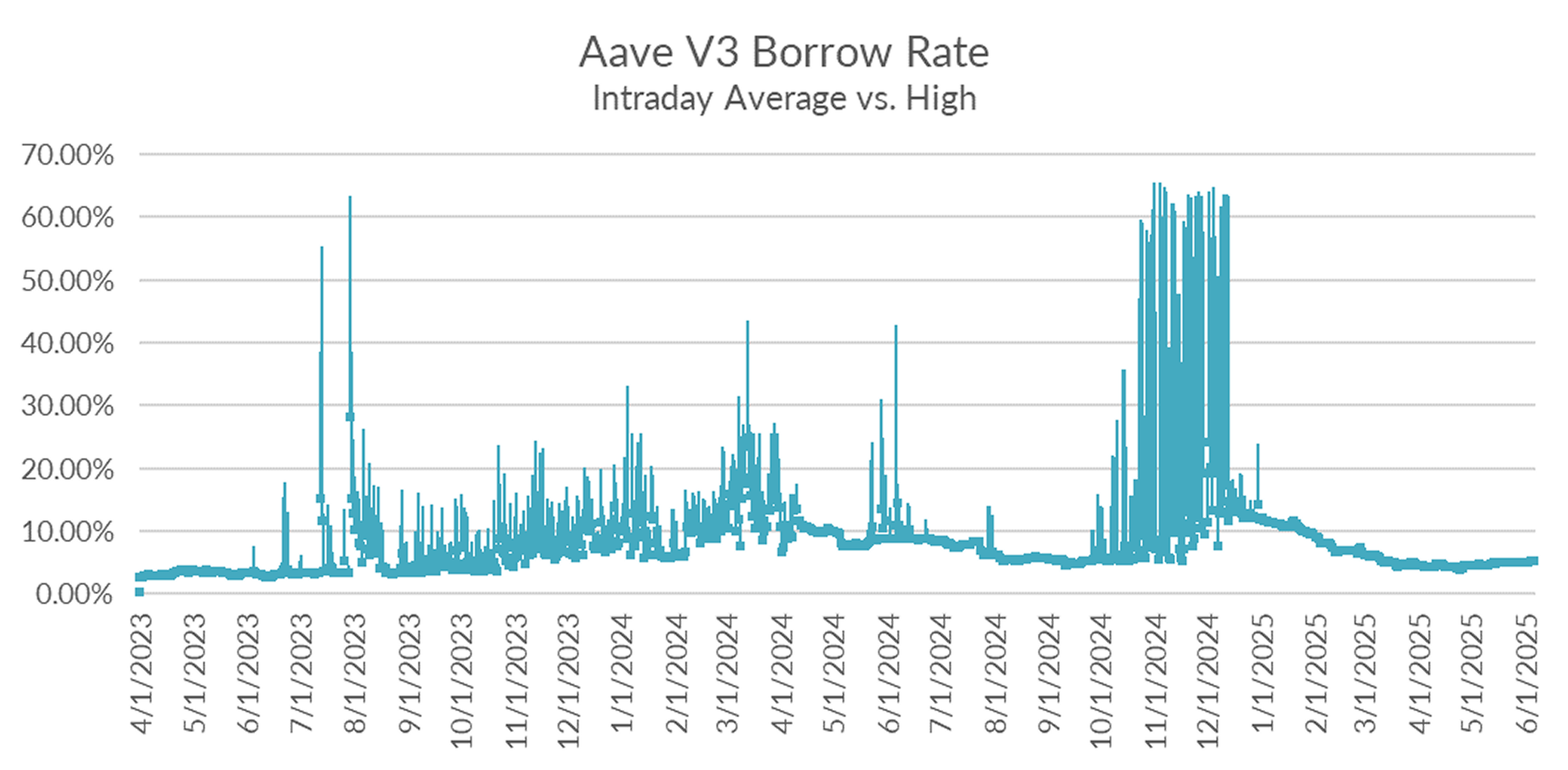

For now, however, rates remain stable

Given that derivatives rates and DeFi rates are moving in opposite directions, the path forward is highly uncertain.

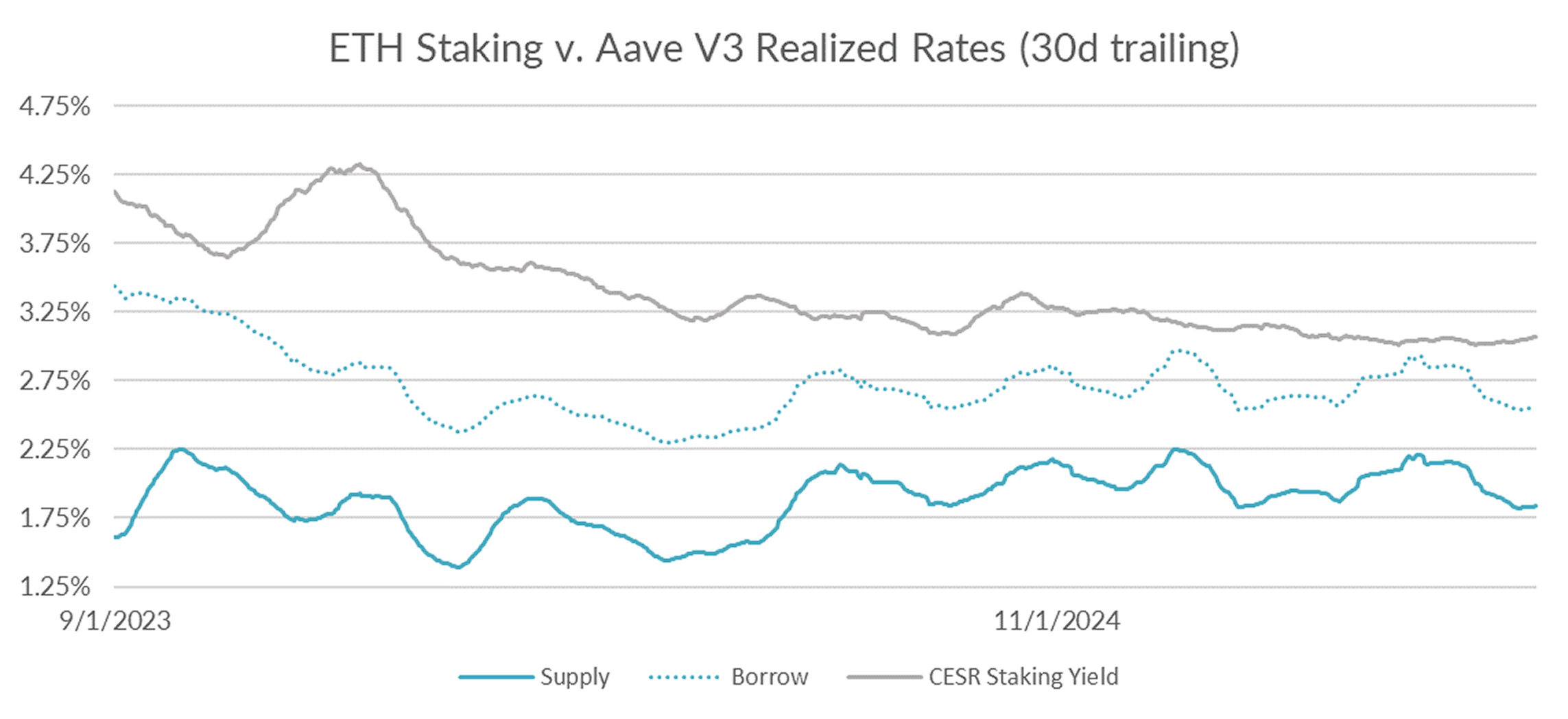

Turning now to ETH markets, ETH rates held steady, rising by +1bp on the week to 2.55% on a 30-day trailing basis. The CESR staking index similarly rose slightly by +2bp to 3.07%, widening the spread by +1bp on a 30-day trailing basis.

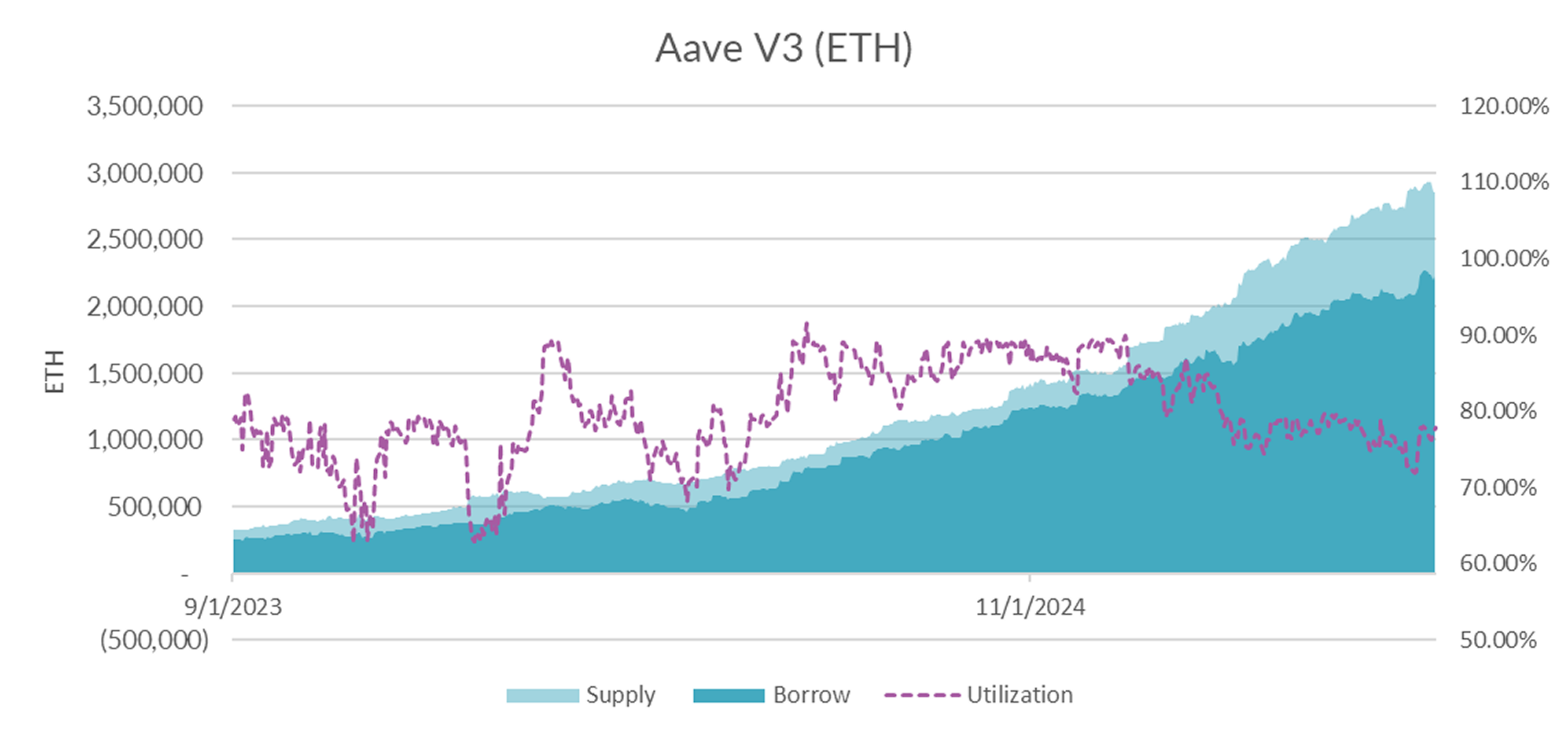

Market internals show that supply (-41k ETH) declined faster than demand (-29k ETH) over the past two days, with utilization slightly higher in the upper 70% range.

With ETH rangebound at current levels, expect borrow rates to find a floor around 2.5%.

This level implies ~0.5% spread between staking and borrowing rates, which gets looping yields up towards the targe 8% range that attracts many ETH denominated DeFi funds.

Cryptoassets traded choppy and in a sideways motion this week. With a lack of upside follow-through to BTC’s run to 110k two weeks ago, it is not surprising that demand for leverage, and implied funding rates, is on the decline. With summer kicking off in earnest, expect markets to hold steady in the near term.