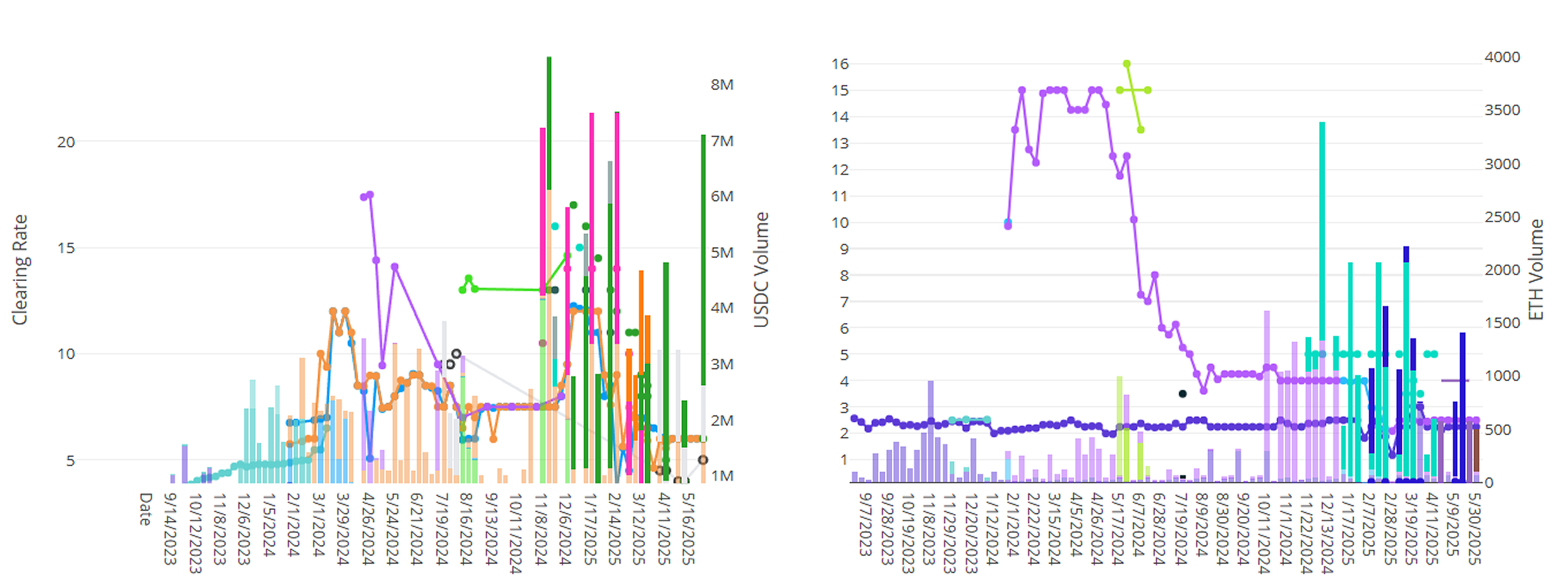

Term cleared around ~8.5M in volume this week, with volumes split between USDC and ETH loans. The majority of USDC loans were on account of rolling of the May PT-sUSDE loans over into matched-maturity loans for the next expiry. On the ETH side, Term onboarded ynETHx collateral and held auctions for both 4 week and 13 week maturities.

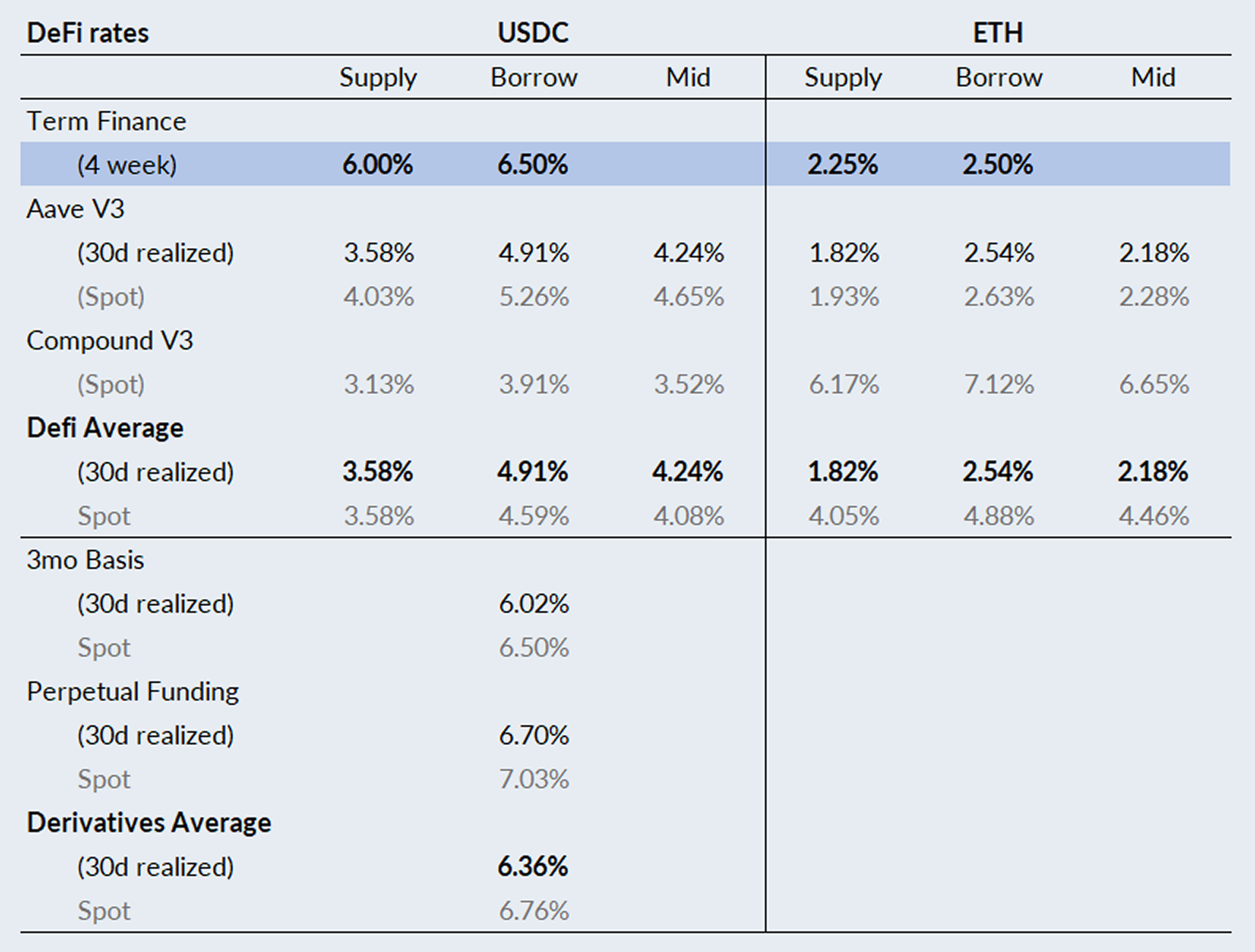

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

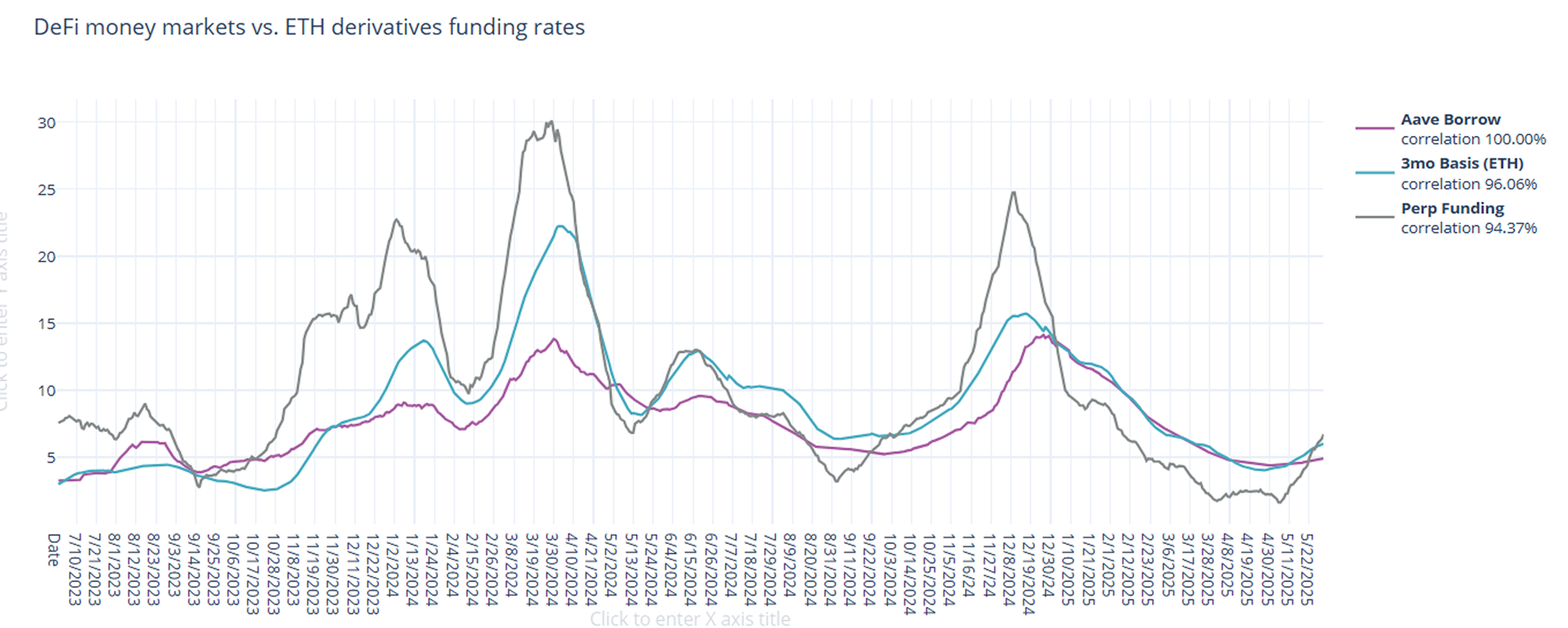

In derivatives markets, funding rates continue to rise rapidly. On a 30-day trailing basis, 3-month basis rose by +45bps to 6.02% and perpetual funding rates rose to 6.70%, up +134bps from the week prior.

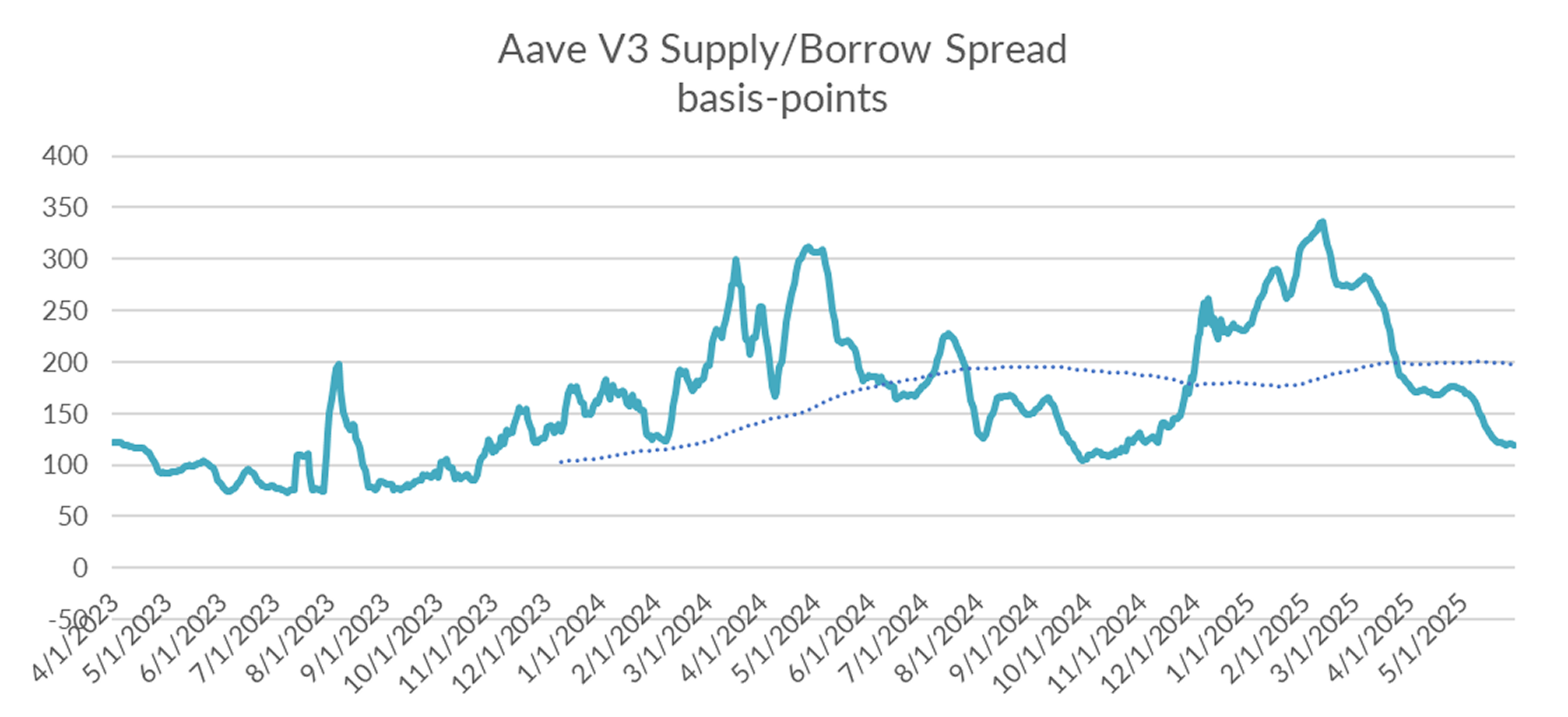

DeFi rates also rose, but at a much slower pace, causing the spread between DeFi and derivatives to continue to narrow back toward historical norms.

Zooming in on price action over the past seven days, derivatives rates mirrored the broader crypto asset market, pulling back from extremes seen last week. Until a solid rally materializes, rates are likely to stabilize at current levels.

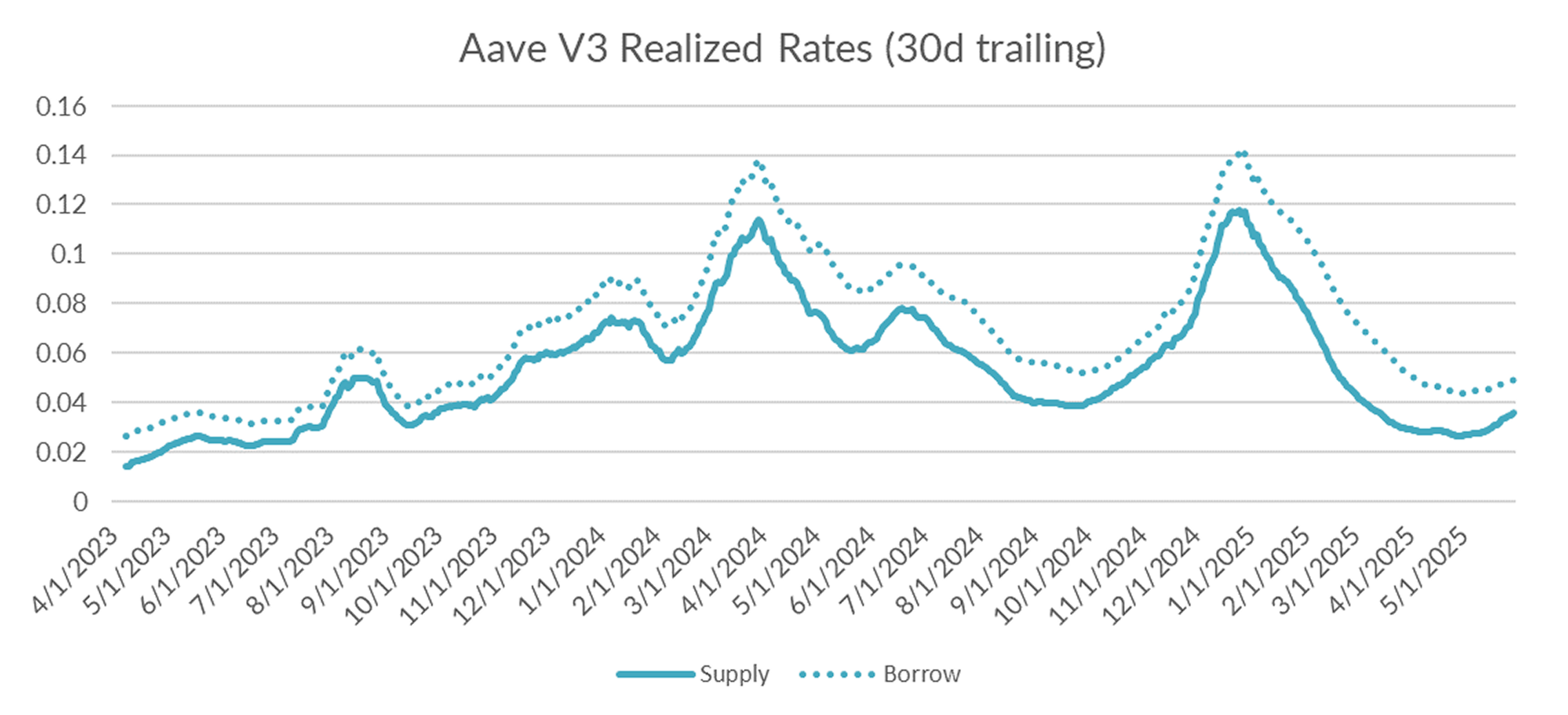

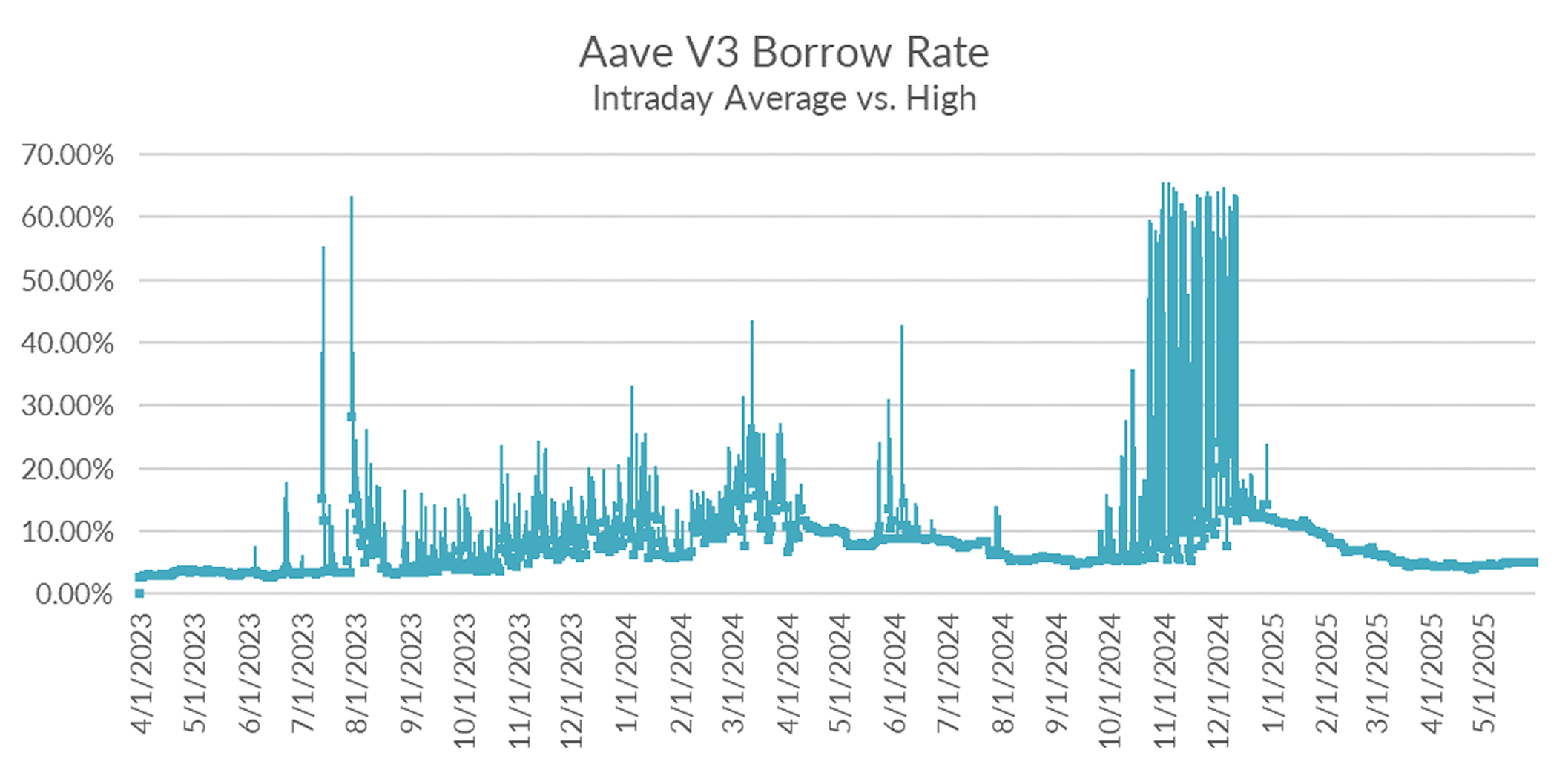

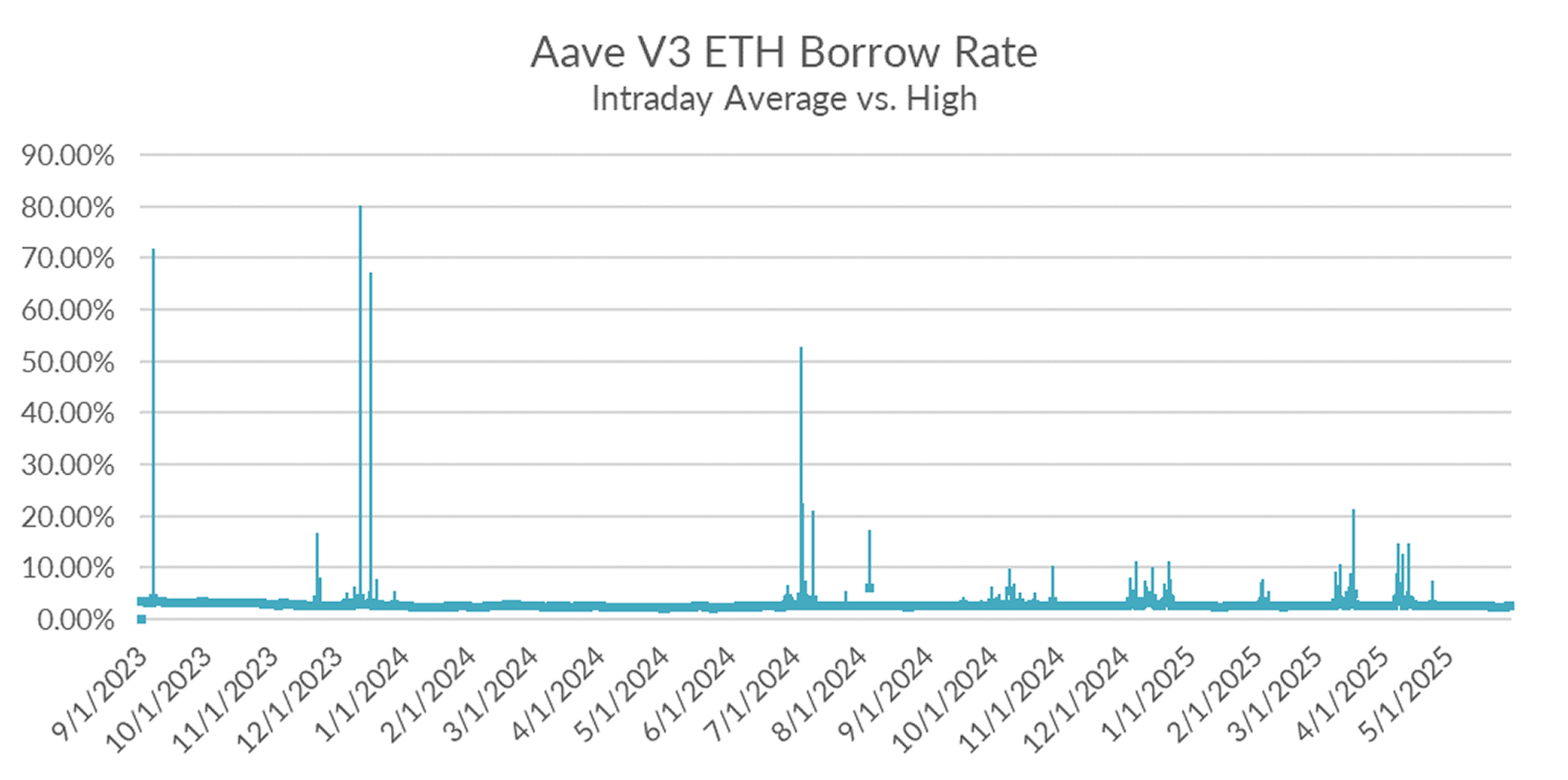

Turning to DeFi variable rate markets, the 30-day trailing average rose +15bps on the week to 4.91%. Over a shorter lookback period (just seven days), Aave borrow rates averaged 5.09% on the week, suggesting limited gains ahead.

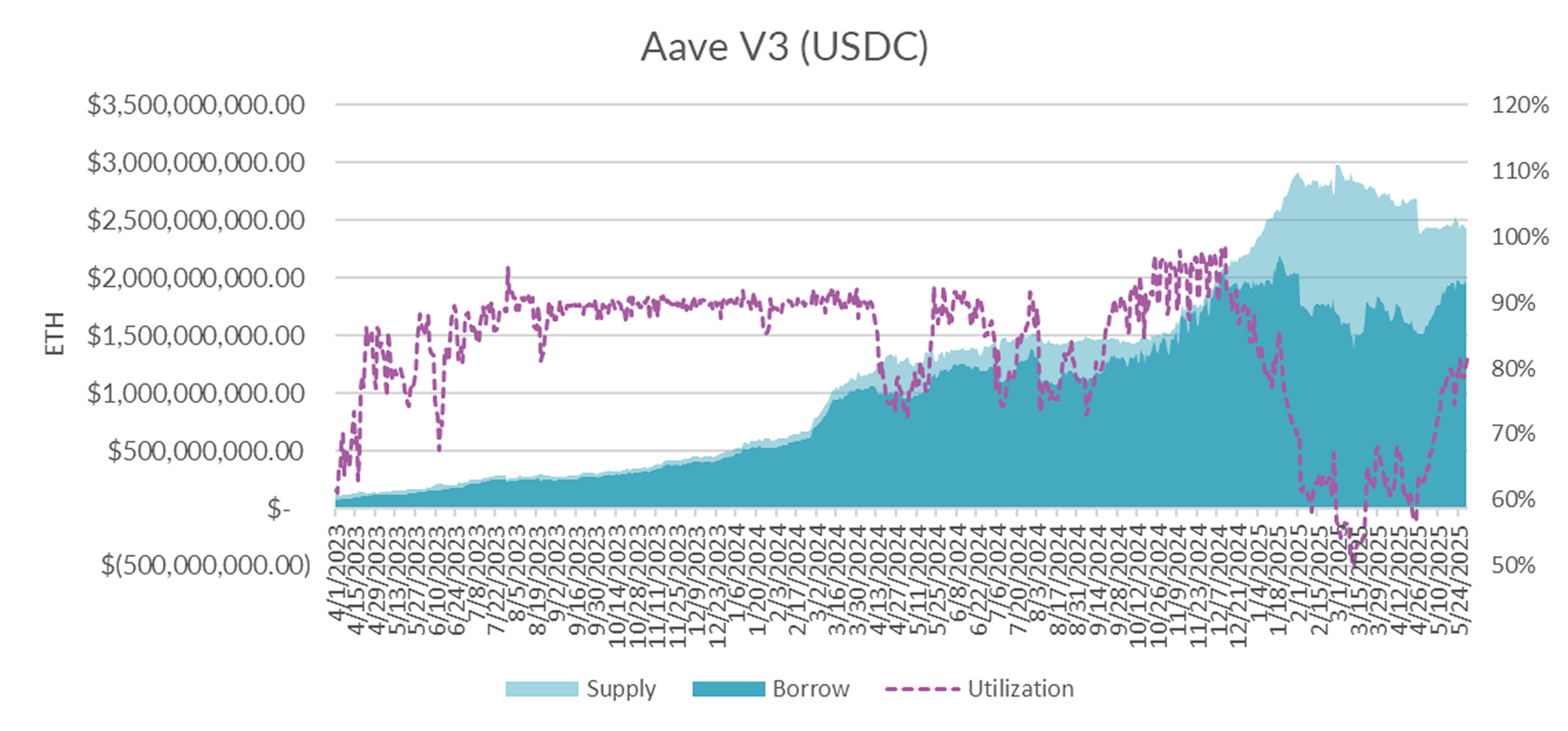

Diving into the microstructure of Aave's USDC markets, utilization held steady at a local peak around 80%, with elevated rates largely driven by a decline in total supply of around -58M USDC.

This withdrawal of excess supply has been beneficial for remaining lenders, keeping yield dilution from unutilized supply down near recent lows.

Yet despite this declining supply, overall rates remain relatively stable.

With perpetual rates coming off recent peaks, expect DeFi rates to remain relatively steady in the near term.

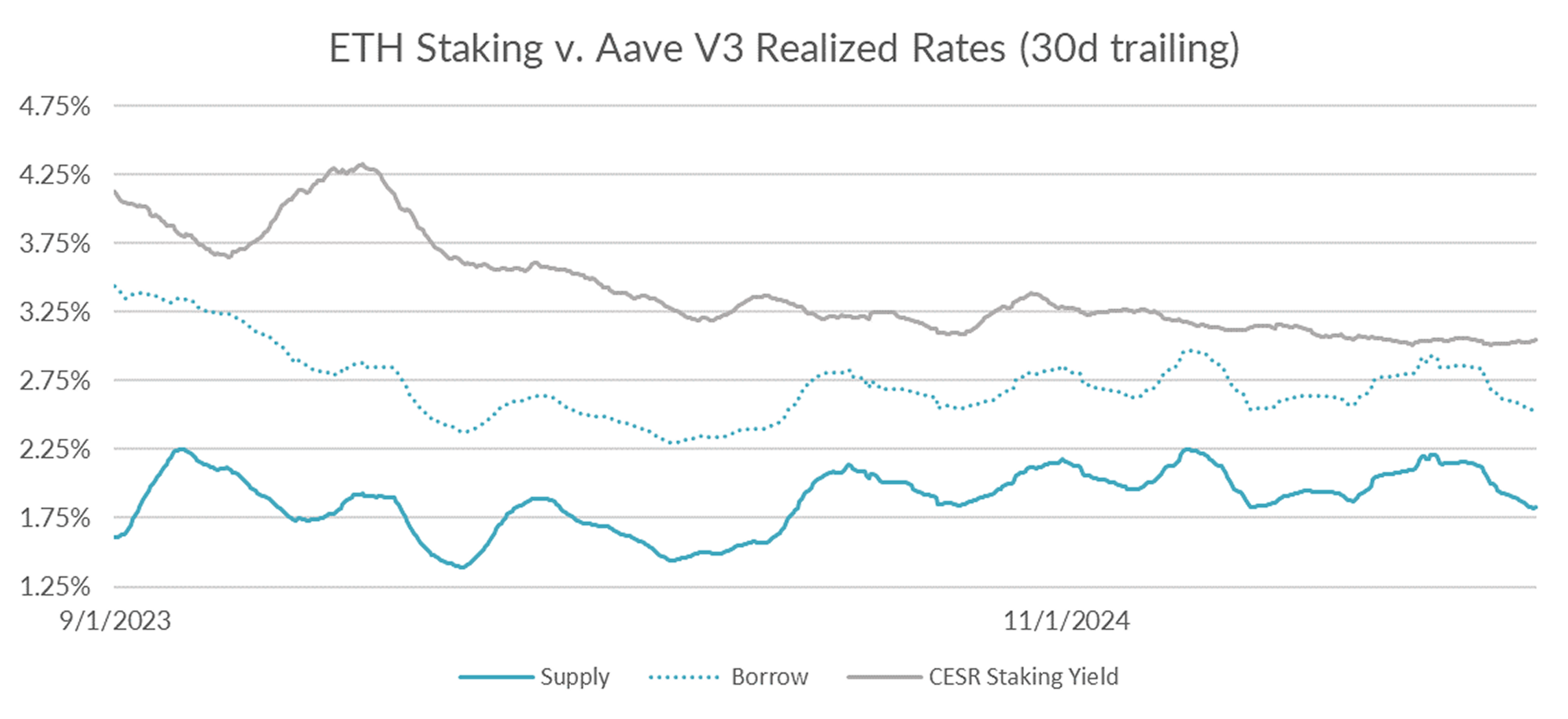

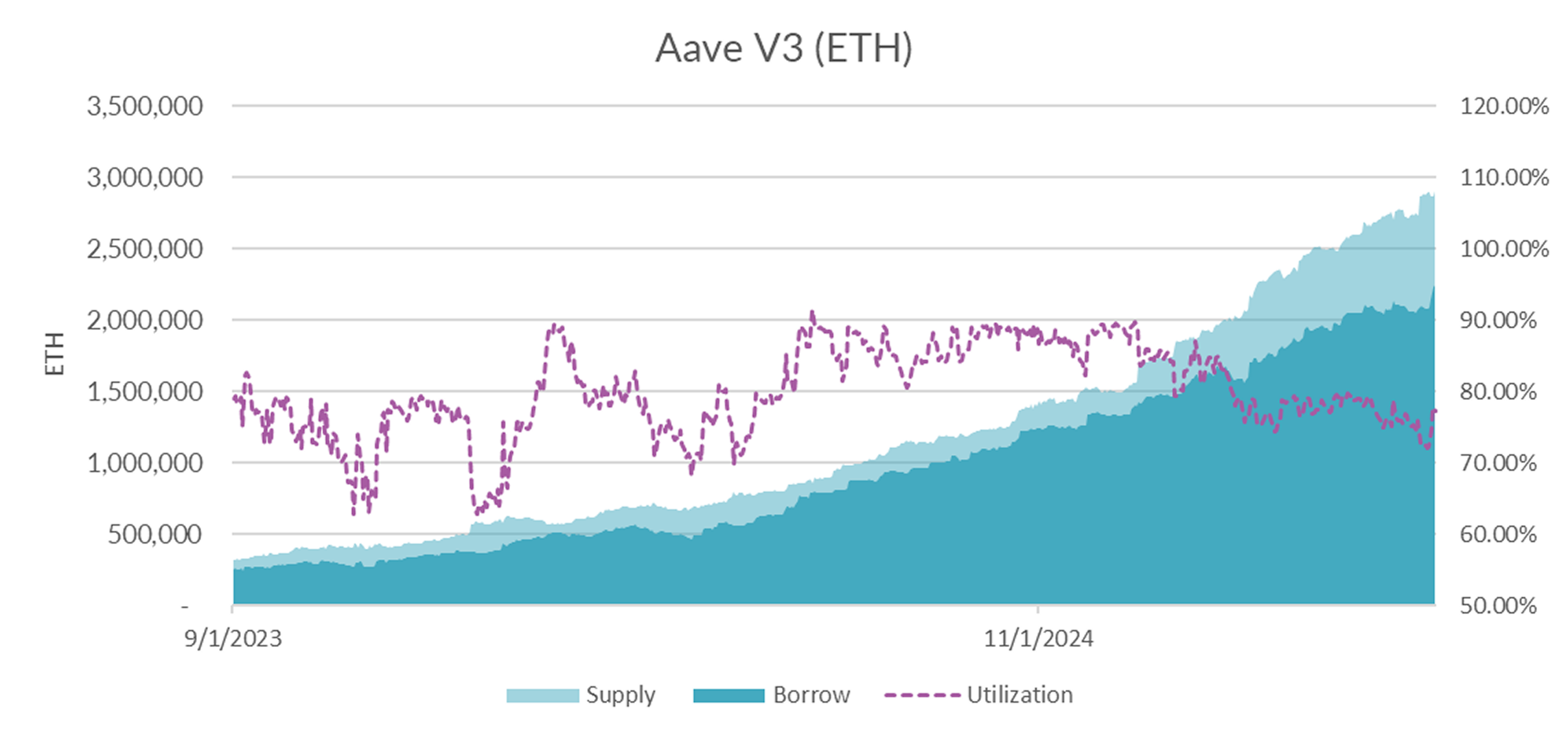

Turning now to ETH markets, ETH rates accelerate to the downside, falling by -4bp on the week to 2.54% on a 30-day trailing basis. The CESR staking index, on the other hand, rose slightly to 3.04%, widening the spread by +5bp on a 30-day trailing basis.

Market internals show that demand (+146k ETH) rose materially faster than supply (+32k ETH) over the past two day, with utilization bouncing back toward recent norms.

This recent pickup in demand suggests that ETH lending markets may have found a bottom in the near term.

Indeed, compound ETH markets are currently yielding 6%+, suggesting some market rotation underway. It would not be surprising to see that demand migrate over to Aave in coming days.

BTC came off new high last week to close down around ~104k. Overall, market volatility appears to be on the decline and markets settling into a range. Absent large external stimulus, expect asset prices and DeFi rates to remain rangebound in the near term.