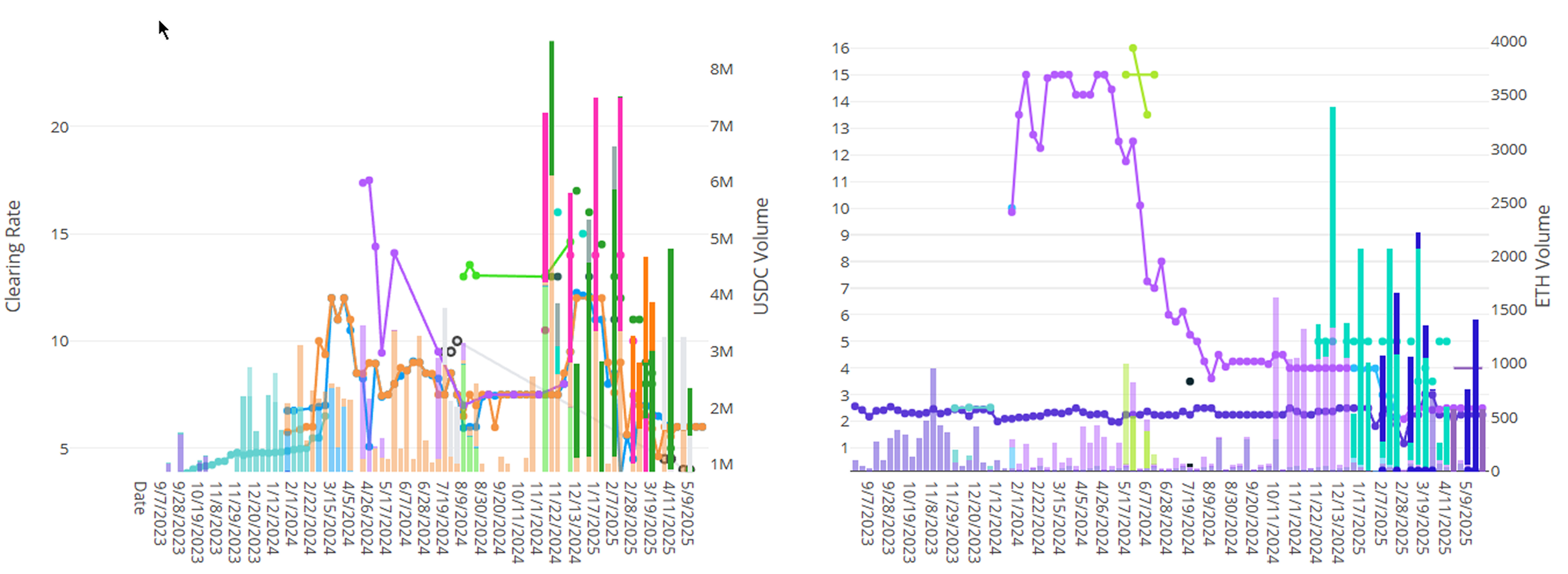

Term cleared around ~2M in volume this week, with volumes driven primarily by ETH loans against superETH and hinkalETH collateral. Overall ETH rates against exotic collateral remain robust and steady on Term.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

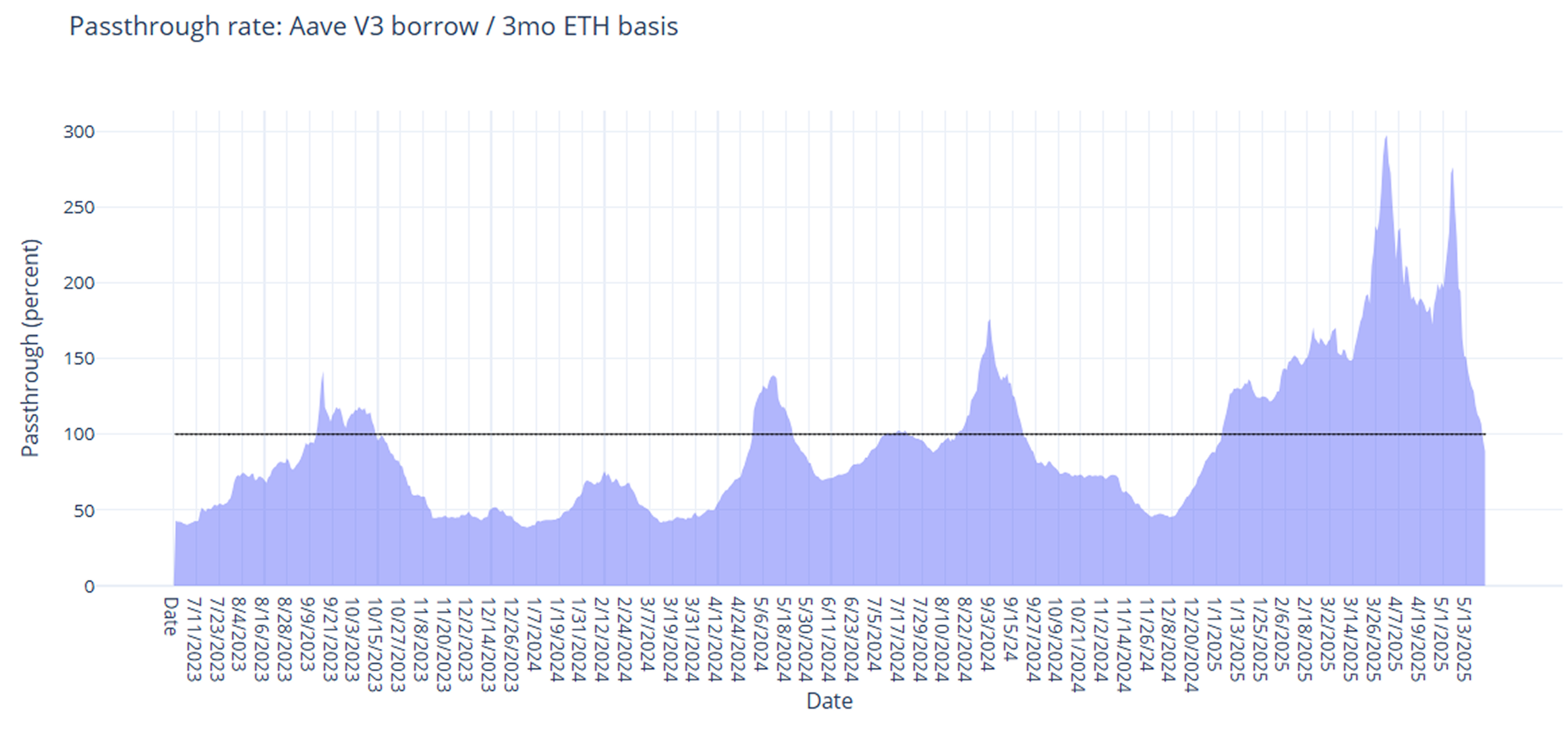

In derivatives markets, funding rates continue to accelerate to the upside. On a 30-day trailing basis, 3-month basis rose by +68bps to 5.60% and perpetual funding rates rose to 5.35%, up +189bps from the week prior.

DeFi rates held steady on the week, rapidly narrowing the spread between DeFi and derivatives rates back toward historical norms.

With BTC breaking new highs this past week, expect funding rates to continue to pick up as the market fomos levered longs.

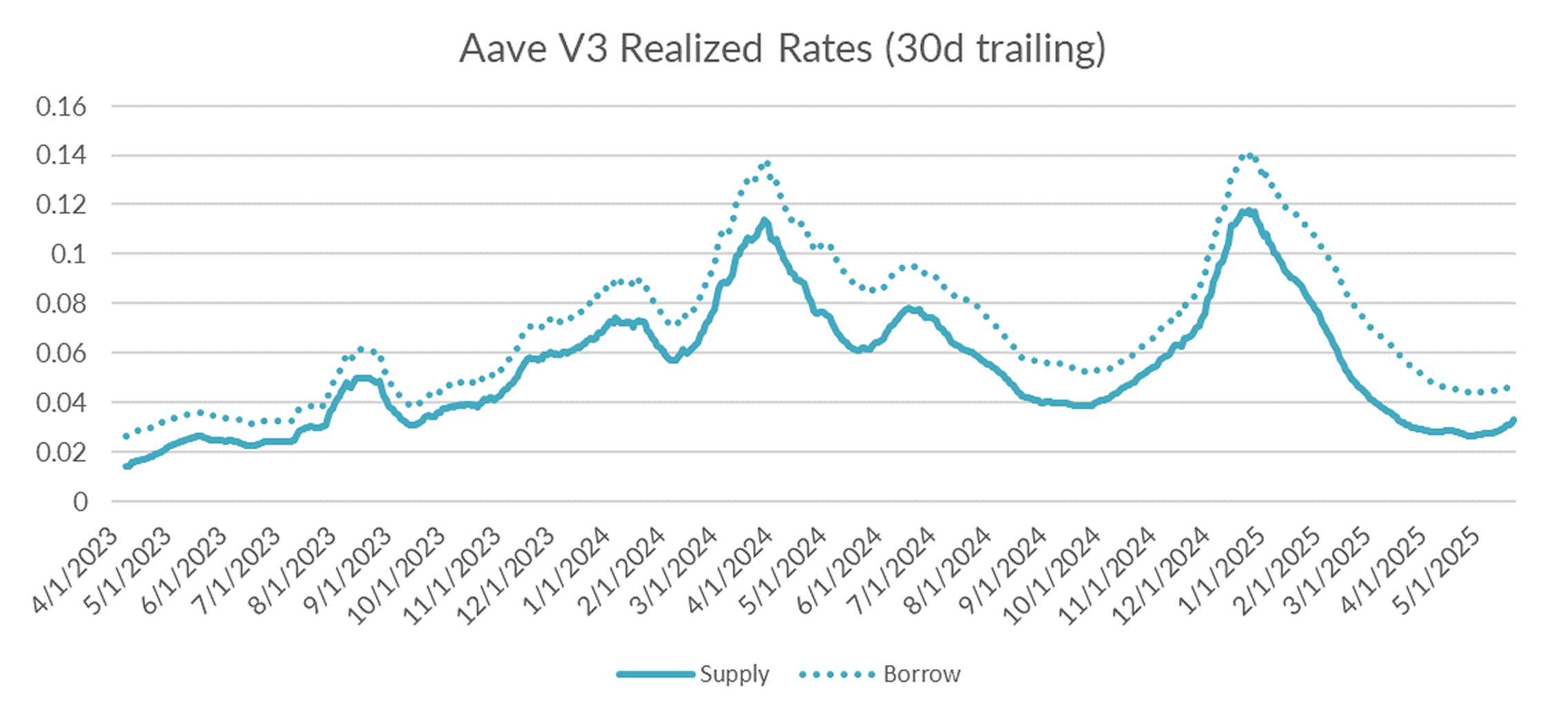

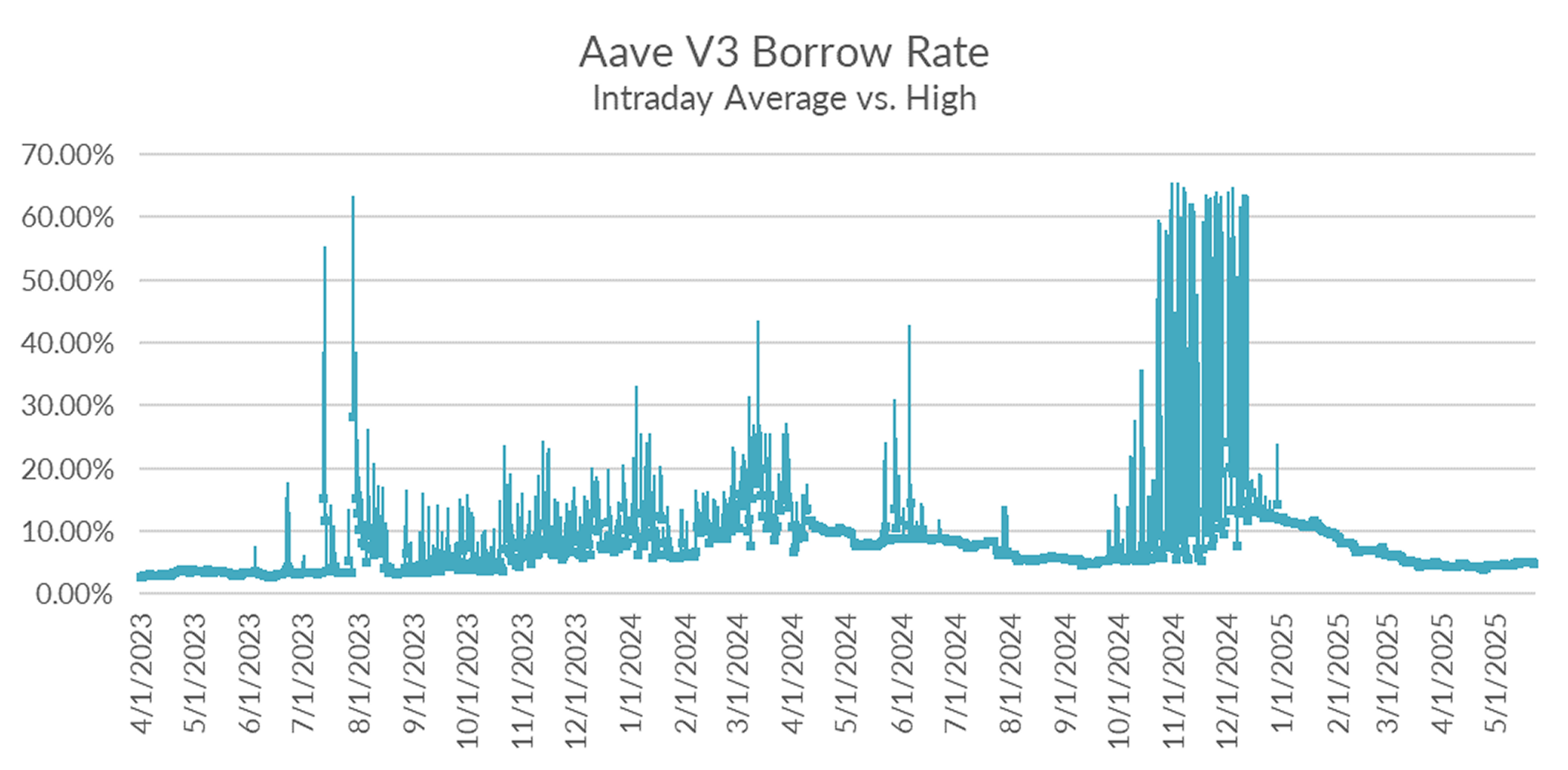

Turning to DeFi variable rate markets, the 30-day trailing average rose +22bps on the week to 4.75. Over a shorter lookback period (just seven days), Aave borrow rates averaged 5.04% on the week, suggesting further gains ahead.

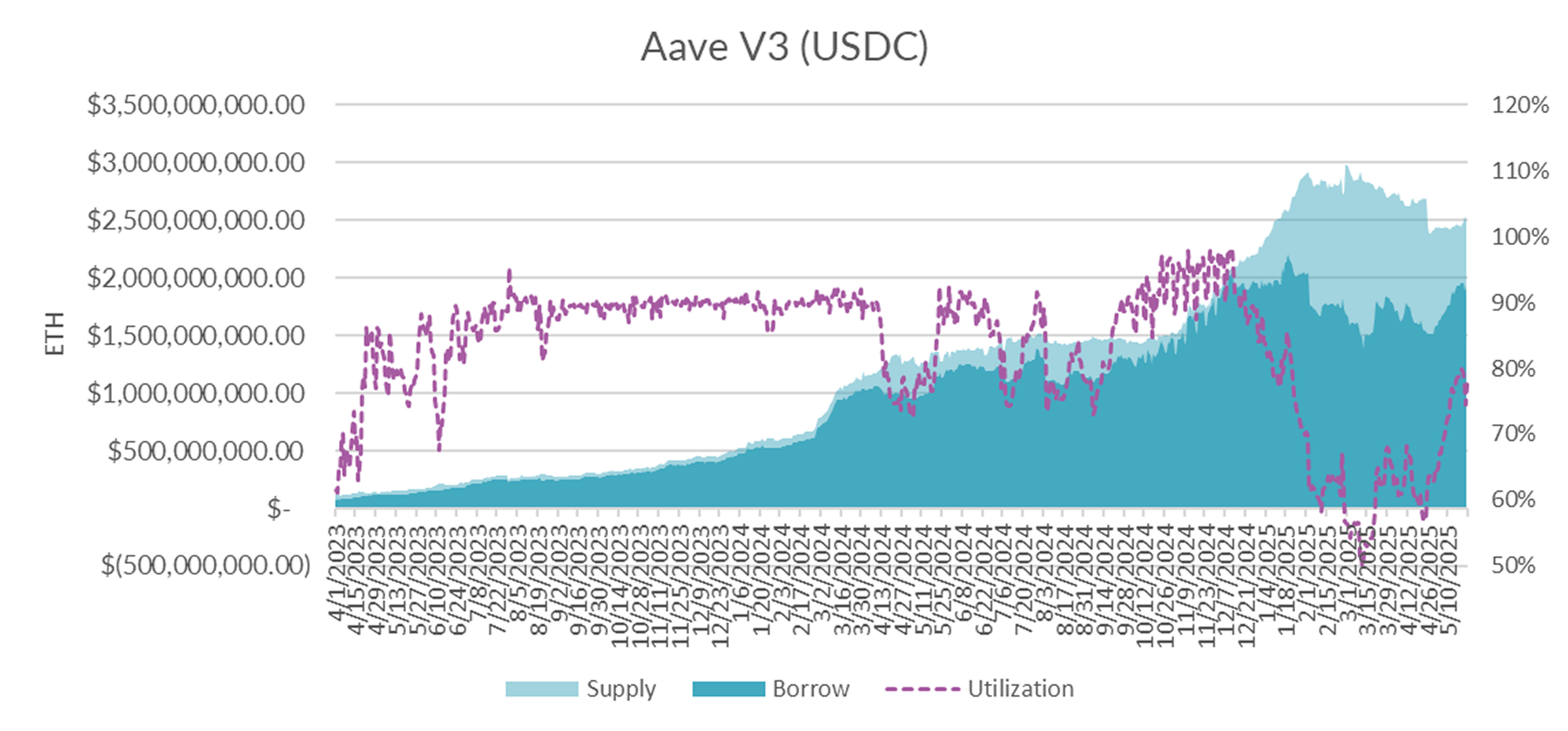

Diving into the microstructure of Aave's USDC markets, utilization held steady at a local peak around 80%—but appears to be lagging funding rate spikes observed in derivatives markets.

With funding rates only just beginning to flip higher than defi funding rates, expect spillover to raise DeFi rates in the coming weeks.

And as utilization rises, supply/borrow spreads should continue to decline.

While derivatives funding rates have surged, they had fallen so low that only recently have they moved above DeFi lending rates. This lag helps explain the muted response in DeFi yields—though a sustained divergence could prompt DeFi rates to reprice. Keep an eye on funding rates over the next week or so .

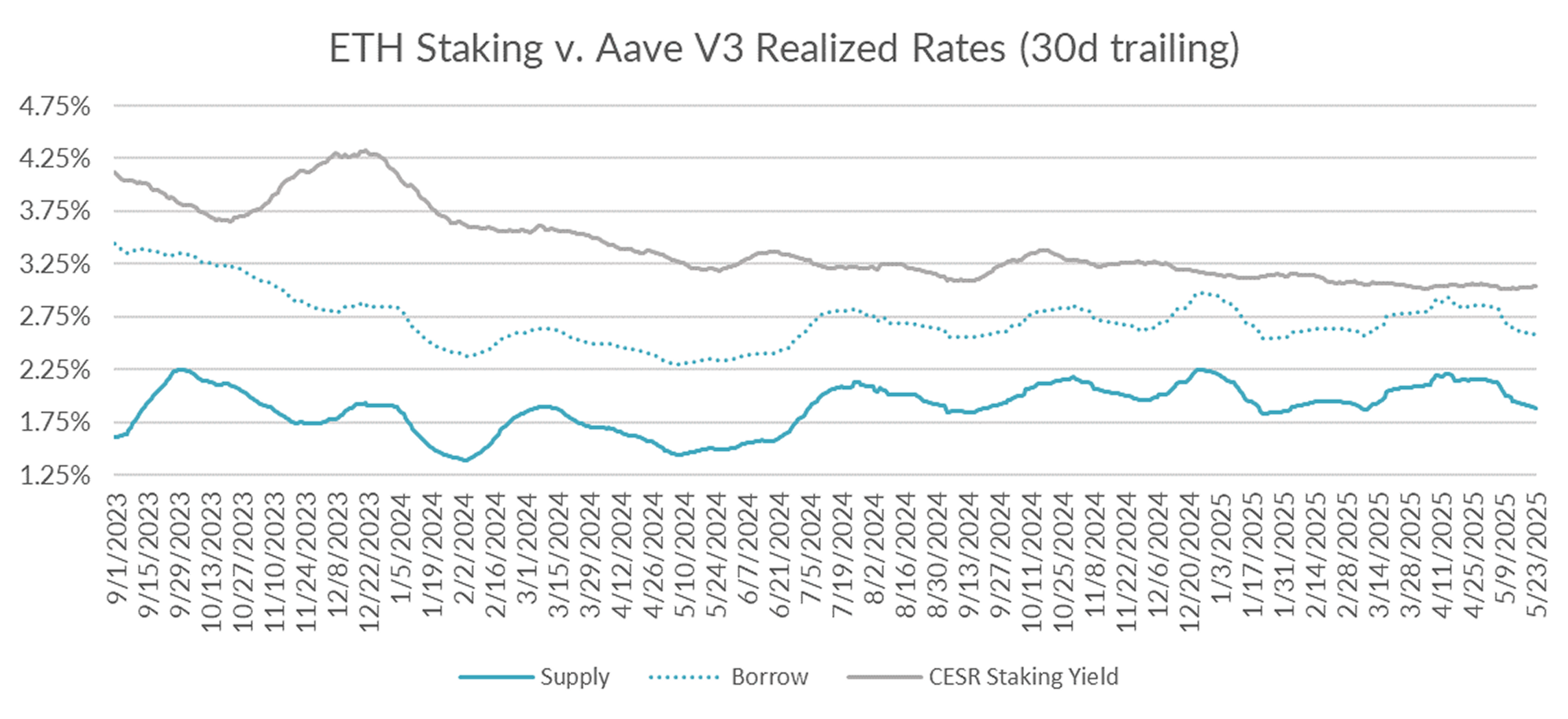

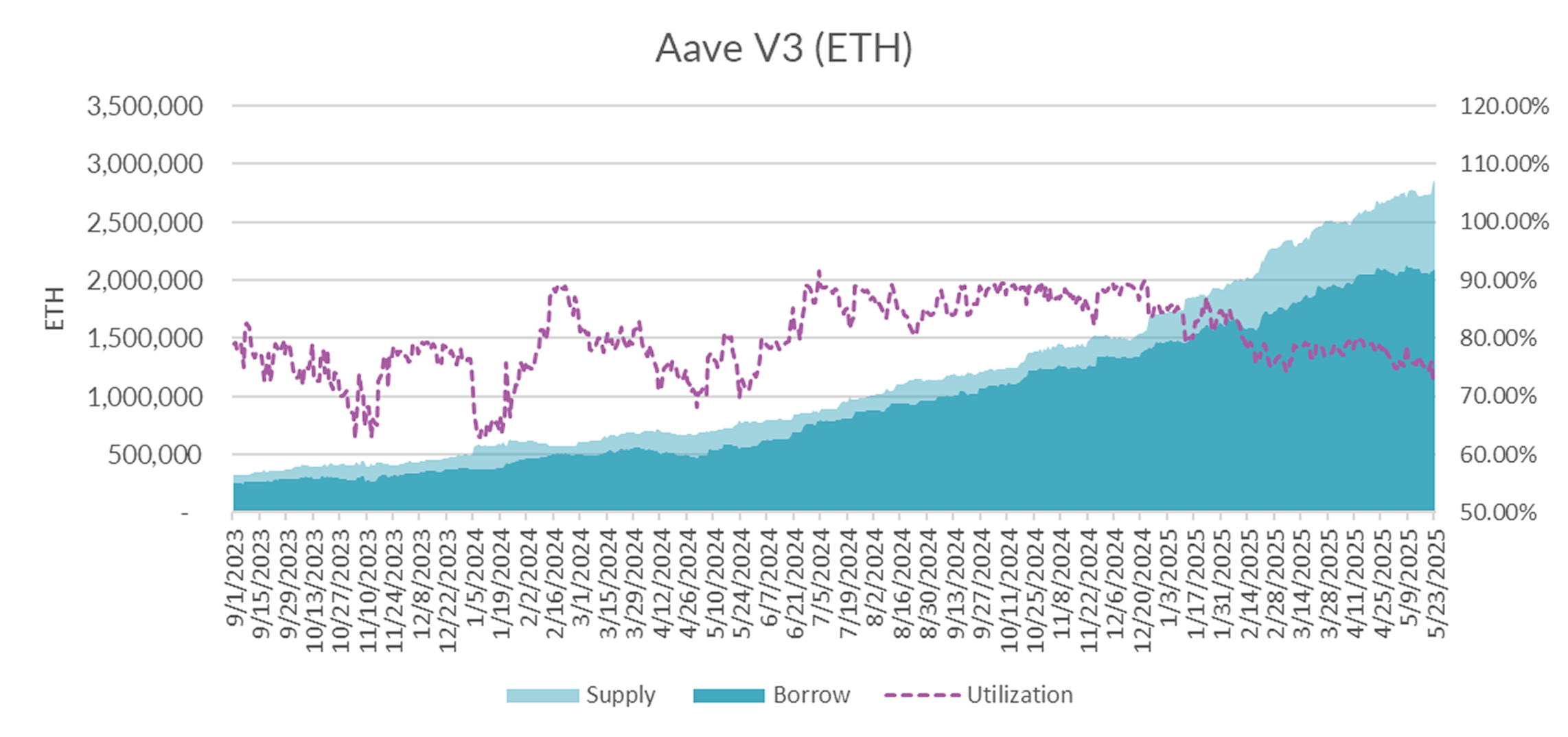

Turning now to ETH markets, ETH rates continue to decline, albeit at a slower pace, falling by -3bp on the week to 2.58% on a 30-day trailing basis. The CESR staking index, on the other hand, rose slightly to 3.01%, widening the spread by +4bp on a 30-day trailing basis.

Market internals show that demand (+38k ETH) rose materially slower than supply (+120k ETH), with utilization on a trend that looks more and more decidedly downtrend.

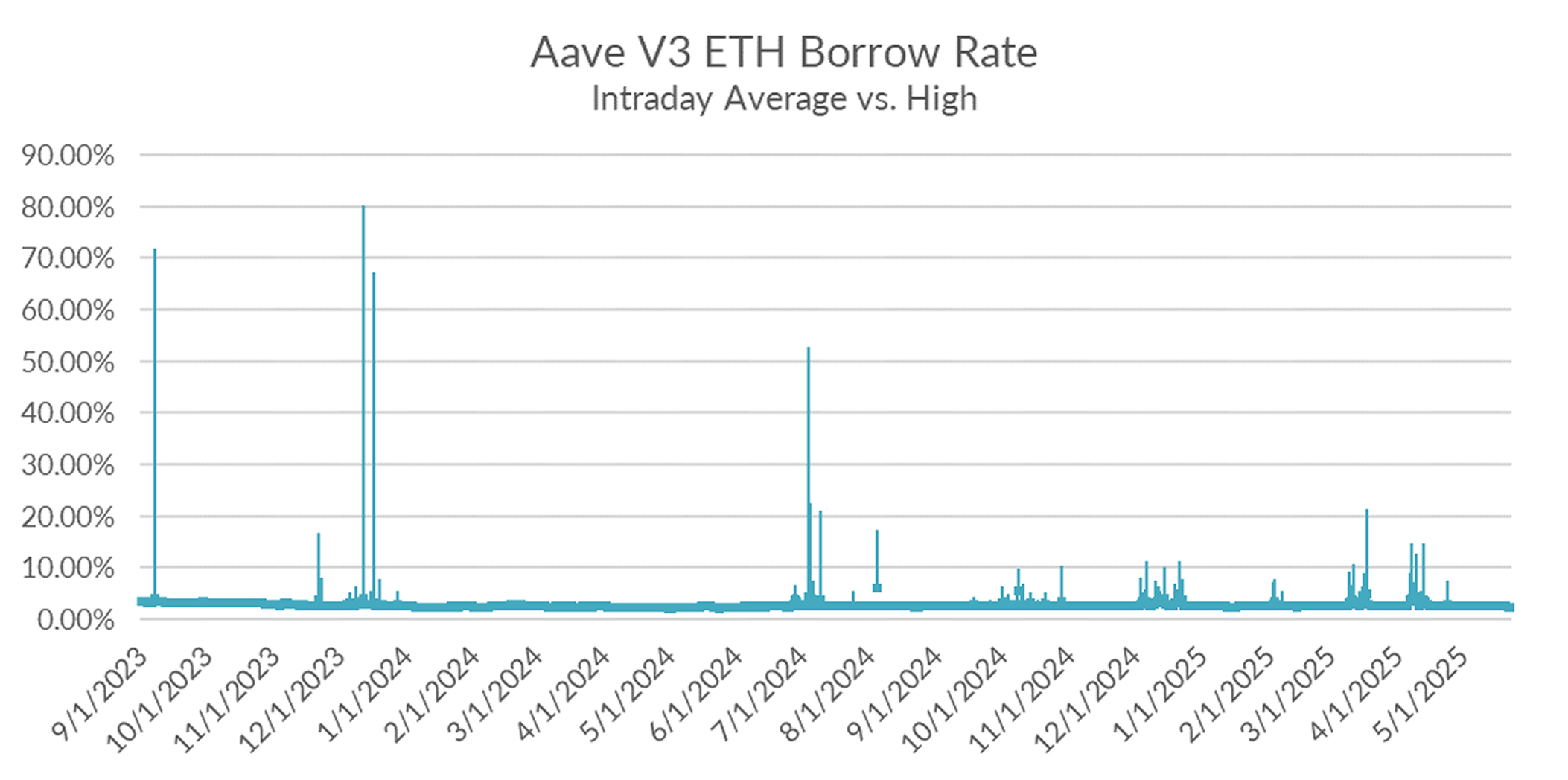

And intraday and intraweek volatility remained low with no kink driven spikes throughout the past week.

Lower ETH rates are commonly associated with bull markets. Should new highs in BTC continue to hold, expect ETH rates to decline further in the near term.

BTC made a run through all-time highs of ~108k and close the week just above the prior peak. Analysts suggest a confirmed breakout could occur if BTC closes above 108K for two consecutive weeks—potentially driving renewed activity in DeFi lending markets.