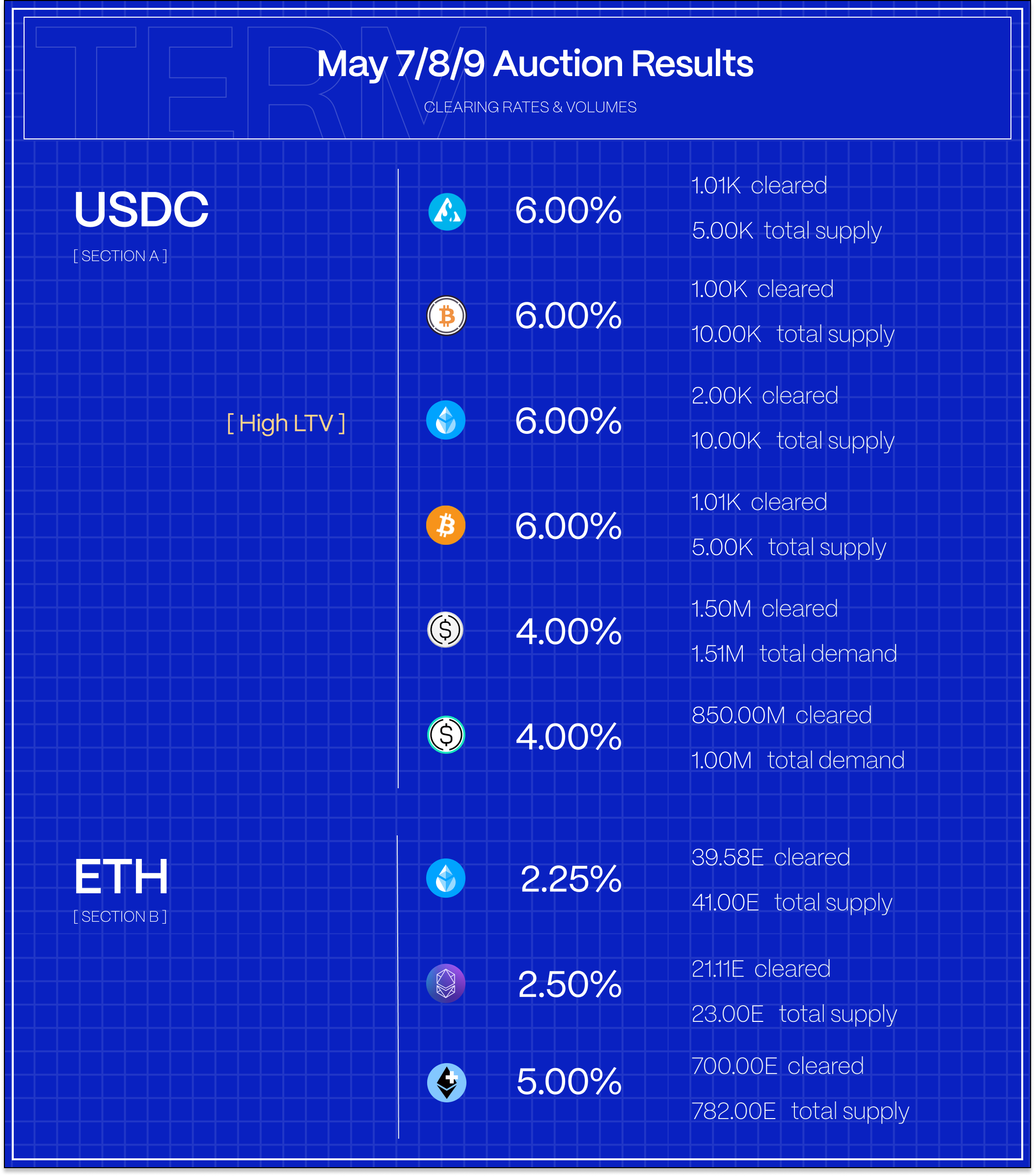

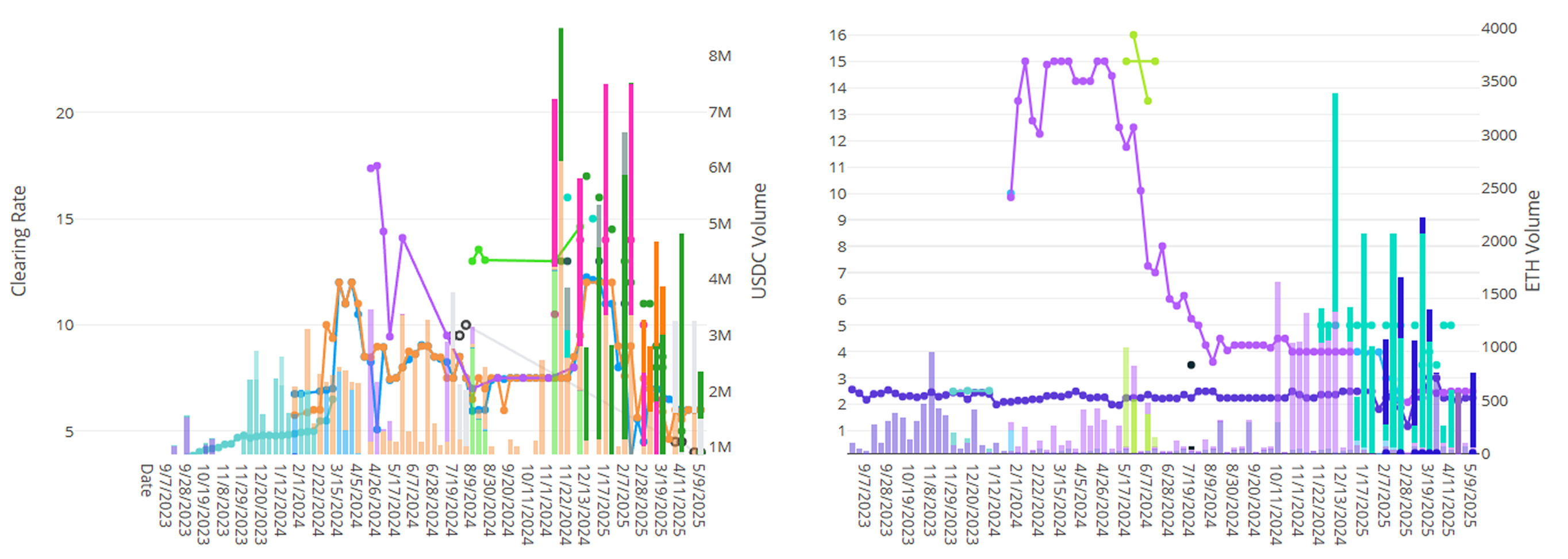

Term cleared ~3.9M in volume this up from 3.4M the week prior. Volumes were split with a slight bias in favor of USDC over ETH. Overall rates remain subdued but given this week’s rally we expect rates to pick up in the near term.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

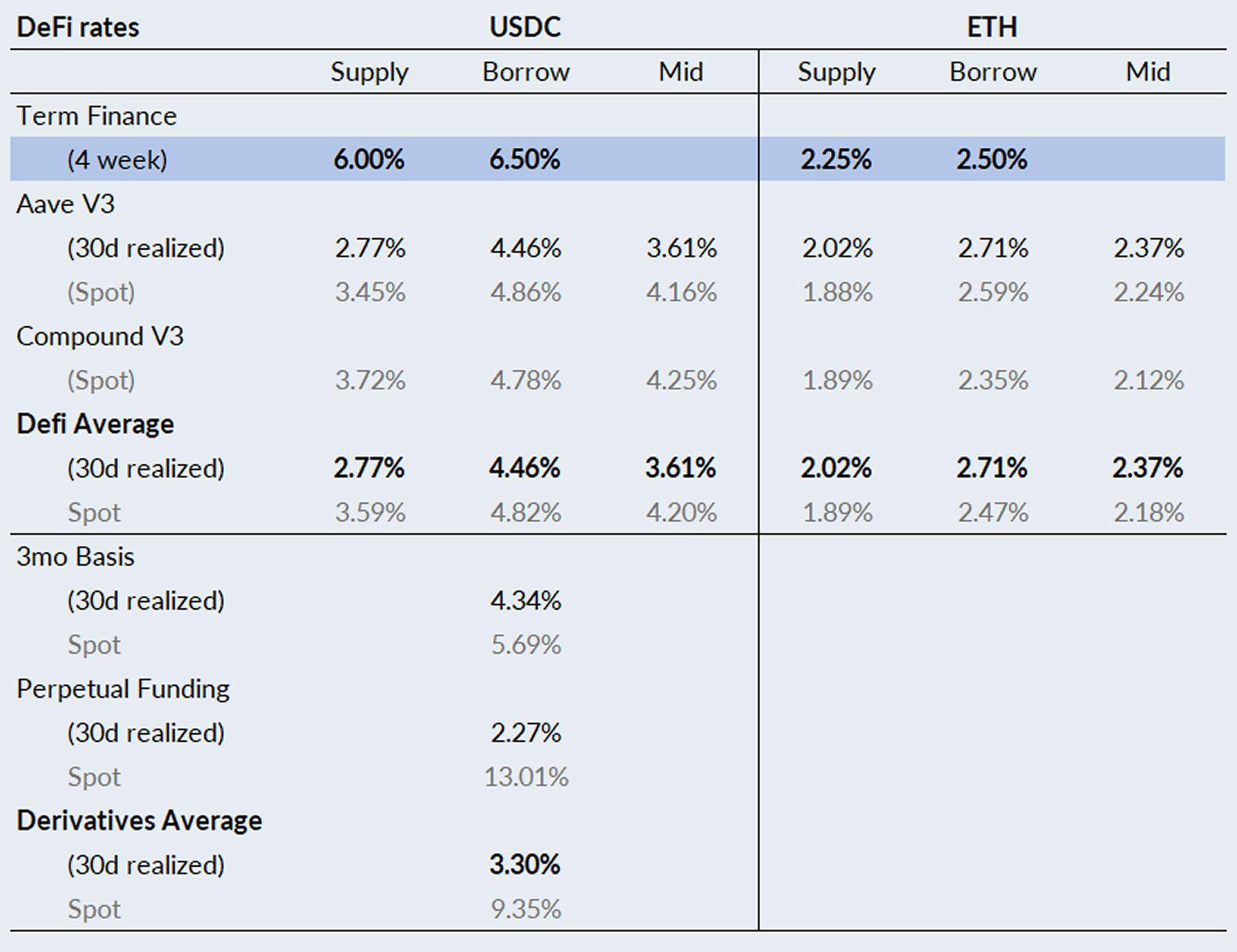

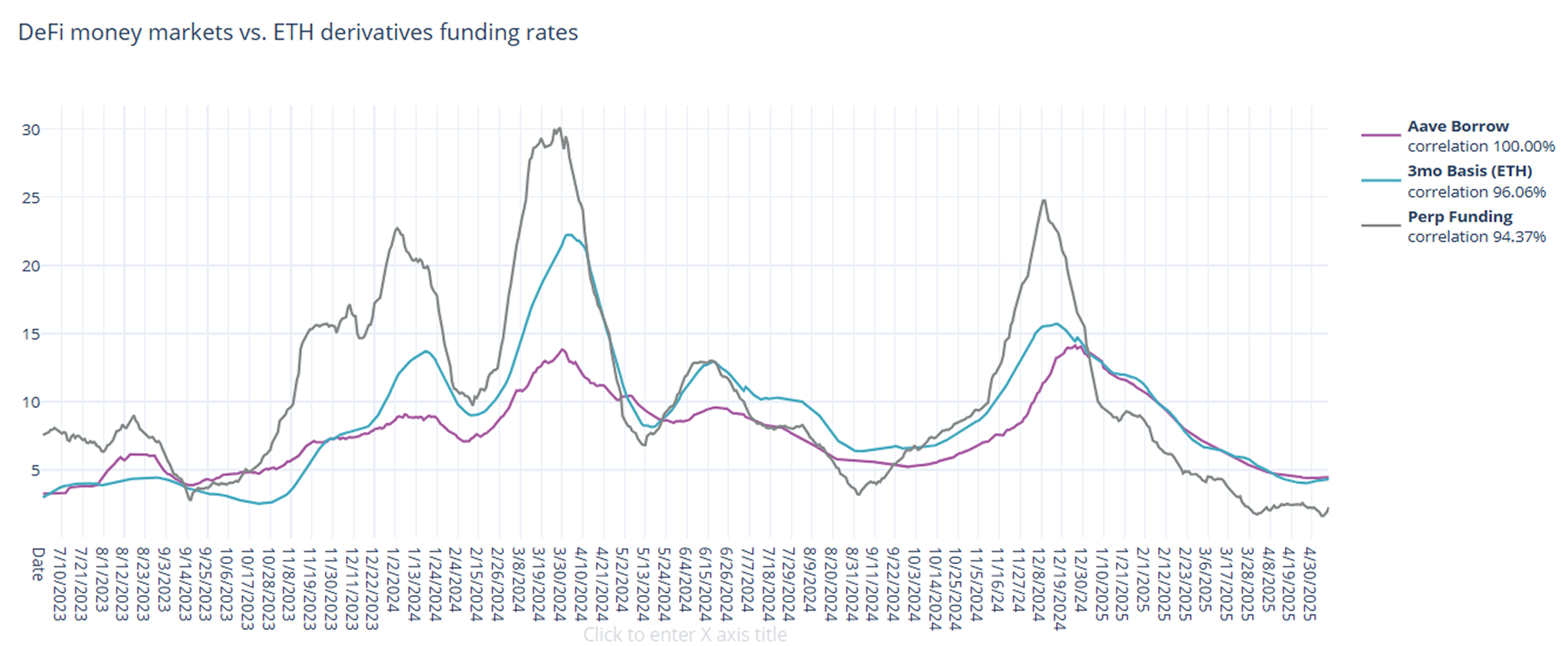

In derivatives markets, funding rates were mixed but ended the week sharply higher with perp rates printing in double digit territory for the first time since February. On a 30-day trailing basis, 3-month basis rose by +15bps to 4.34% and perpetual funding rates rose to 2.27%, up +17bps from the week prior.

DeFi rates held steady on the week, narrowing the spread between DeFi and derivatives rates by roughly -15bps.

With BTC breaking back above 100k for the first time since February and perpetual funding rates heating up into the double digits, signs of a shift in tone appears to be in the making. Should this move sustain, expect funding rates to pick up as leverage traders pile on the trade.

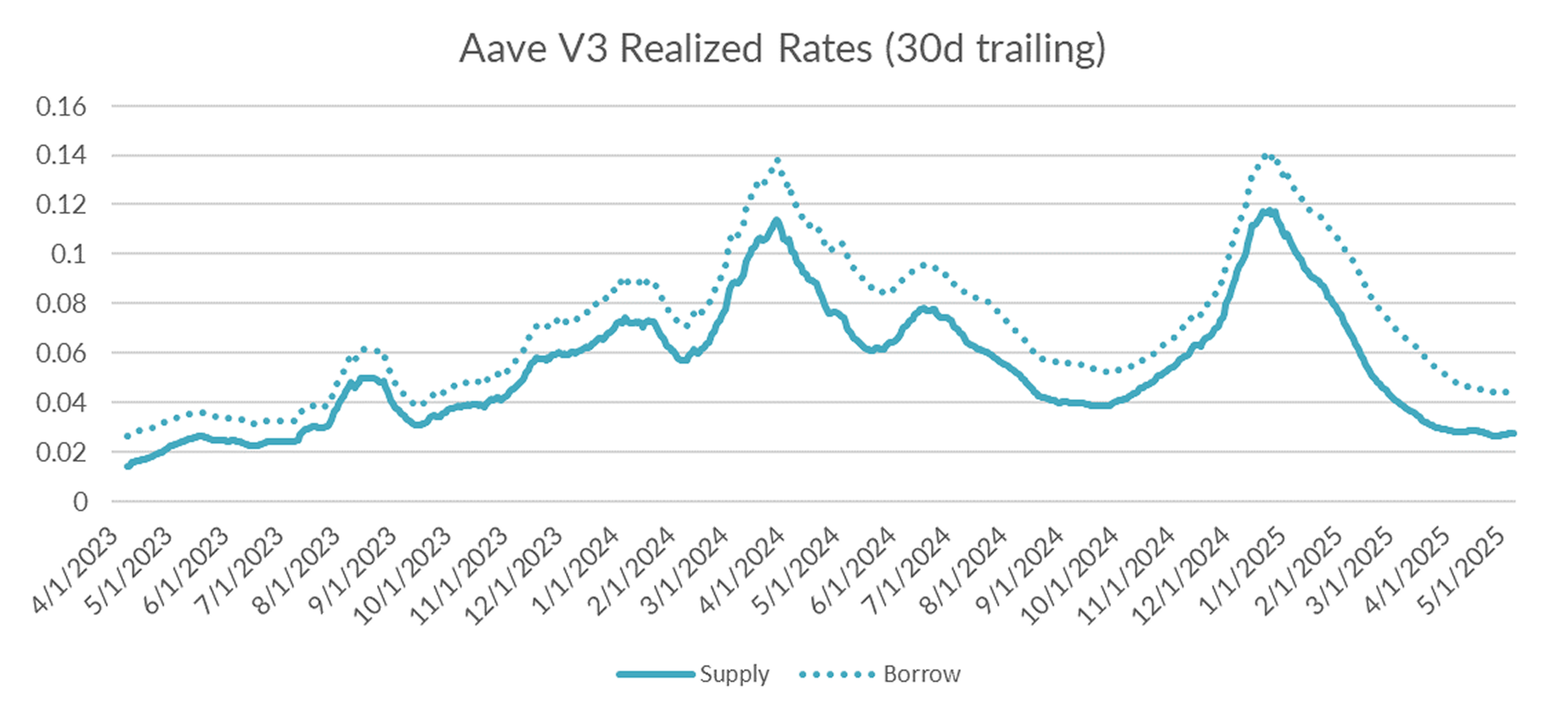

Turning to DeFi variable rate markets, the 30-day trailing average rose +1bps on the week to 4.66. Over a shorter lookback period (just seven days), Aave borrow rates averaged 4.16% on the week, suggesting consolidation ahead.

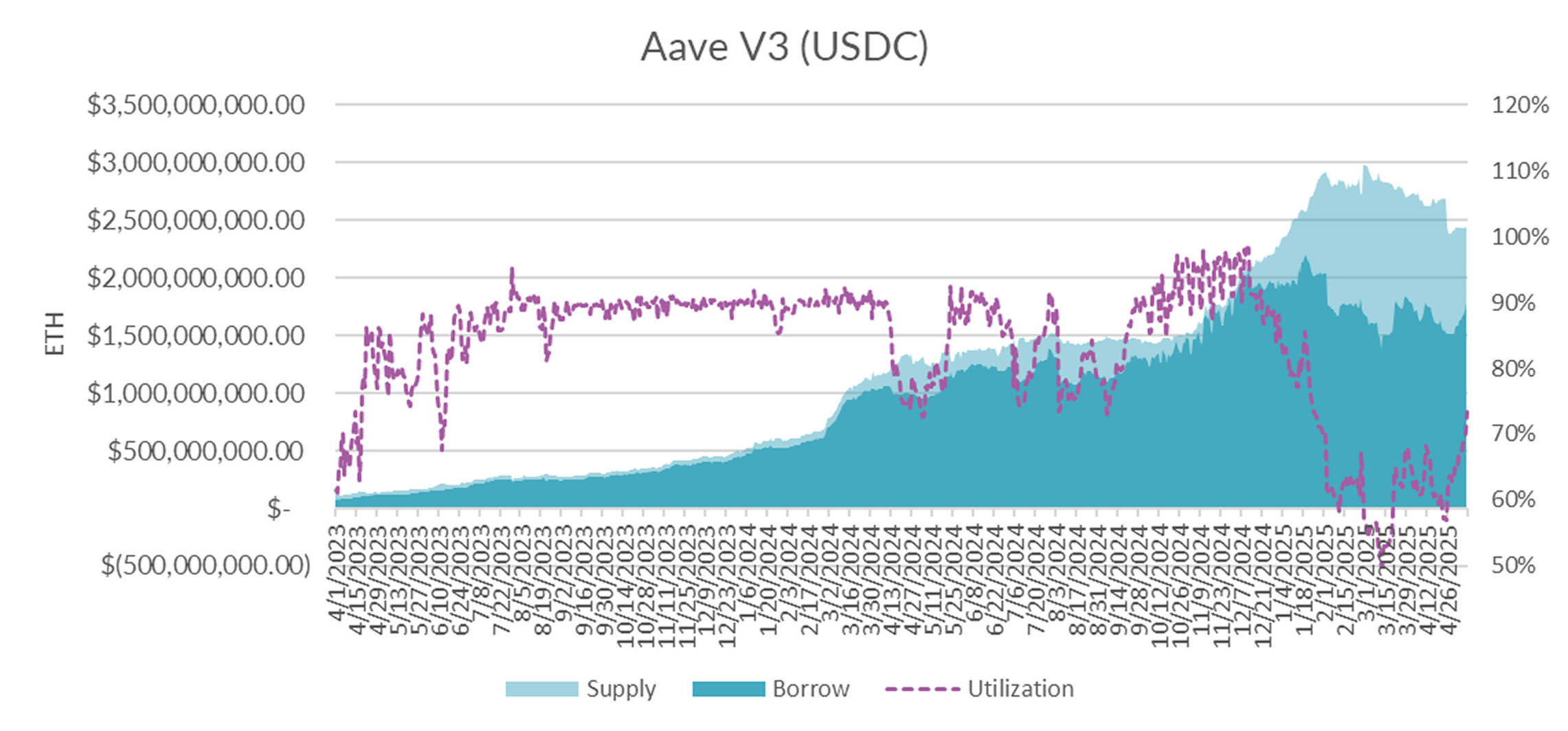

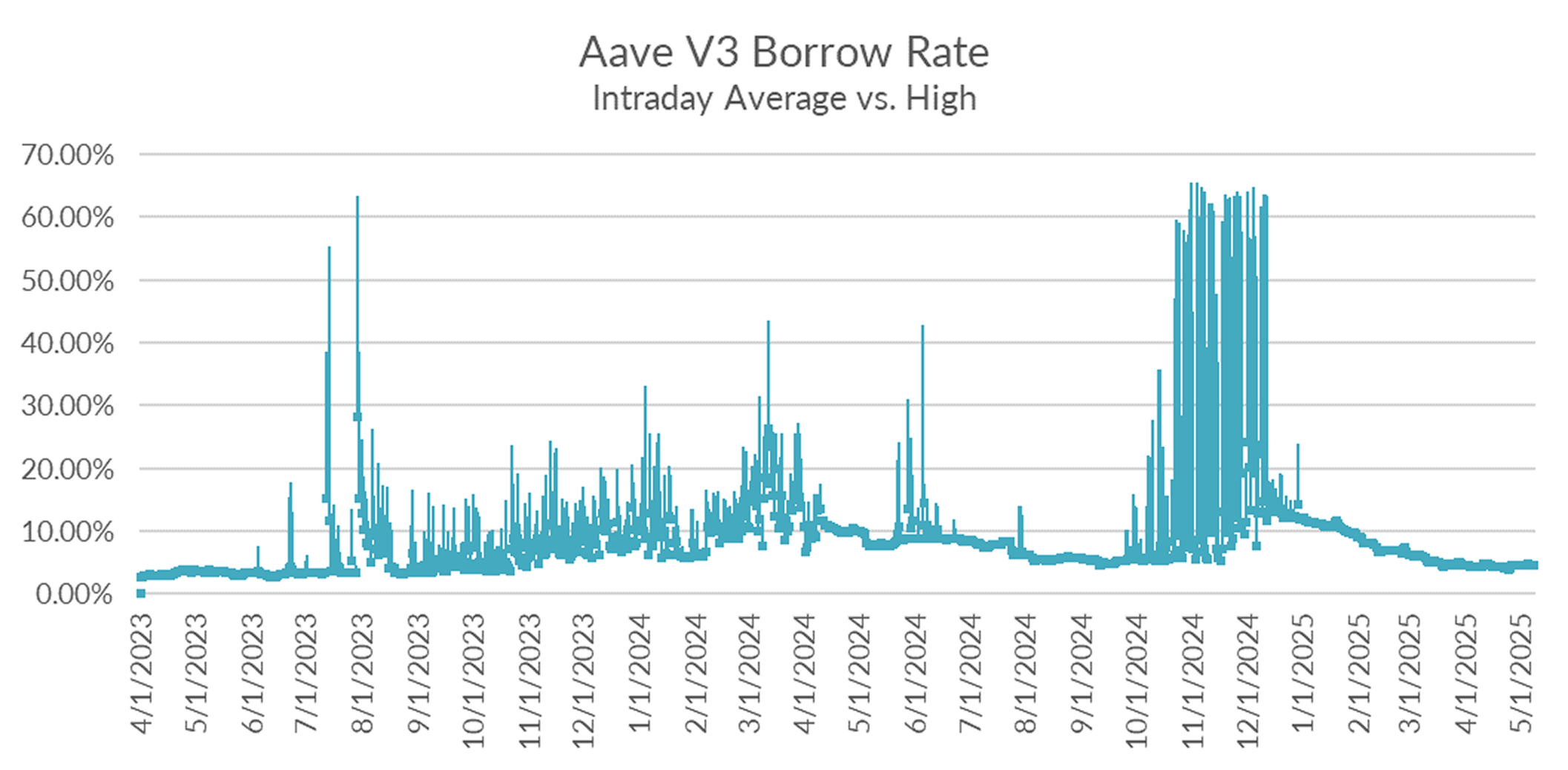

Diving into the microstructure of Aave USDC markets, utilization rose sharply into the 70s over just the past two days, consistent with the rise in perpetual funding rates into the double digits over the same period.

Should perpetual funding rates continue to rise, expect utilization and rates to pick up in the near term.

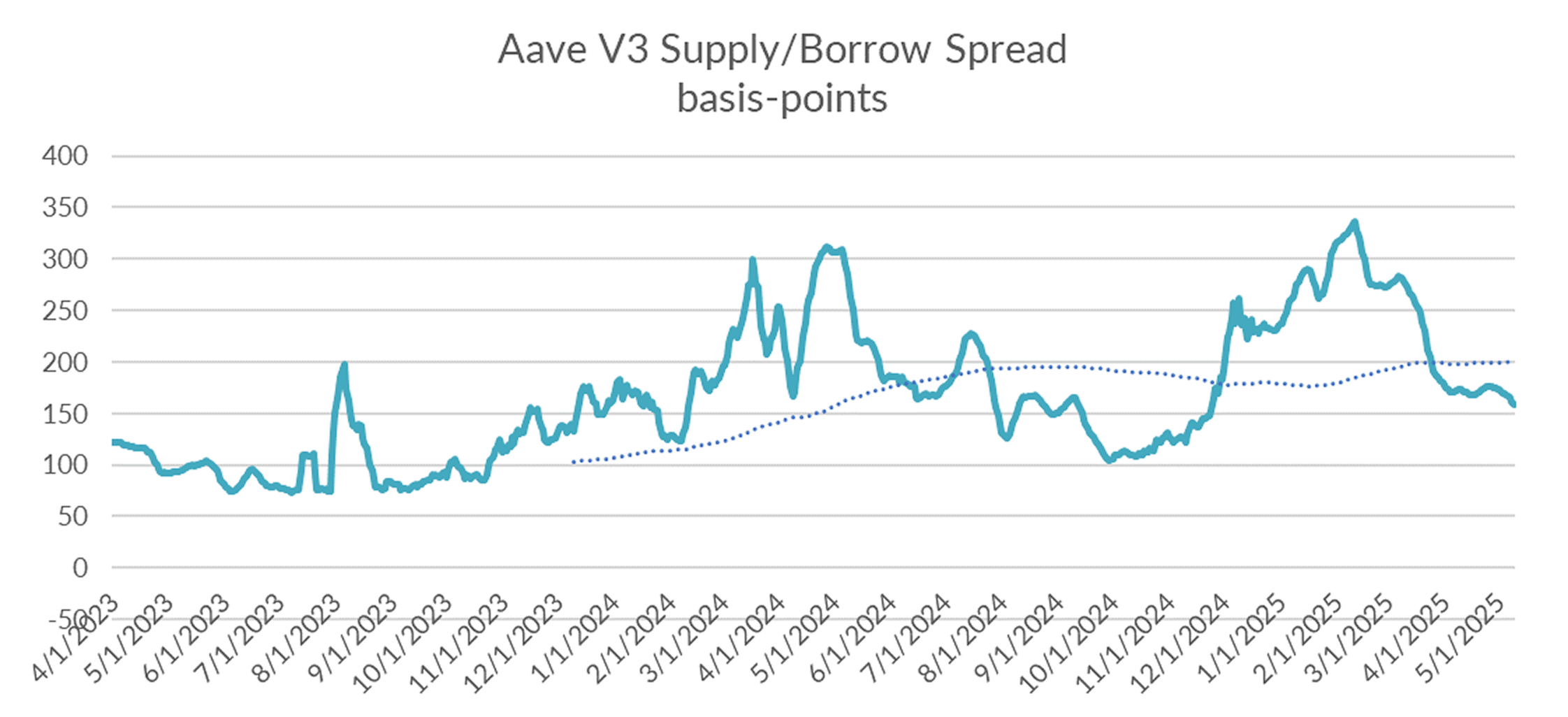

And with utilization on the rise, supply/borrow spreads should continue to decline.

Looking forward, expect DeFi rates to pick up, assuming this two day trend holds into the following week.

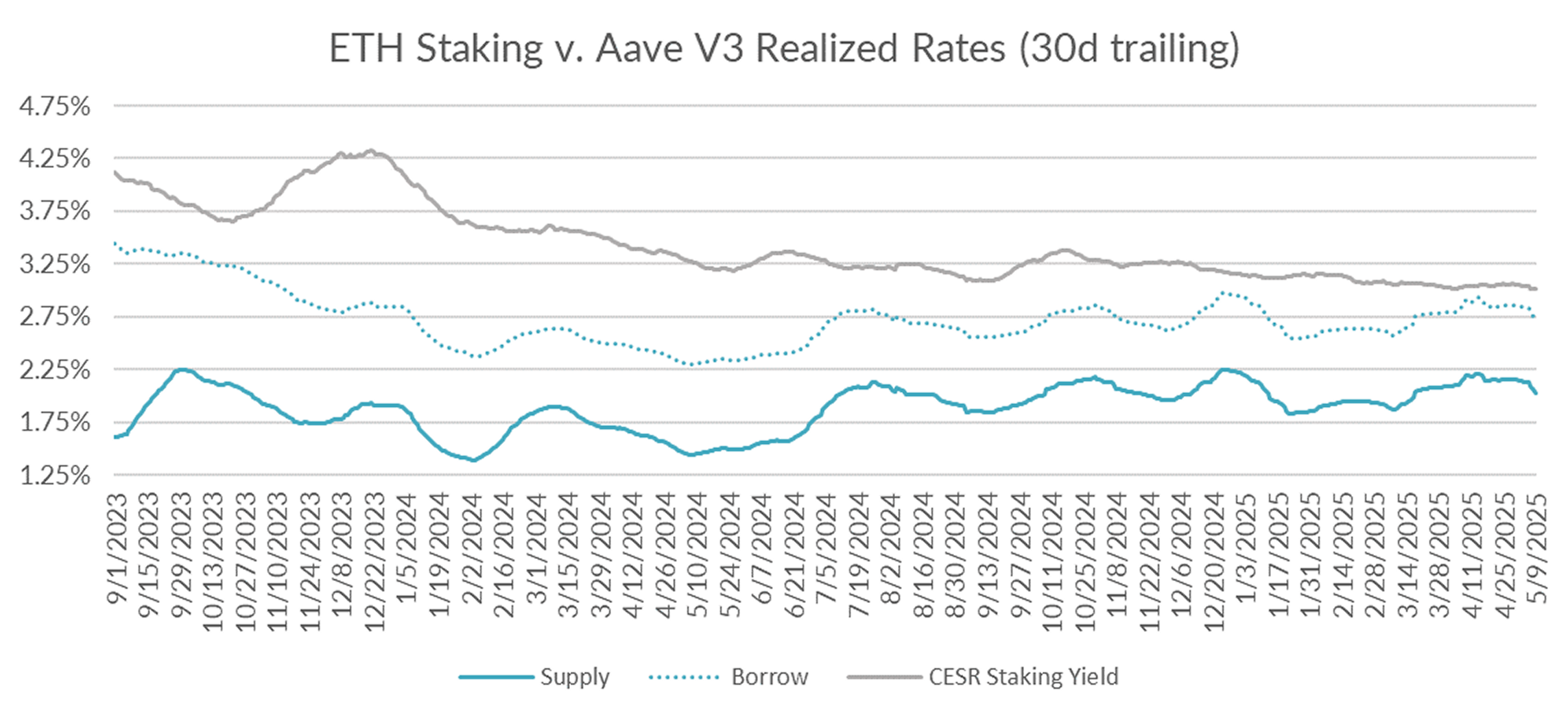

Turning now to ETH markets, ETH rates close the week significantly lower, falling by -12bp on the week to 2.71% on a 30-day trailing basis. The CESR staking index also fell, but in a more muted fashion, declining by just -4bp to 3.01%, widening the spread by +8bp on a 30-day trailing basis.

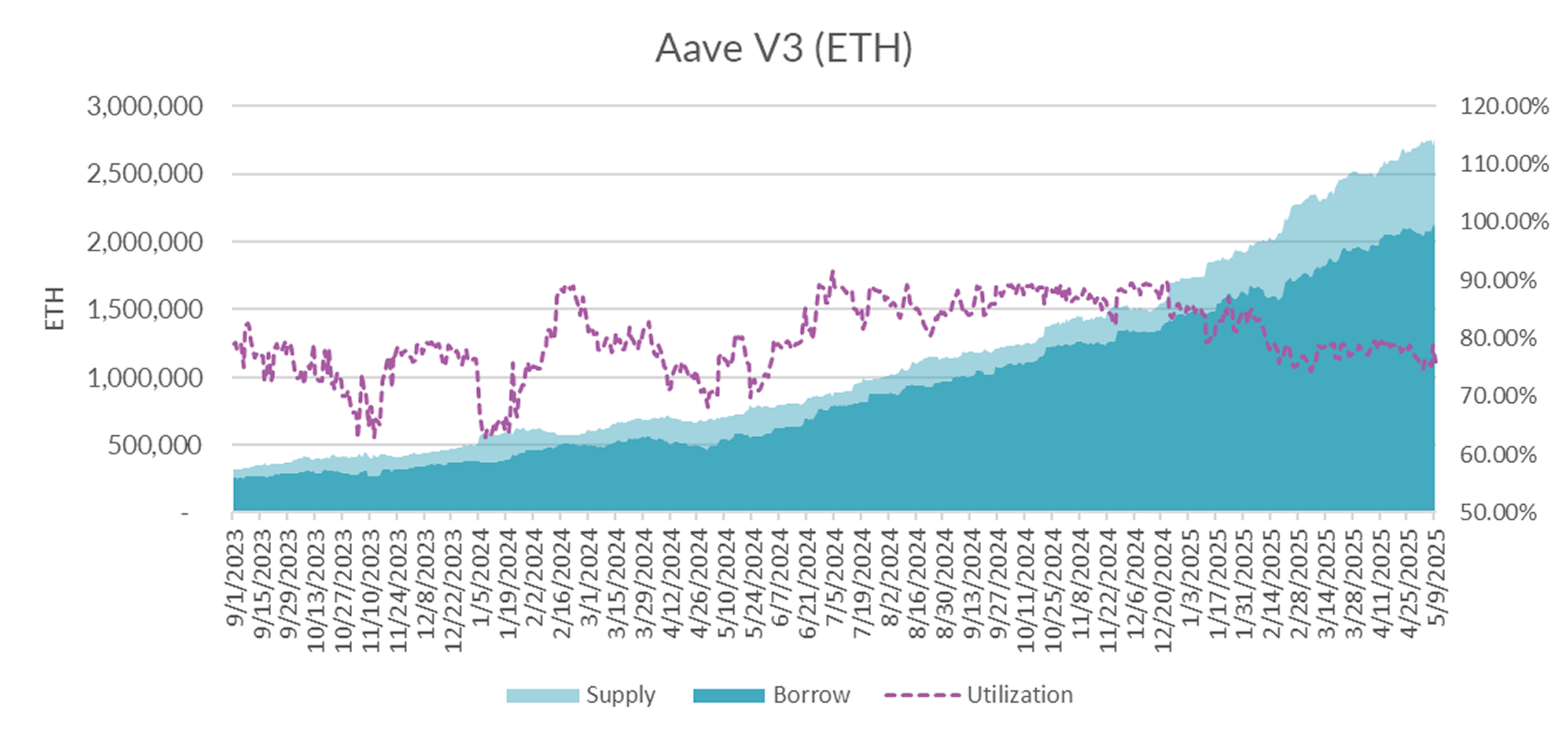

Market internals show that new demand (+49k ETH) slightly outstripped supply (+31k ETH) week on week, but over market dynamics appear balanced.

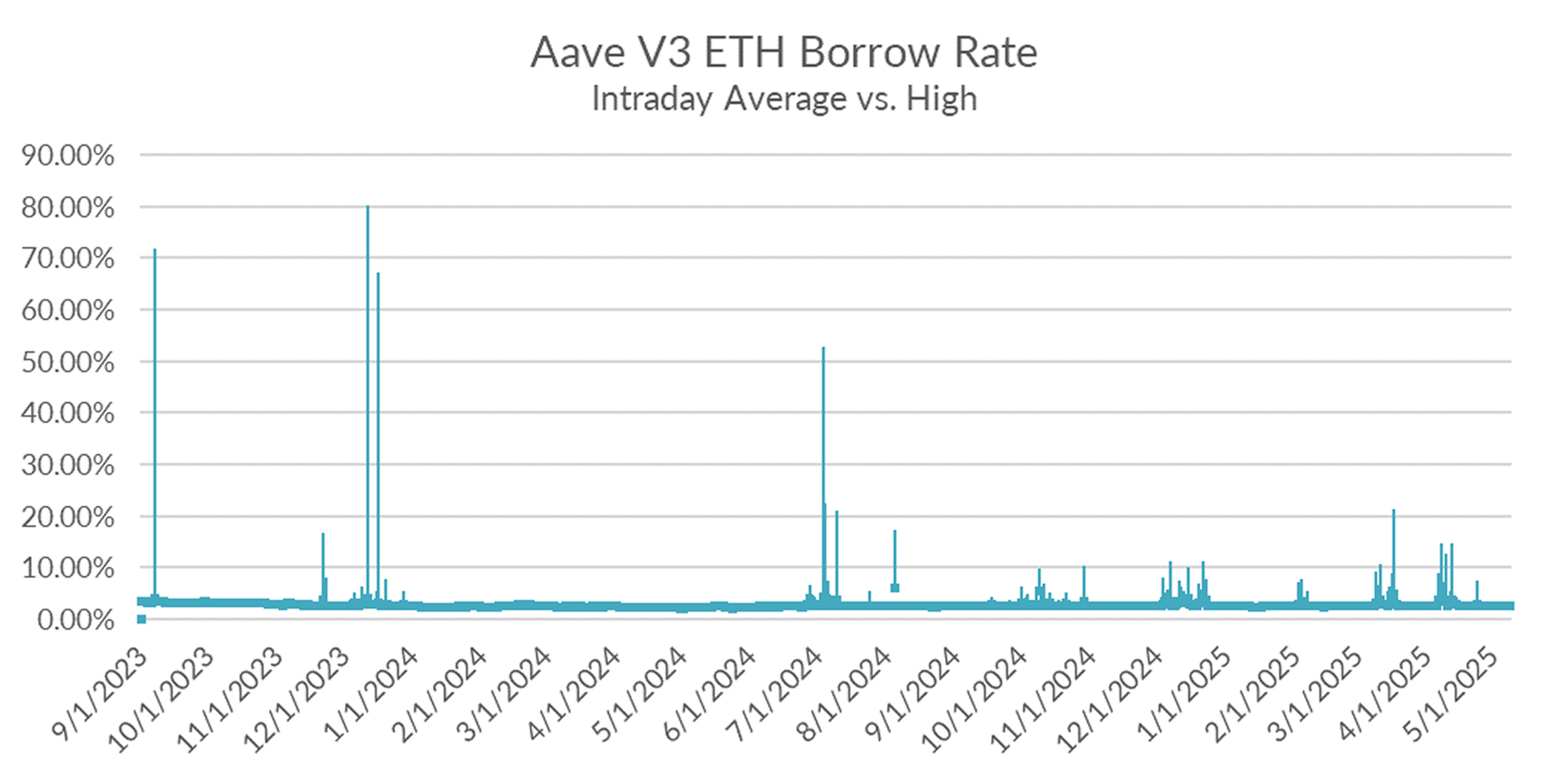

And intraday and intraweek volatility remained low with no kink driven spikes throughout the past seven days.

Overall, ETH rates remain relatively rangebound with the drop in the 30-day trailing average due primarily to that fact that stress levels from April are beginning to move out of the rolling window. Expect rates to remain steady on ETH in the near term.

After weeks of posturing, the U.S. and China have finally set on a date to begin trade talks. This development coupled with de-escalation of the trade war has brought relief to all markets, but particularly so with BTC. With BTC zooming back towards all-time-highs and leverage demand on the rise, expect DeFi rates to follow suit in the medium term.