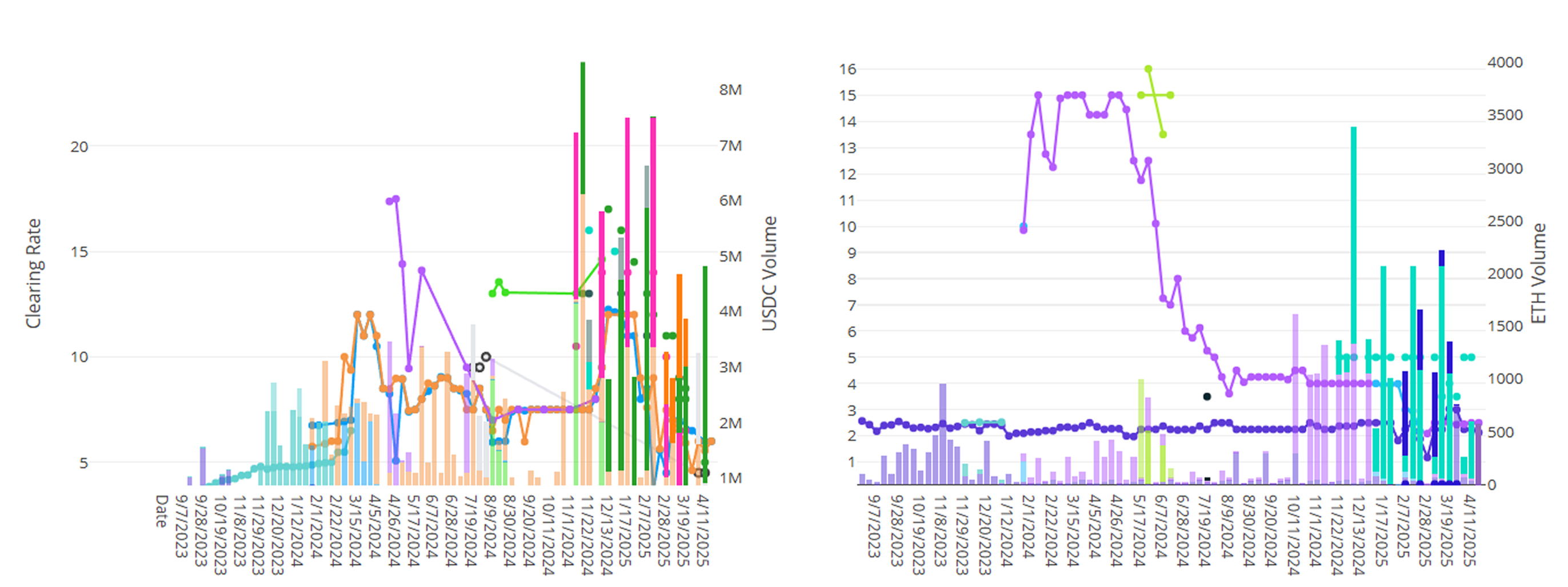

Rates were steady on Term this week. USDC volumes against the majors were light but the Protocol saw demand for and onboarded SuperETH as collateral against wETH supply.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

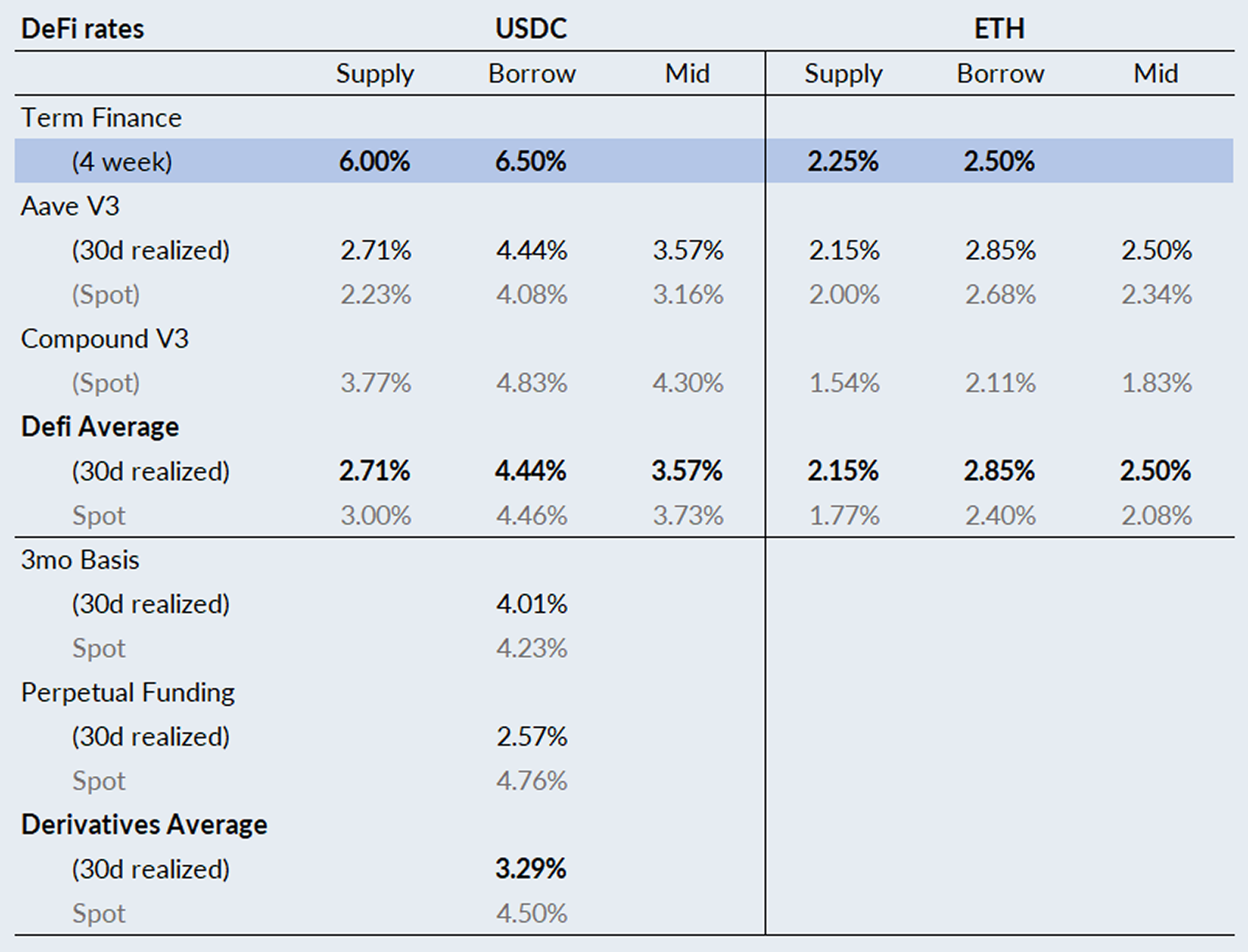

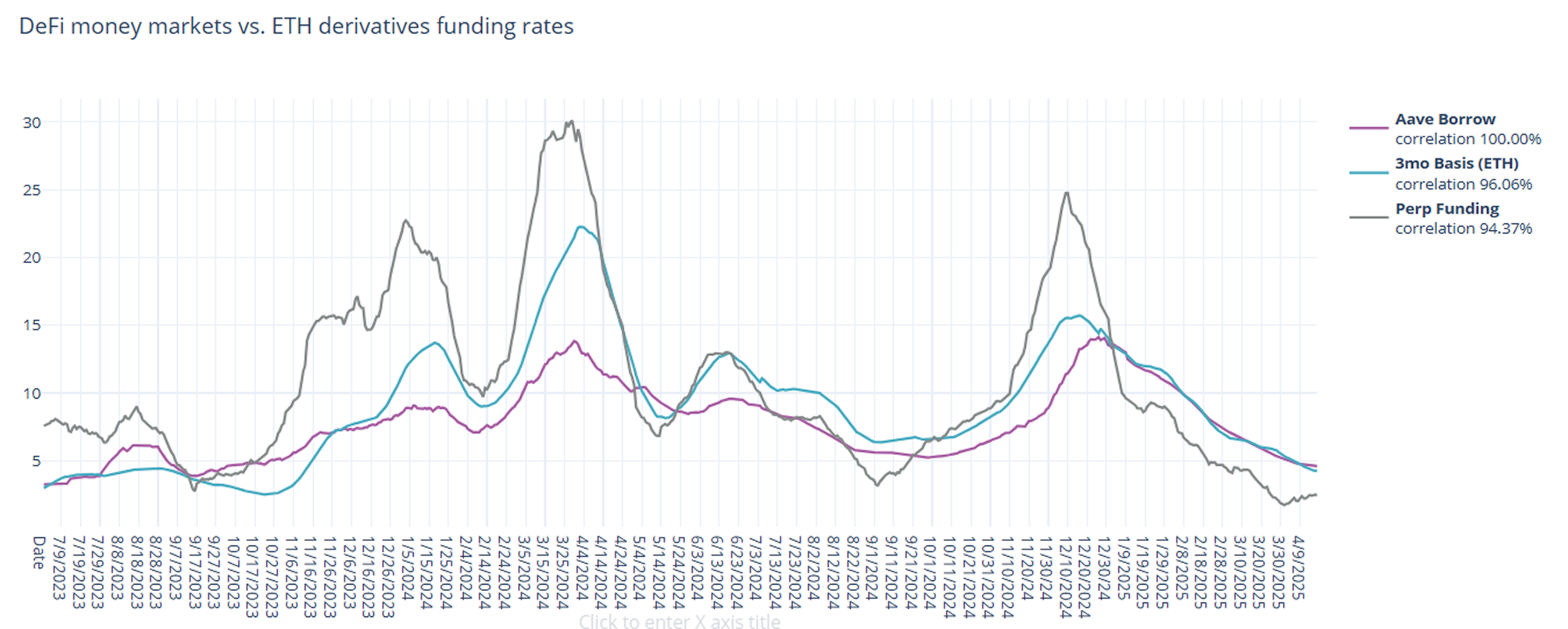

In derivatives markets, funding rates were mixed again, with 3-month basis falling by -22bps to 4.01% and perpetual funding rates rising, for the third week in a row, to 2.57% on a 30-day trailing basis.

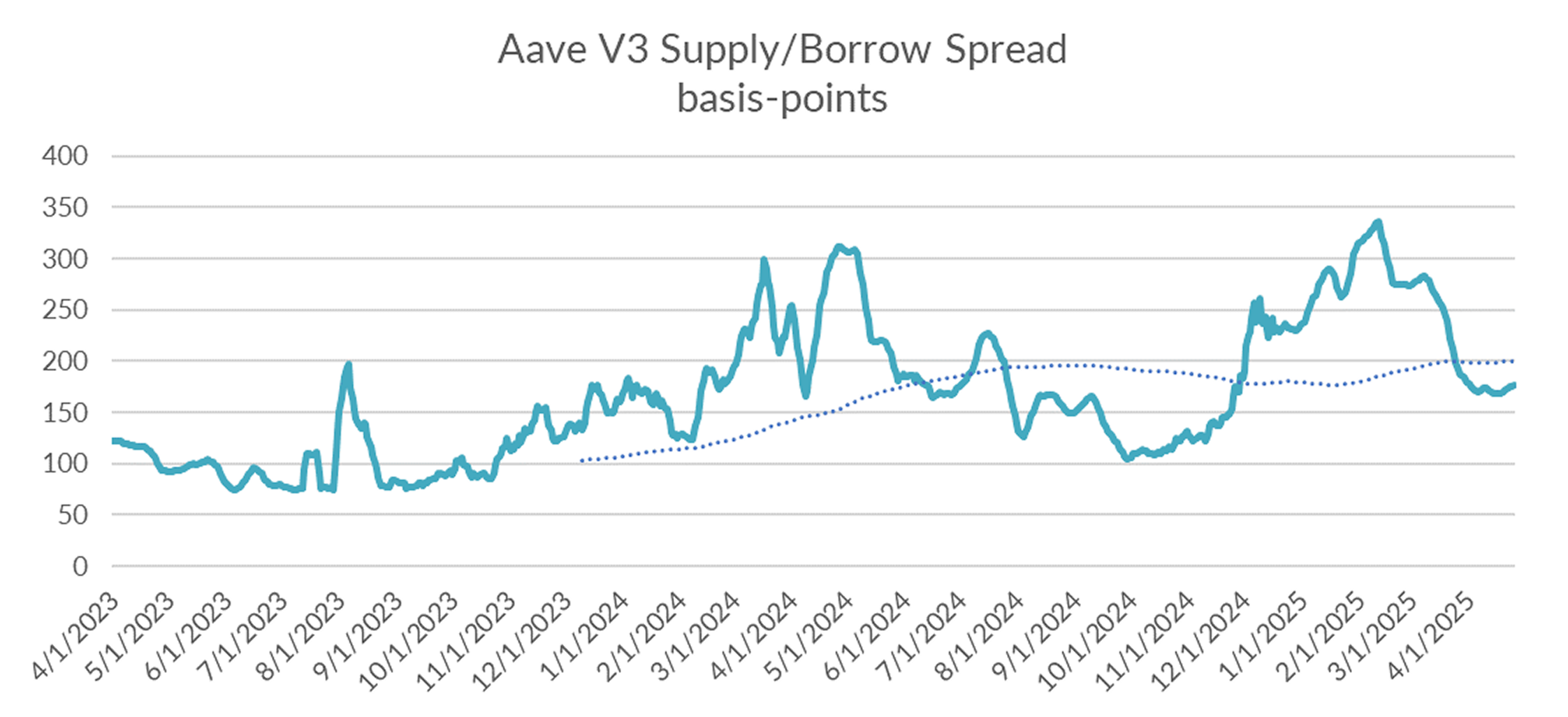

DeFi rates declined slightly on the week, narrowing the spread between DeFi and derivatives rates by roughly -37bps.

Despite this compression, spreads remain well above prior highs and is still quite a ways from inverting back to historical norms where derivatives rates tend to yield higher than its DeFi counterparts. On the other hand, with perpetual swap funding rates rising for a third week in a row and BTC back above 90k, animal spirits are showing early signs of reawakening.

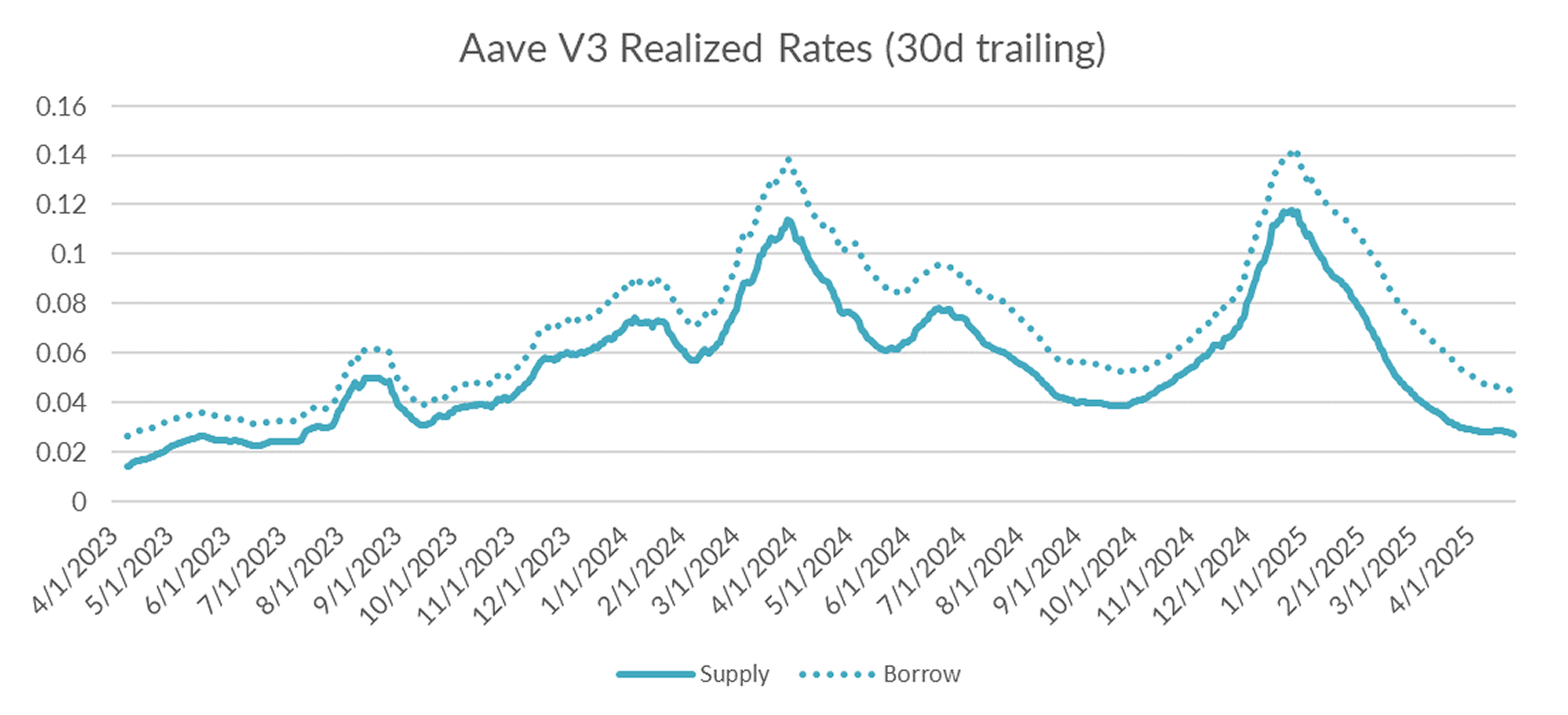

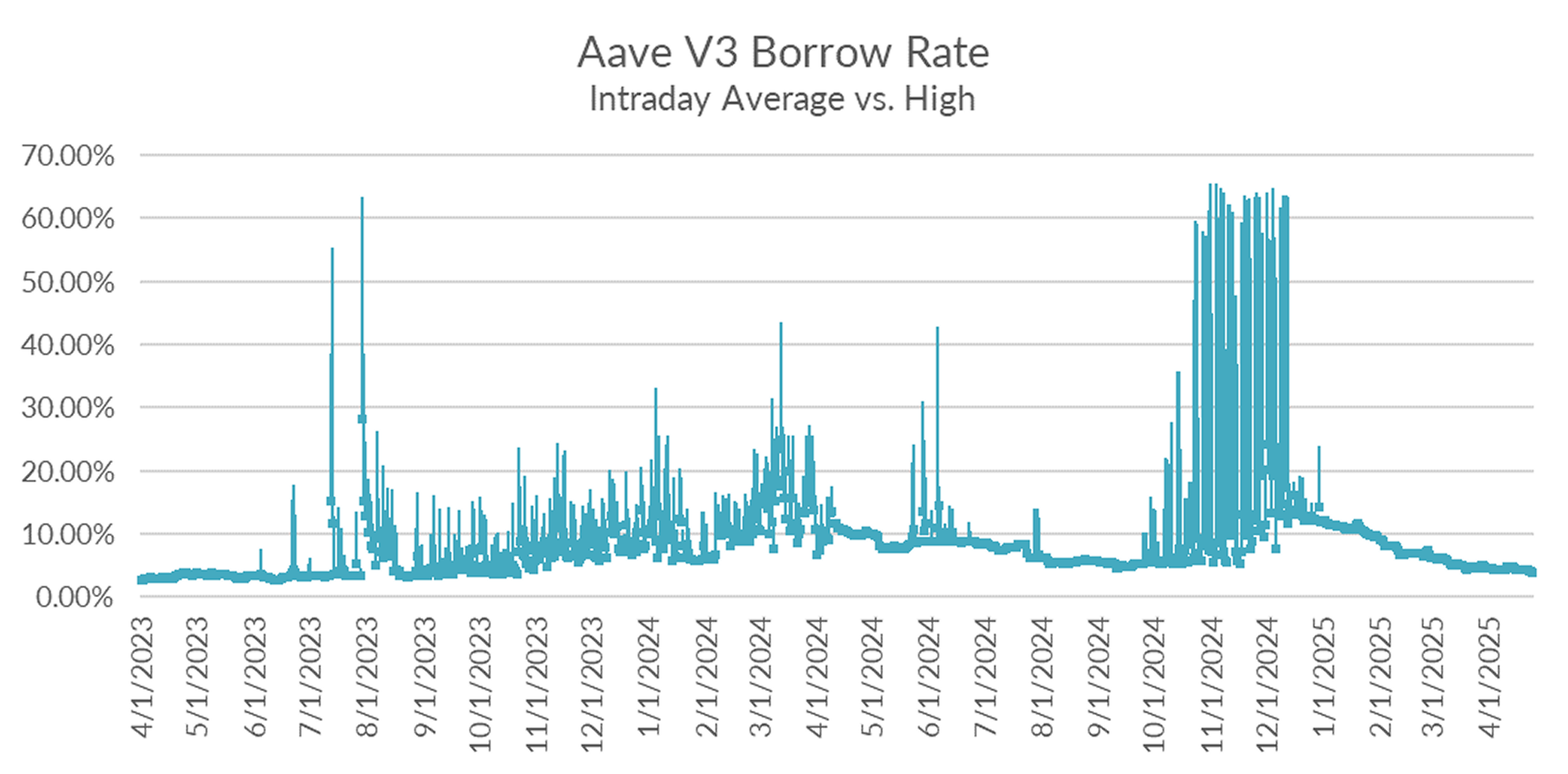

Turning to DeFi variable rate markets, the 30-day trailing average declined -9bps on the week to 4.44. Over a shorter lookback period (just seven days), Aave borrow rates averaged 4.16% on the week, suggesting further declines ahead.

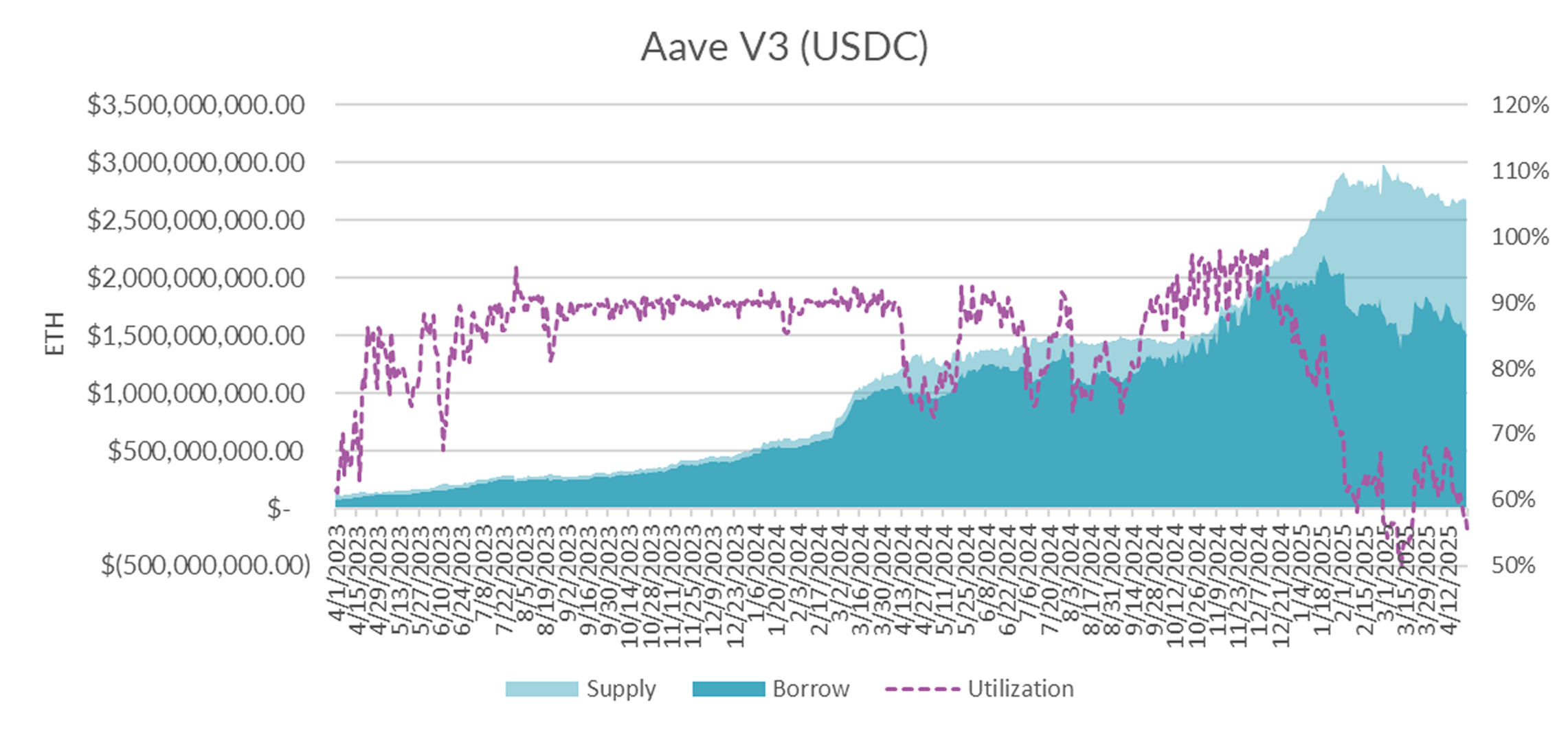

Diving into the microstructure of Aave USDC markets, utilization dipped into the 50s, closing the week at 56%, down from 67% the week prior, primarily due to a sharp decline in borrow demand (-$128M).

Despite the fact that DeFi borrowers can borrow overnight below the risk-free interest rate, overall appetite remains weak.

And with DeFi borrow demand on the decline, supply rates continue to suffer from extreme dilution.

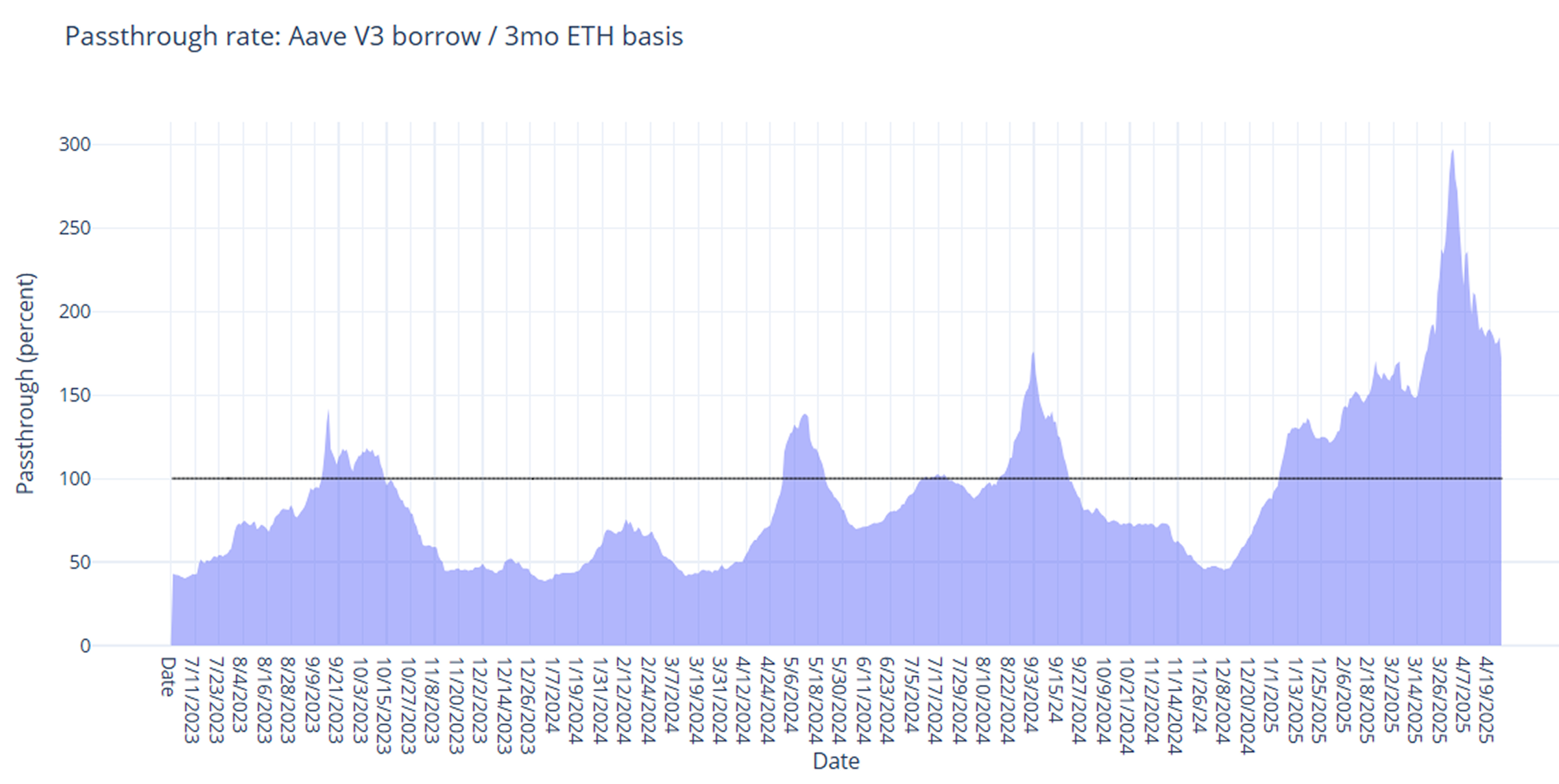

Looking forward, expect DeFi rates to continue to remain weak until we see a more notable uptick in leverage demand in futures and perps markets.

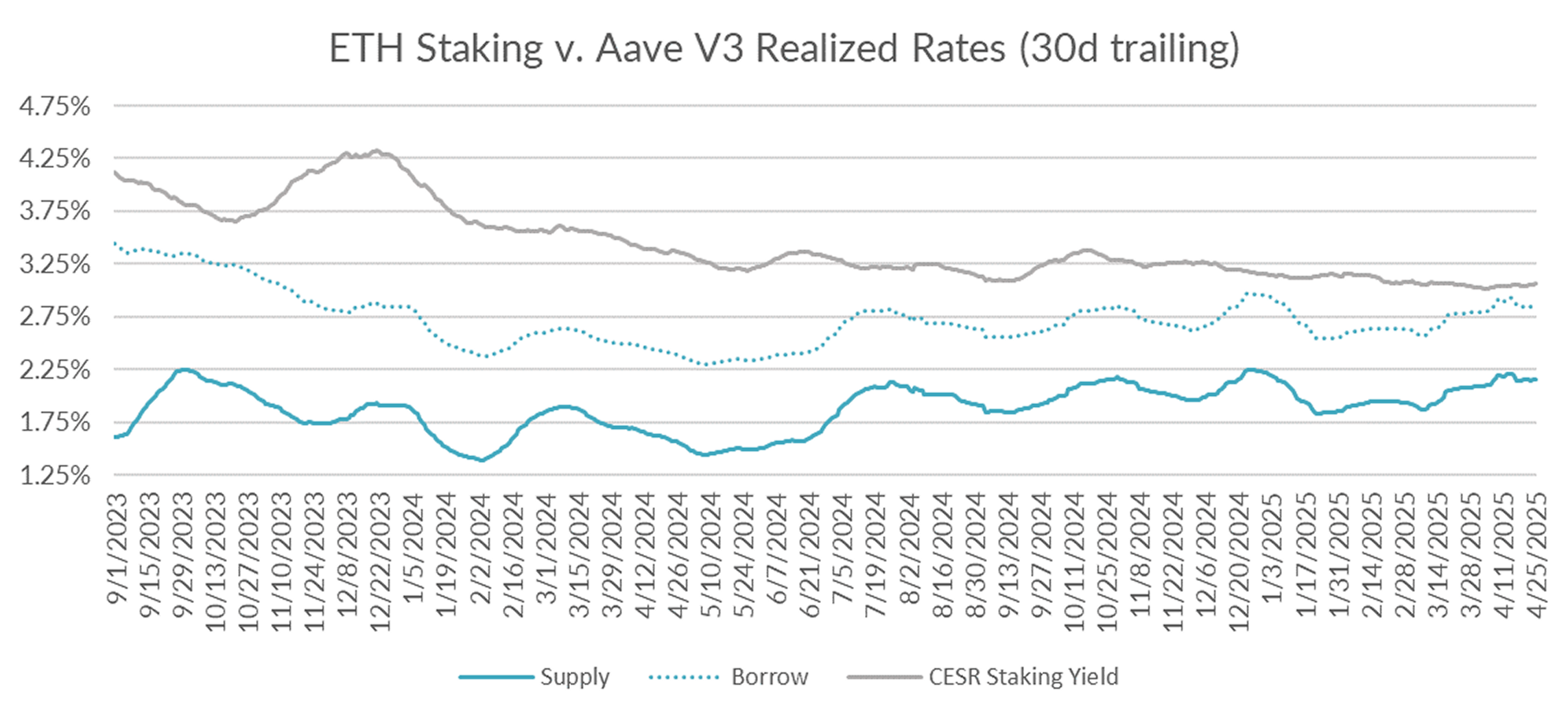

Turning now to ETH markets, ETH rates close the week unchanged, rising by just +1bp on the week to 2.85% on a 30-day trailing basis. The CESR staking index, similarly held steady rising by just +2bp to 3.06%, keeping the spread relatively flat on a 30-day trailing basis.

Market internals show that new supply (+74k ETH) slightly outstripped demand (+38k ETH) week on week.

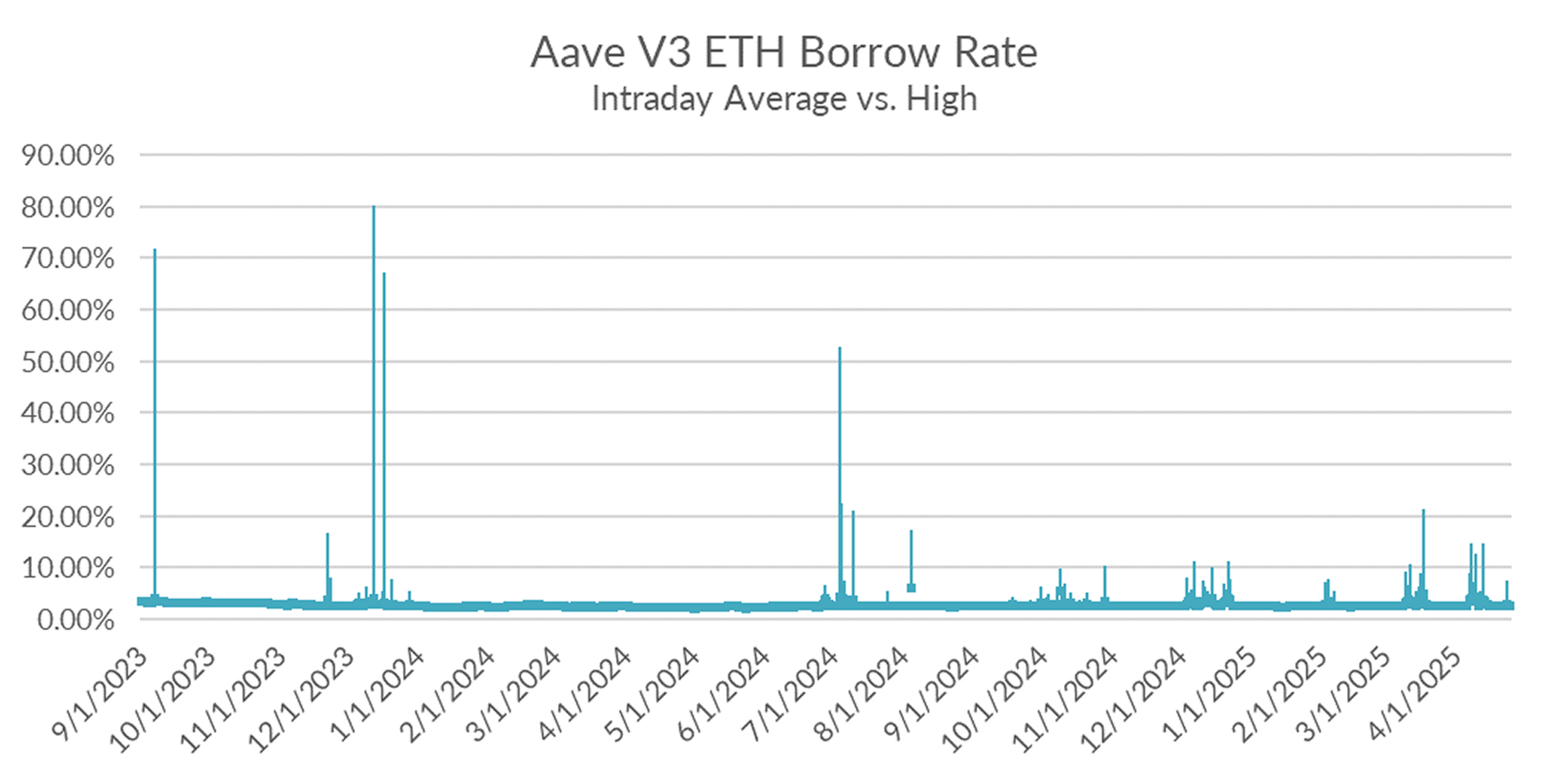

And intraday and intraweek volatility remained low with no kink driven spikes throughout the past seven days.

With ETH borrow costs pushing up against the ETH staking yield and the spread compressing to just 20bps on a 30-day trailing basis, it appears the further upside will be capped. In the near term expect rates to remain rangebound but elevated on ETH.

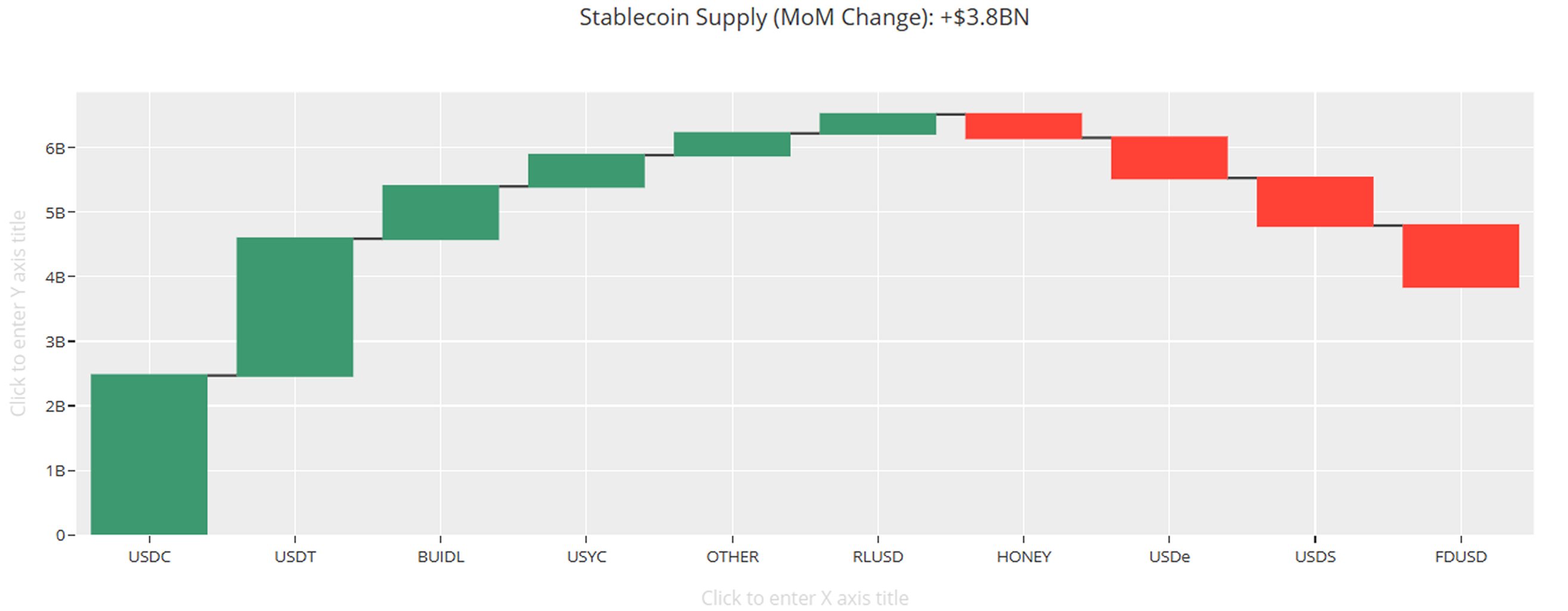

Turning to the flow of funds, stablecoin supply increased by 3.8BN on the month, with USDC leading again for the second month in a row. USDC supply increased by close to +2.5BN, followed closely by USDT at a gain of +2BN. FDUSD, USDe and USDS gave up the most ground at -900M, -700M and -600M, respectively.

Rhetoric around the ongoing trade war cooled, with the Trump administration suggesting the potential for lower tariffs against China and reassuring markets that it would not seek to replace Fed Chair Powell. This de-escalation helped drive a +12–13% gain on the week for both BTC and ETH. With BTC closing the week just under ~95K, interest in leveraged trading is picking up once more. Keep an eye on the markets — if BTC is able to hold this range and break to new highs, it could mark a key turning point for DeFi lending markets.