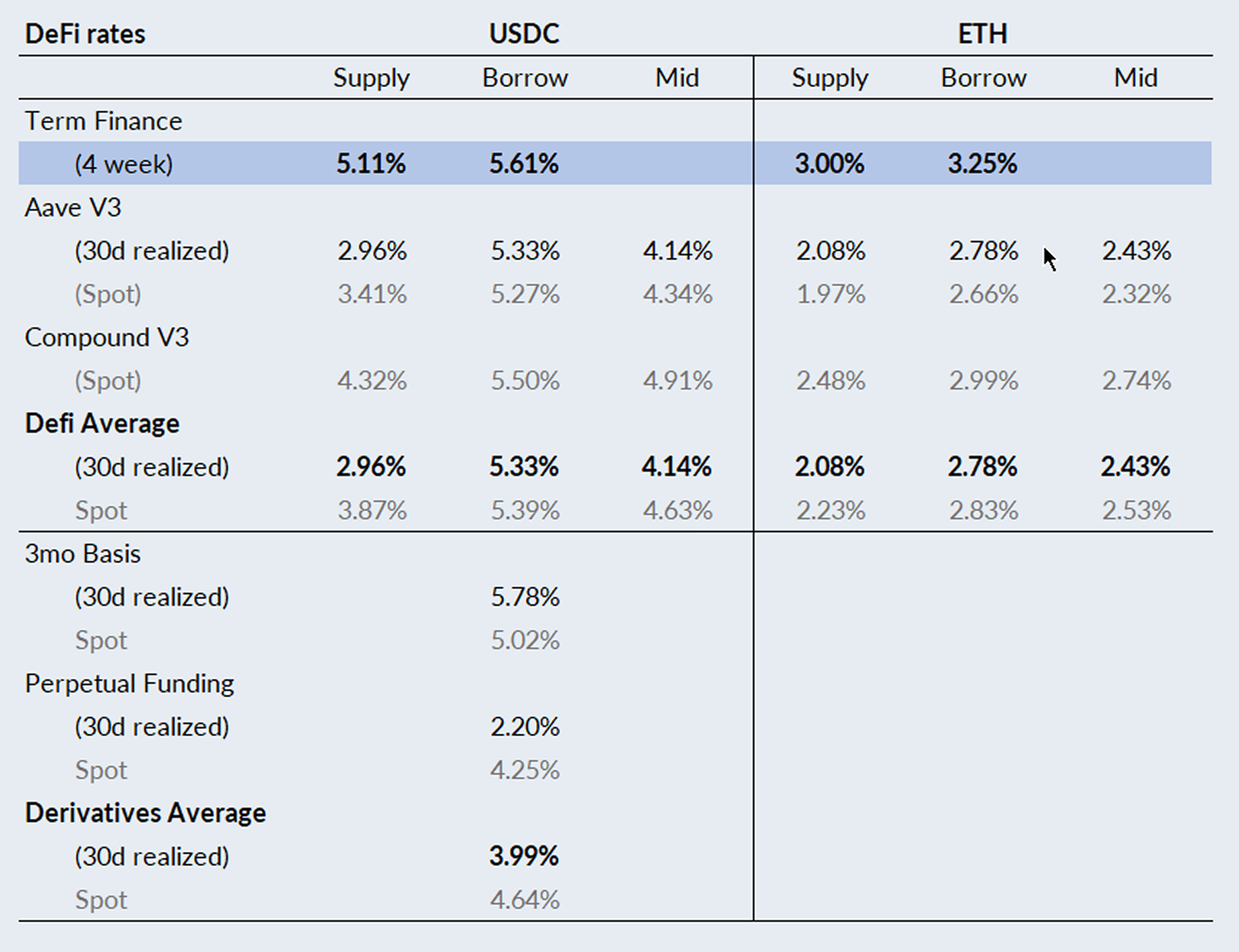

USDC rates continued to drop this week, falling by another -90bps on low volume to clear around 5.11% , on average against the majors. ETH rates bumped up slightly, clearing at 3.0% against wstETH and 3.5-4% against exotics.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

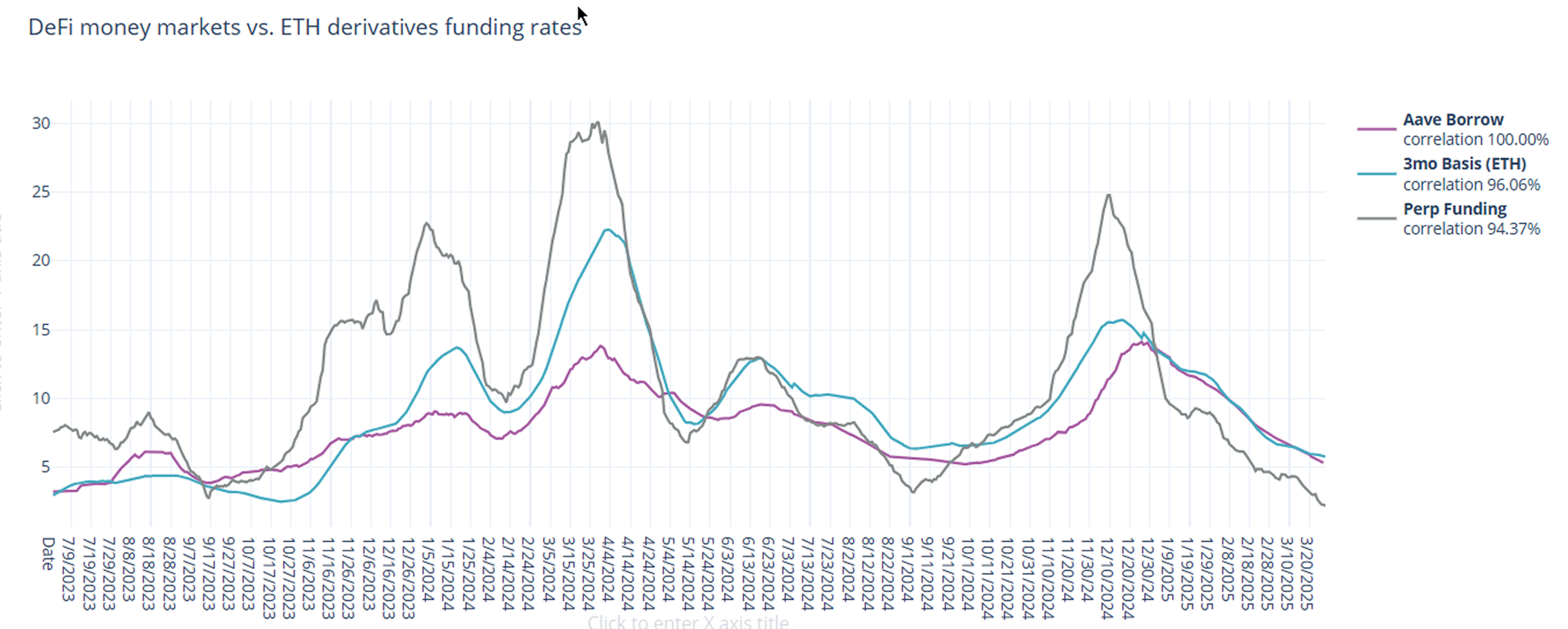

In derivatives markets, funding rates continue to decline, with 3-month basis falling by -20bps to 5.96% and perpetual funding rates falling by -85bps to 2.20% on a 30-day trailing basis.

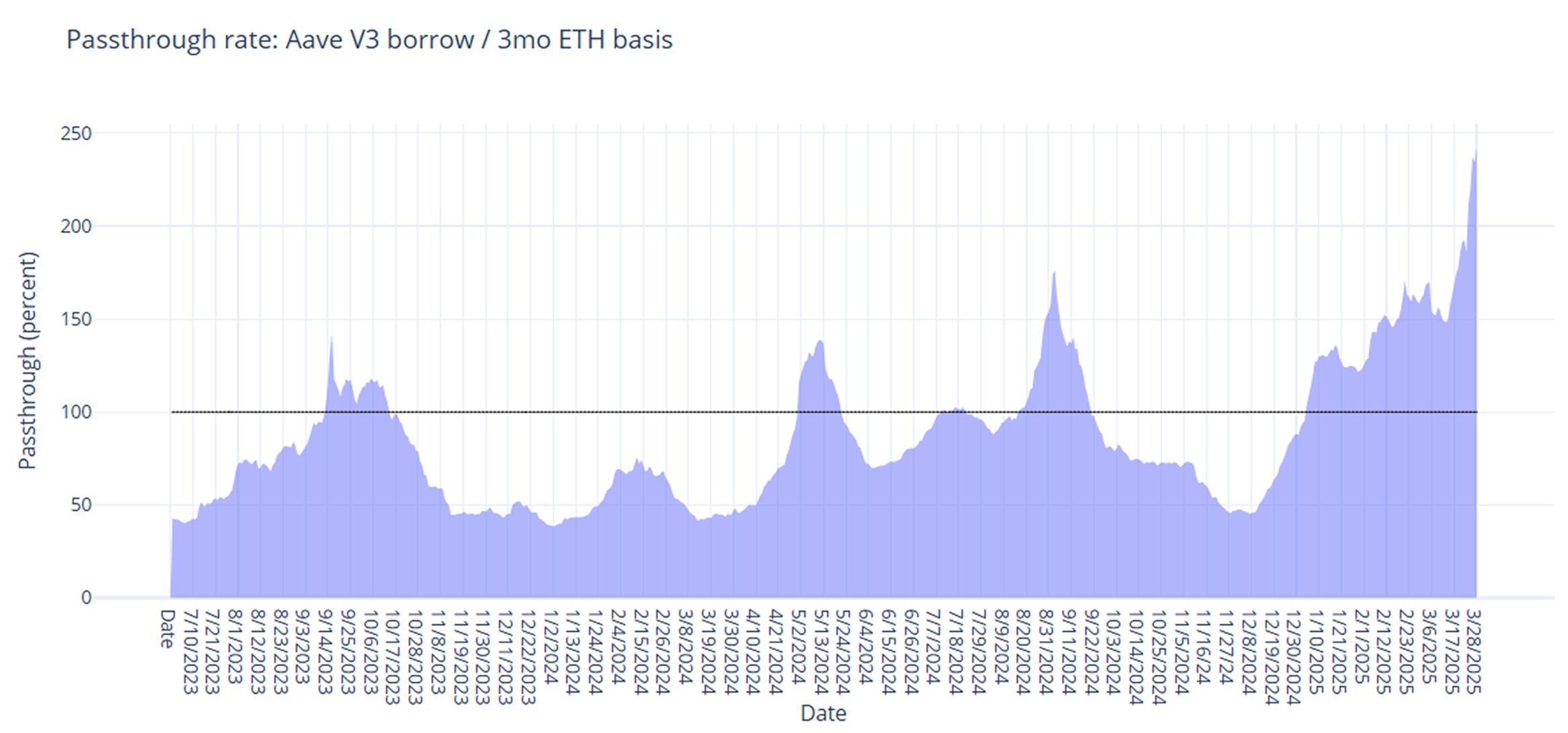

DeFi protocols, on the other hand, remain steady with rates prevailing >240% above perps, which is approaching the lowest levels since we started tracking on this newsletter.

While perps continue to average down over a 30 day lookback period, the silver lining is that this past week was the first week in a month where rates did not dip into negative territory at least once over the past 7 days.

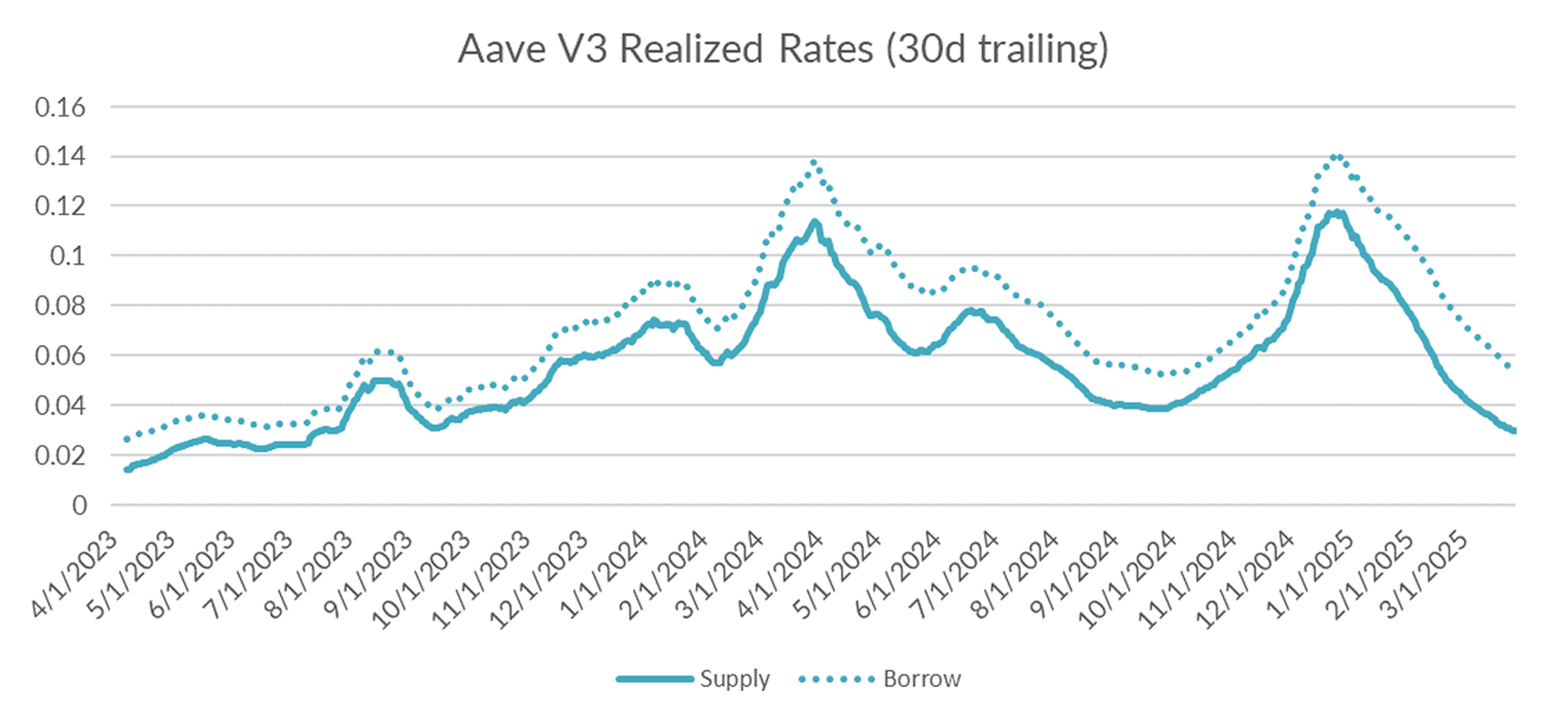

Turning to DeFi variable rate markets, the 30-day trailing average declined -51bps on the week to 5.33%. Over a shorter lookback period (just seven days), Aave borrow rates averaged 4.83% on the week, consistent with 3-mo basis and close to the Fed Funds target rate.

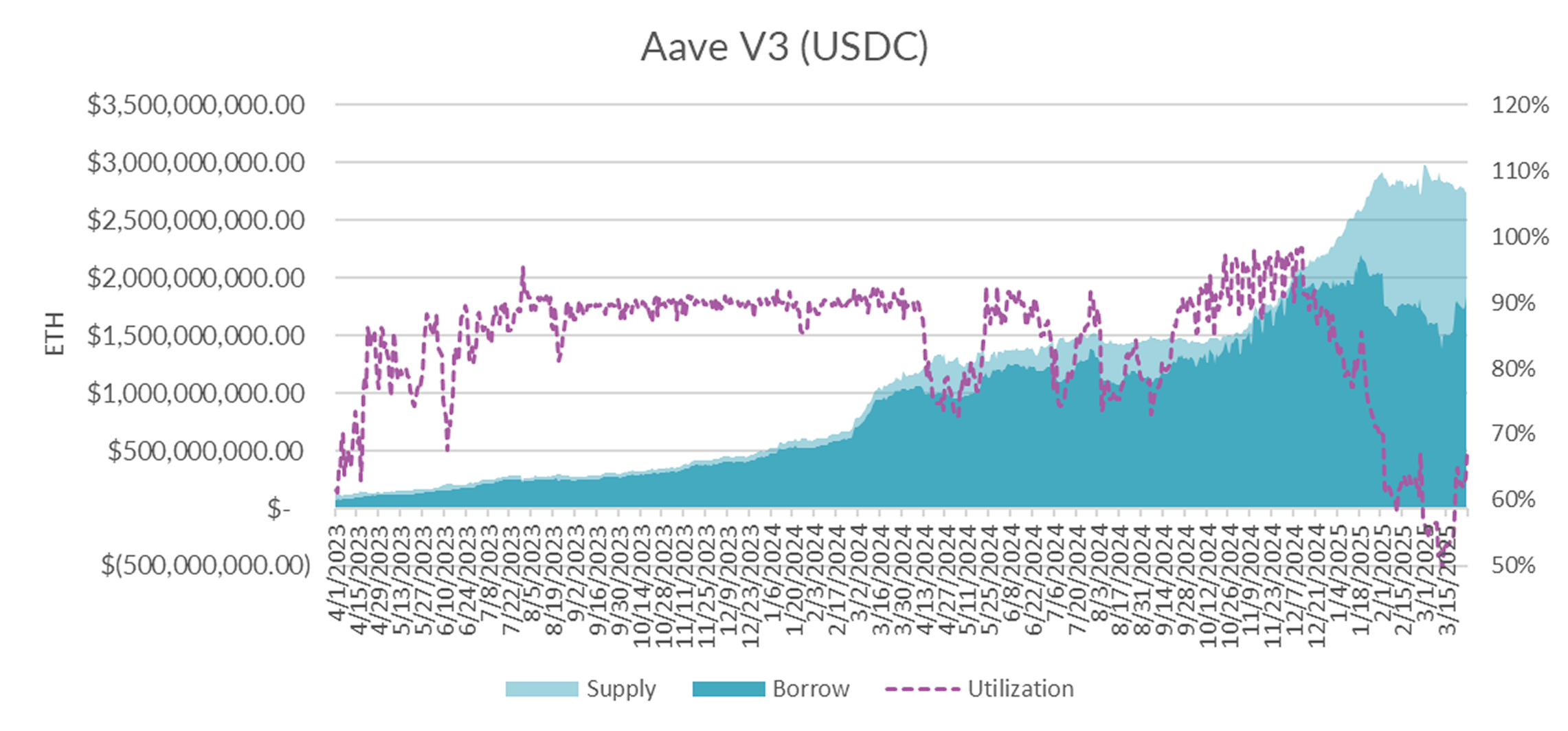

Diving in the microstructure of Aave USDC markets, utilization held steady in the mid 60s% range — due to a mix of lower supply and increased borrow demand at lower rates.

Since the beginning of the year, Aave markets have been a one way street lower. With the recent increase in utilization the past two weeks, there is hope this may stabilize.

In a win for suppliers on Aave, the recent increase in utilization has brought down the spread between borrow/supply rates mitigating some of the dilutive effects of idle capital on the platform.

Overall, Aave’s USDC market seems closer to finding an equilibrium. With perps solidly below Aave borrow rates, we’re starting to feel out a bottom to see what DeFi money markets settle in the absence of basis arbitrage.

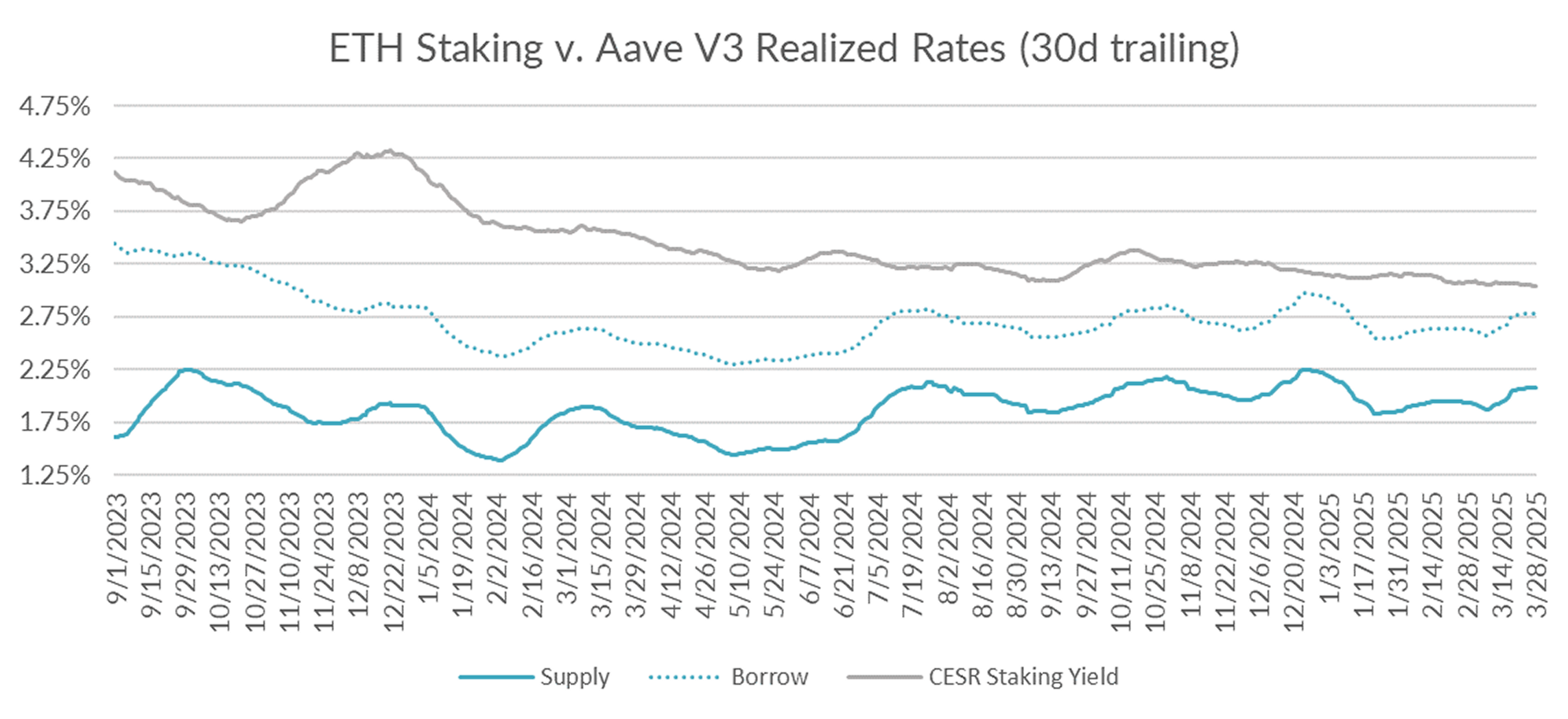

Turning now to ETH markets, ETH rates rise slightly by +1bp on the week to 2.78% on a 30-day trailing basis. The CESR index held steady, closing unchanged on the week, keeping the spread between staking and borrowing to just 29bps on a 30-day trailing basis.

Market internals show that overall supply and demand picture remains robust on Aave. Increased borrow demand was matched by an increase in available supply over the course of the week of a similar amount.

Signs of short term stress due to sudden spikes in ETH borrowing also dissipated, consistent with the lack of negative perp rates seen over the past week.

Overall, ETH rates appear to levelling out with a steady growth in TVL as alternative ETH yield opportunities decline.

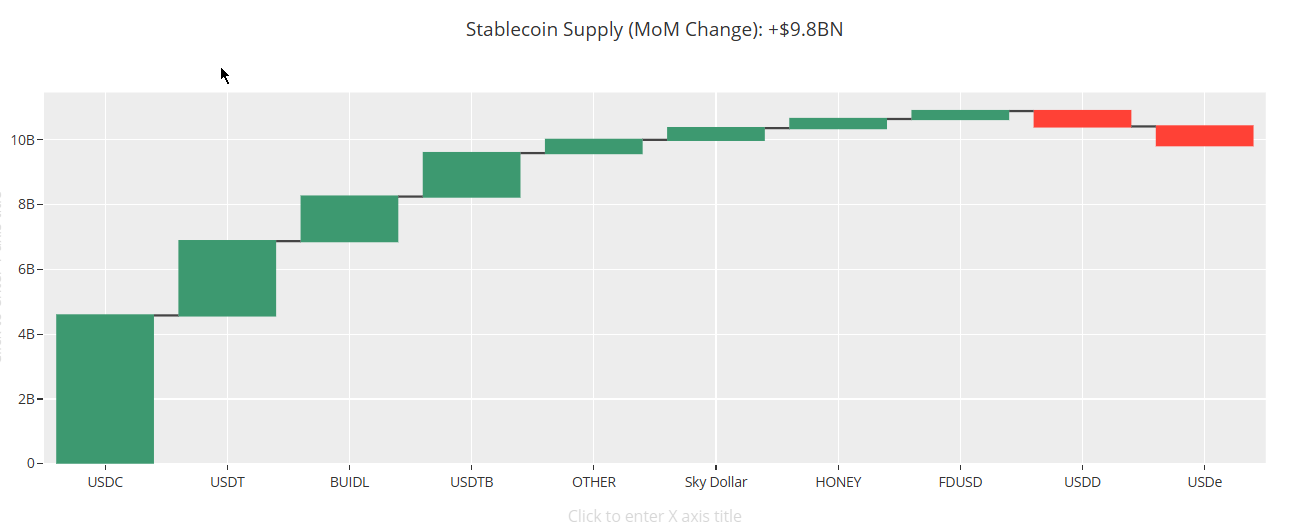

In flow of funds, stablecoins saw another +9.6BN in inflows this past month, matching the ~10BN in inflows the month prior. Despite all the bearish sentiment around crypto assets, stablecoin flows suggest that DeFi and blockchain adoption continues to grow.

Over the month, USDC was the largest gainer with USDT taking an unusual second place. Other notable gainers were Blackrocks BUIDL (+1.375BN),

Ethena’s USDTB ( +1.3BN, backed by BUIDL), and Sky’s USDS (+362M).

On a macro level, crypto markets close the week flat to slightly down while BTC held steady around ~85k. The decline in perp rates and 3mo basis rates suggest a lack of near-term optimism and DeFi rates will likely be subdued in the near future.