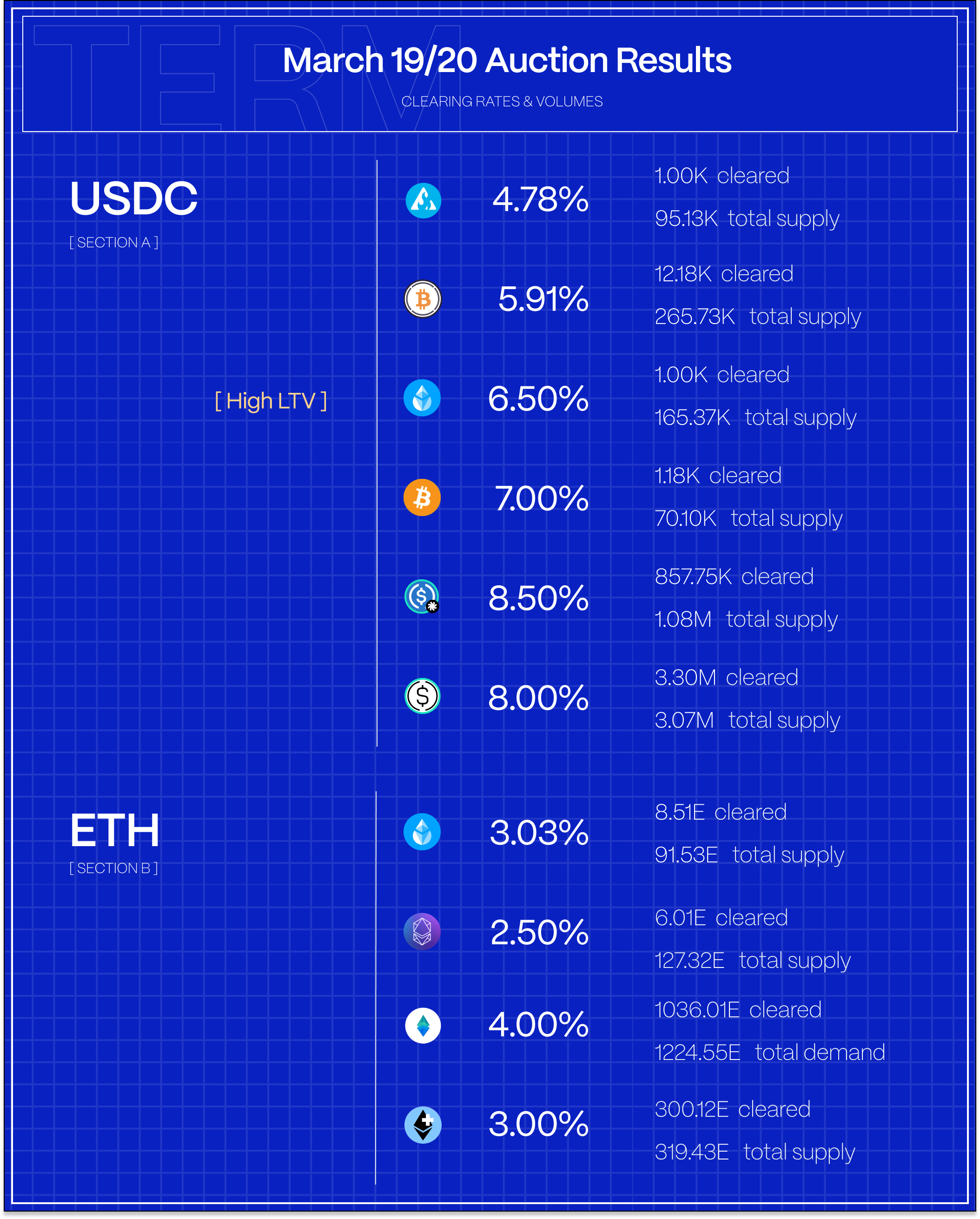

USDC rates continued to drop this week, falling by another -50bps to clear around 6% , on average, against the majors, while rates against exotics held steady around 8% - 9%. ETH rates were unched, clearing at 2.5% against blue chips and 3-4% against exotics. On the Term Vaults side, deposits increased this week taking total deposited up towards $15M.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

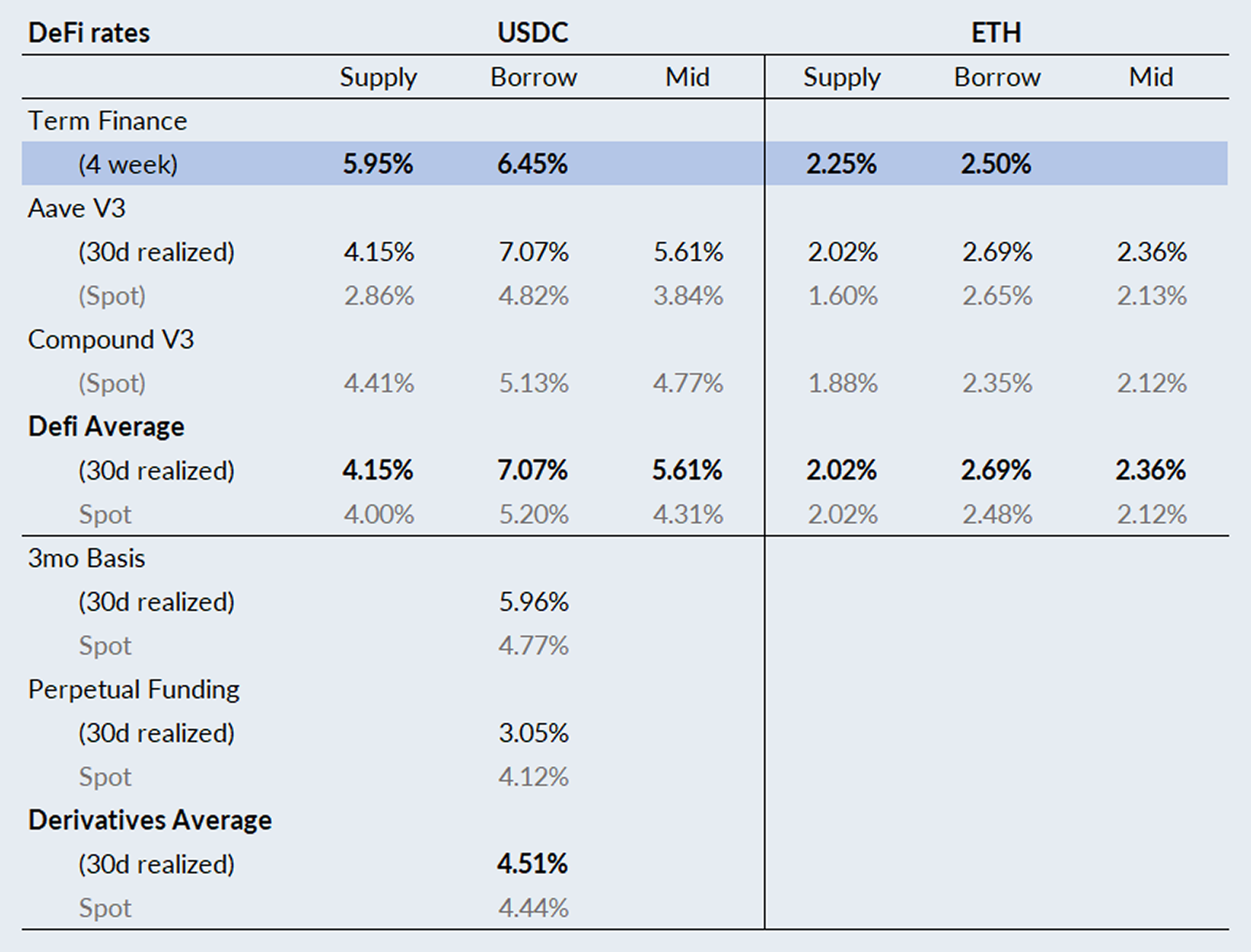

In derivatives markets, funding rates accelerate to the downside, with 3-month basis falling by -42bps to 5.96% and perpetual funding rates falling by -121bps to 3.05% on a 30-day trailing basis.

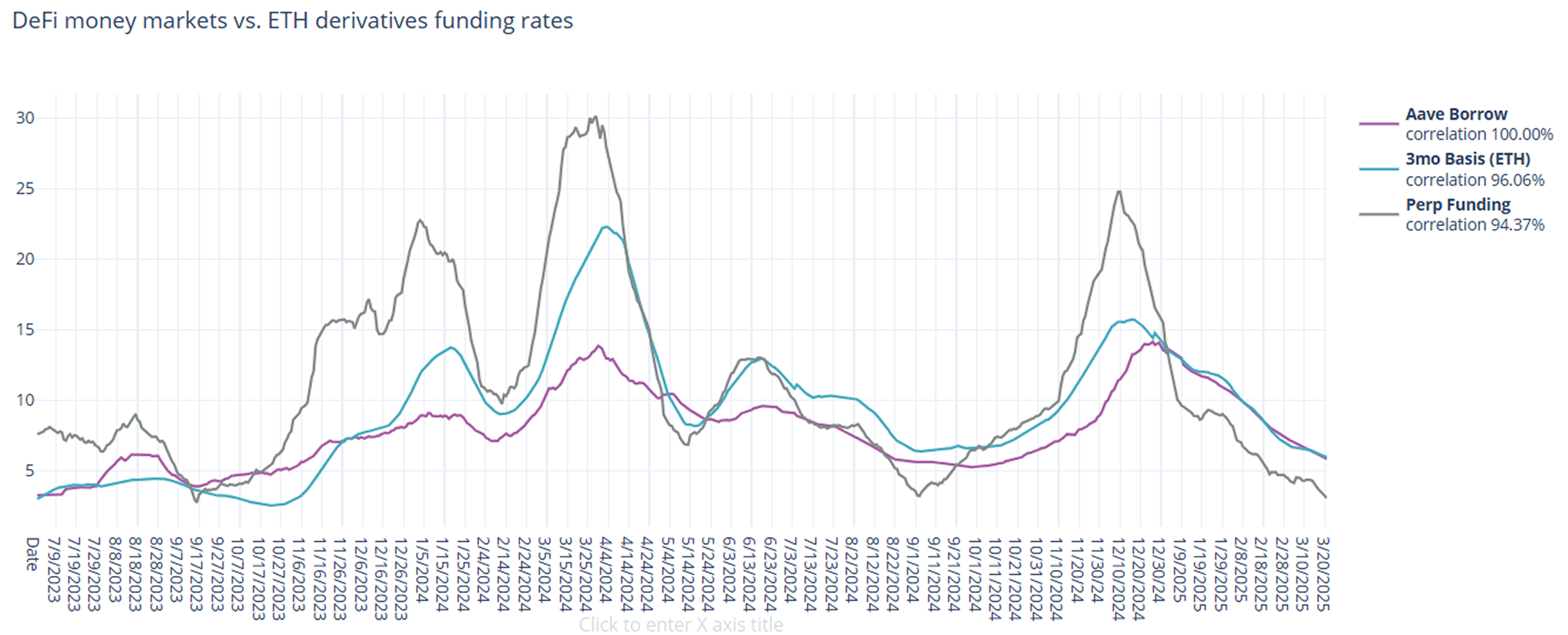

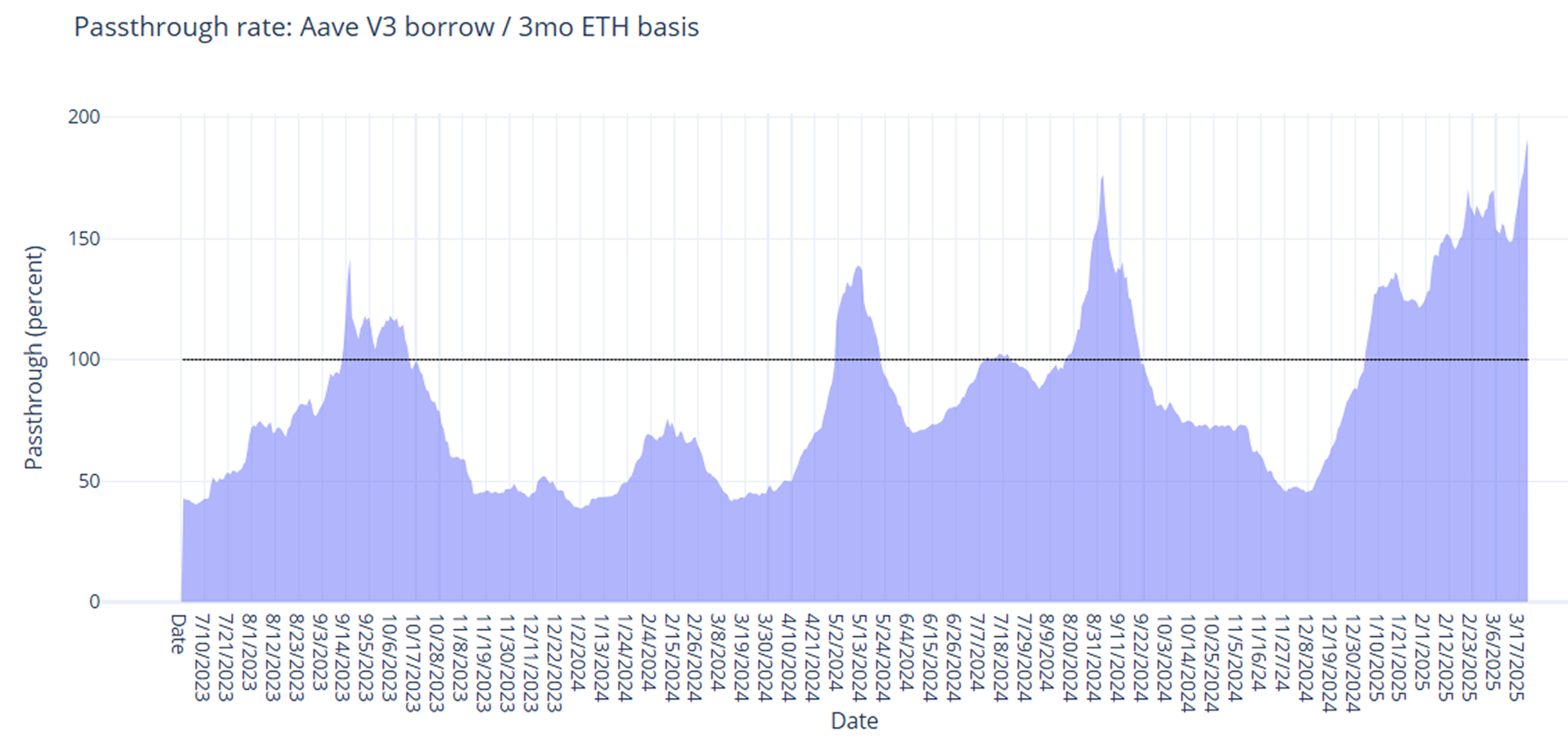

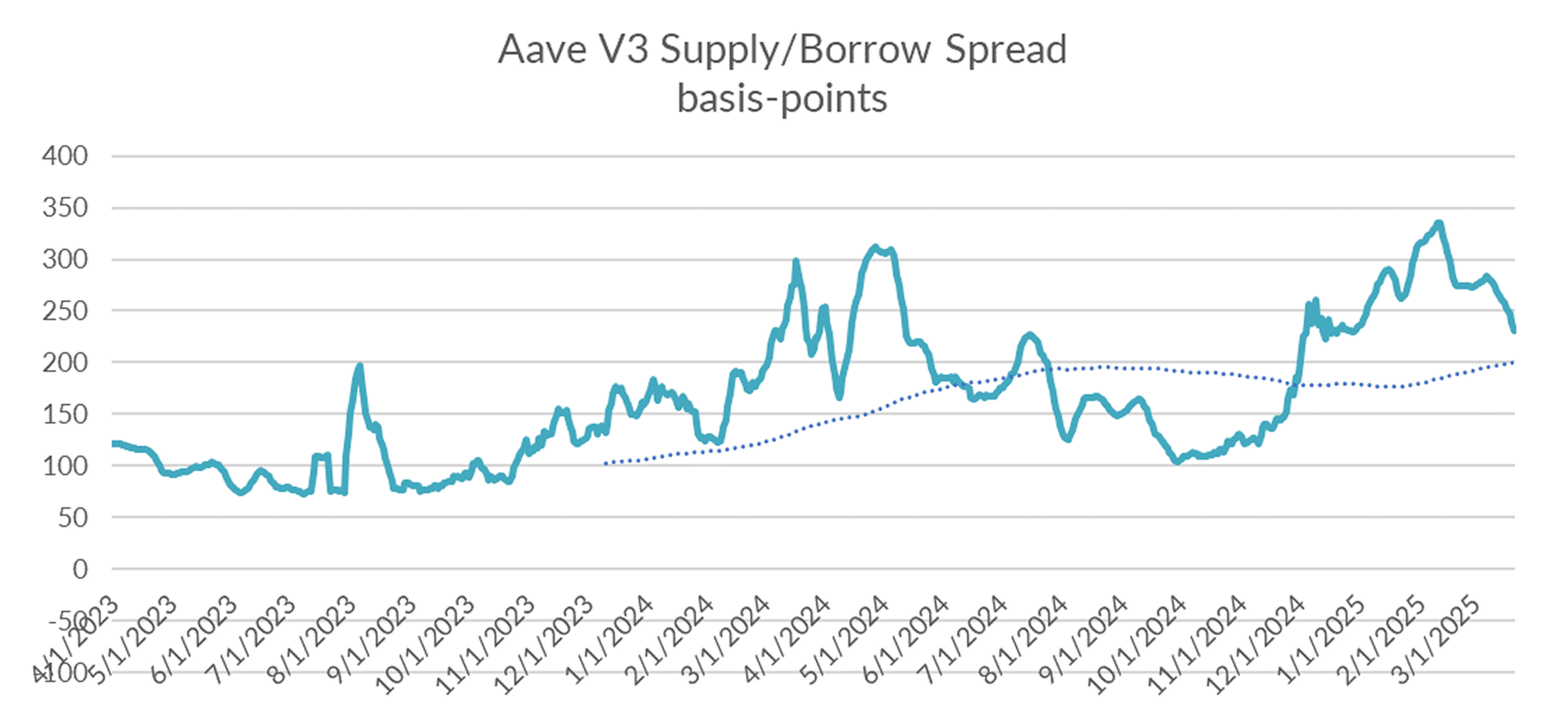

With floating rate protocols behind the curve on adjusting rates, DeFi borrow rates continue to remain elevated as compared to derivatives funding rates, causing the spread to hover at all time highs.

The collapse of 3-mo basis down -82bps week on week, which to this point held steady in the 6-7% range, is concerning. It suggests that institutional players are pricing in lower rates for longer.

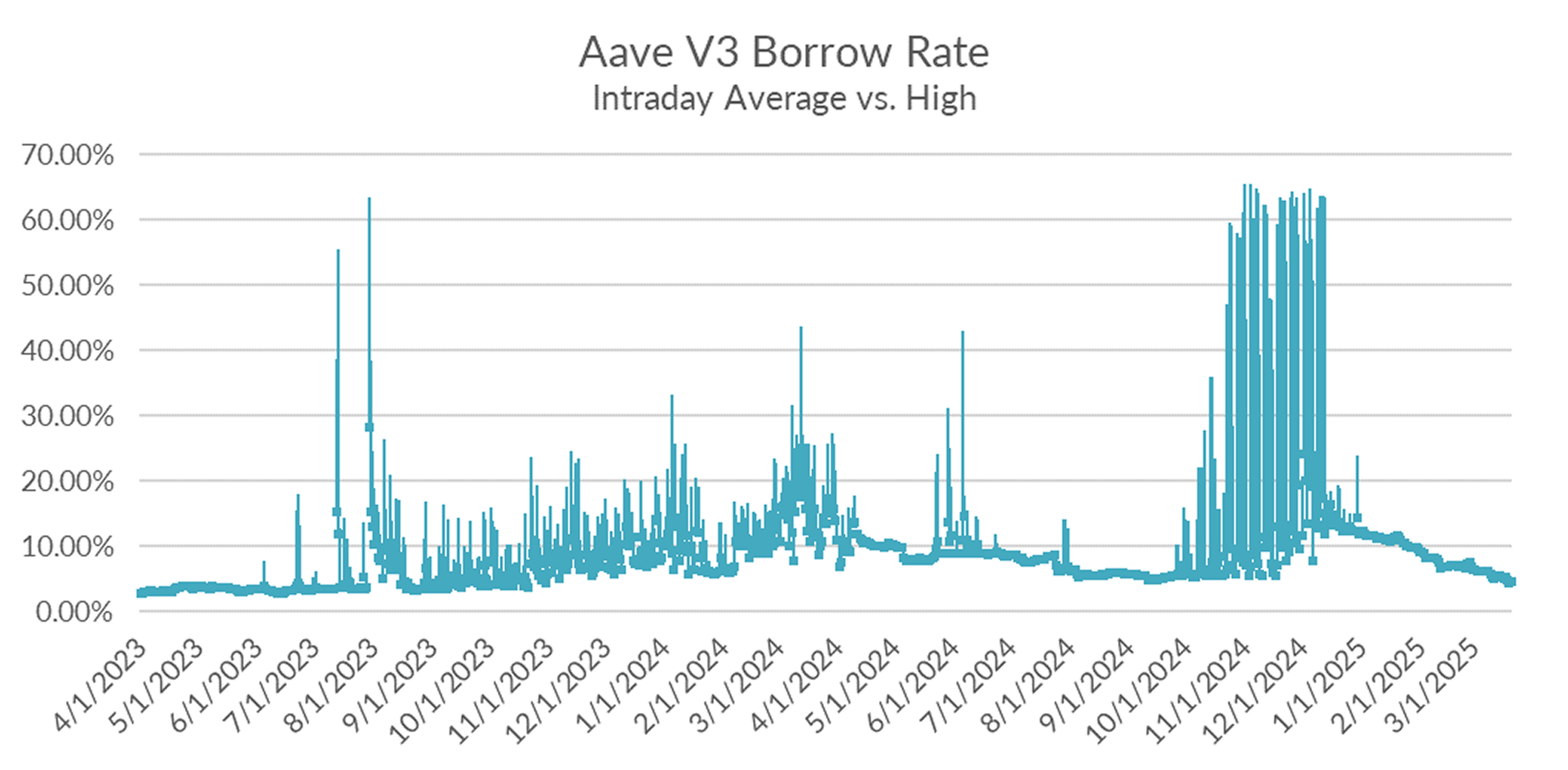

Turning to DeFi variable rate markets, Aave’s base rate adjustment this past week allowed rates to come down, taking the 30-day trailing average down -53bps on the week to 5.83%. Over a shorter lookback period (just seven days), Aave borrow rates averaged 4.75% on the week, consistent with 3-mo basis and close to the Fed Funds target rate.

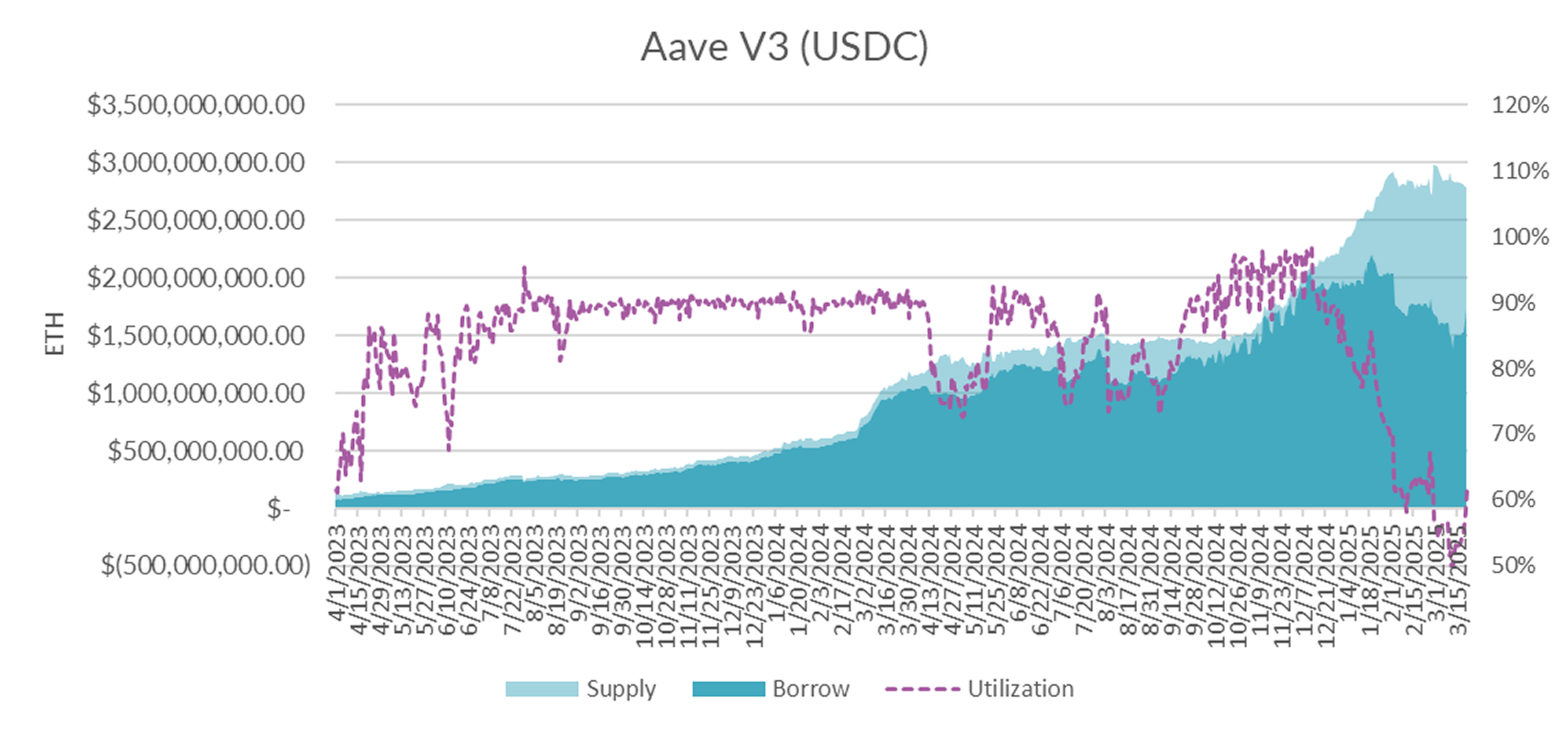

Diving in the microstructure of Aave USDC markets, utilization literally fell “off the charts” but bounced back as the Aave base rate adjustment went into effect to bring Aave borrow rates in line with the market.

Due to quirks of Aave’s interest rate model, this cut in the base rate actually led to HIGHER supply rates for depositors — total supply held steady.

And as a result of increased utilization due to the base rate adjustment, the spread between supply/borrow rates is beginning to normalize.

While the adjustment was welcome in helping to normalize market dynamics, overall utilization hovers around 60%, still far from the optimal utilization rate of 90% and suggests that the base rate has room to decline further. Based on market dynamics in the derivatives market, all signs point to lower rates.

ETH Markets

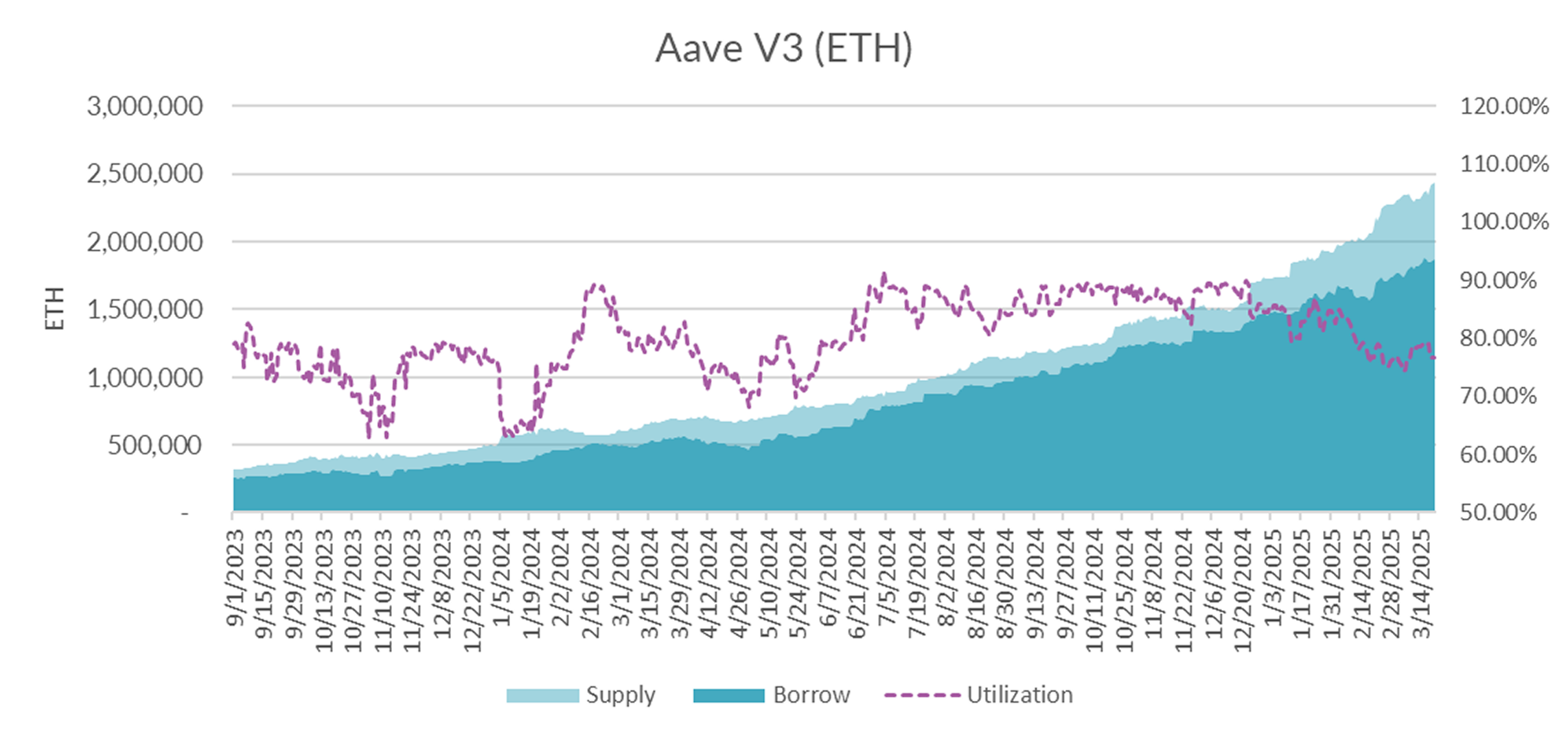

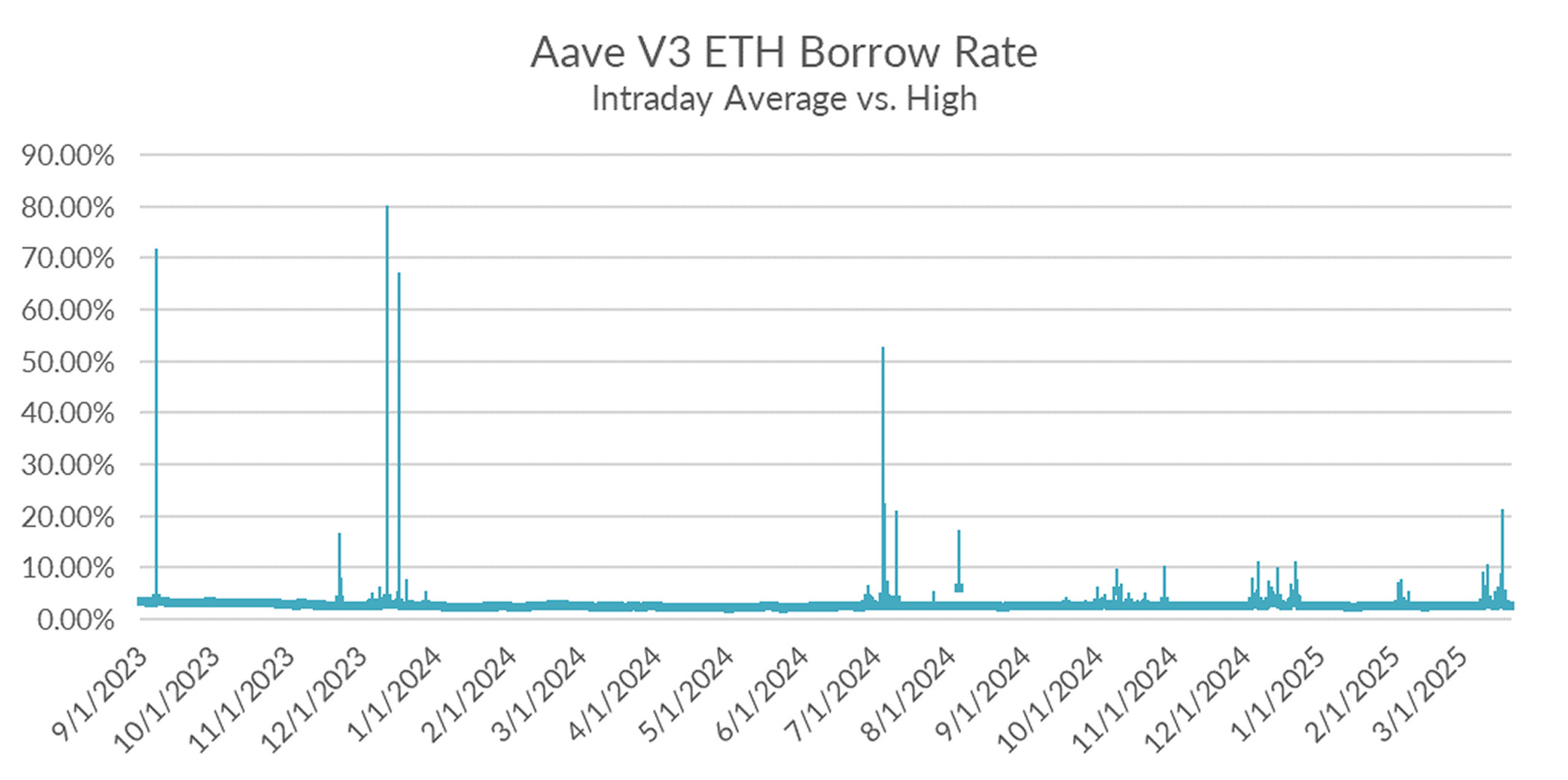

Turning now to ETH markets, ETH rates accelerate to the upside rising by +12bps on the week to 2.77% on a 30-day trailing basis. The CESR index on the other hand held steady, falling by -1bp on the week, narrowing the spread between staking and borrowing to just 29bps on a 30-day trailing basis.

Market internals show that overall supply and demand picture remains healthy on Aave. Increased borrow demand was matched by an increase in available supply over the course of the week,

though intraweek the increase in both total supplied and demanded was anything but coordinated. ETH rates spiked up to 16.84% on Tuesday for a brief period, perhaps driven by short term borrowing as an alternative to selling short on perps when funding rates turn negative.

Overall, ETH rates continue to climb and show more frequent occurrences of short term spikes in intraday borrow rates.

Despite relatively flat crypto asset markets over the past week, DeFi lending markets continue to paint a grim picture. Deleveraging persists in both derivatives and DeFi lending markets, pushing rates lower—an unsurprising development given the lack of clarity around macro policy over the past two months. Indeed, as the Fed reiterated 16 times in its post-statement press conference this week, markets remain highly “uncertain.”