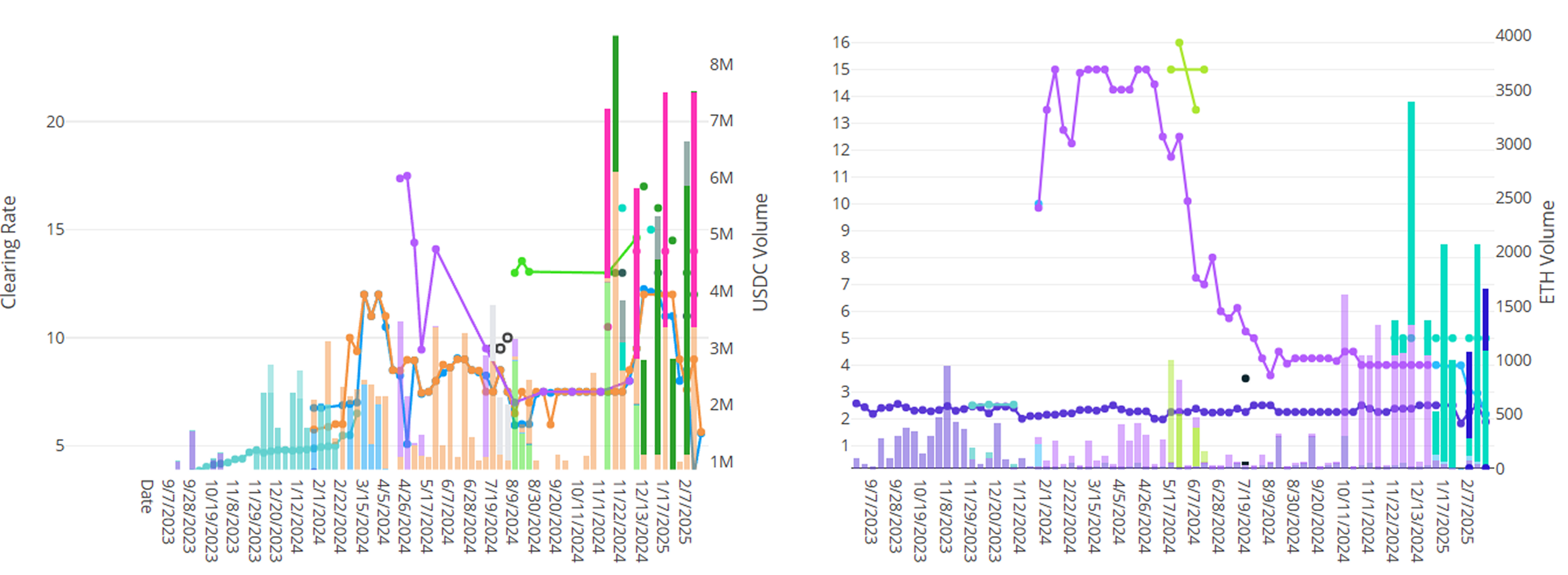

This week was a rocky week in cryptoasset markets, culminating in a $1.5BN hack at Bybit that shook the markets. Stablecoin rates and demand were down across the board this week, consistent with markets on the variable rate lending protocols. ETH borrow demand, however, remains healthy and showed continued growth with over 1500 ETH borrowed across all ETH auctions.

For those eager to lock in fixed rates and hedge against further declines in lending rates, visit our Blue Sheets Simple Earn page to explore current opportunities (Not available to U.S. persons).

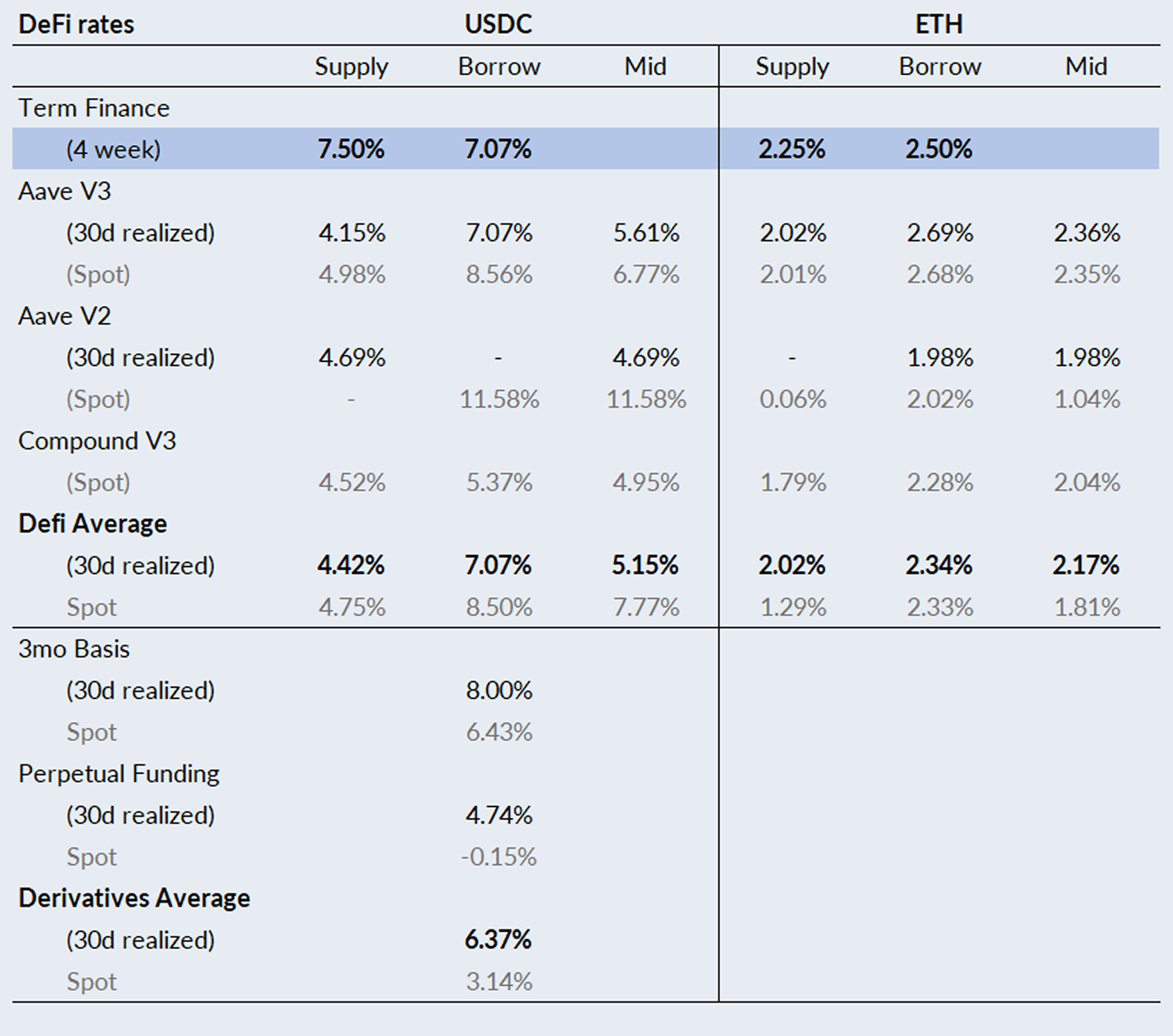

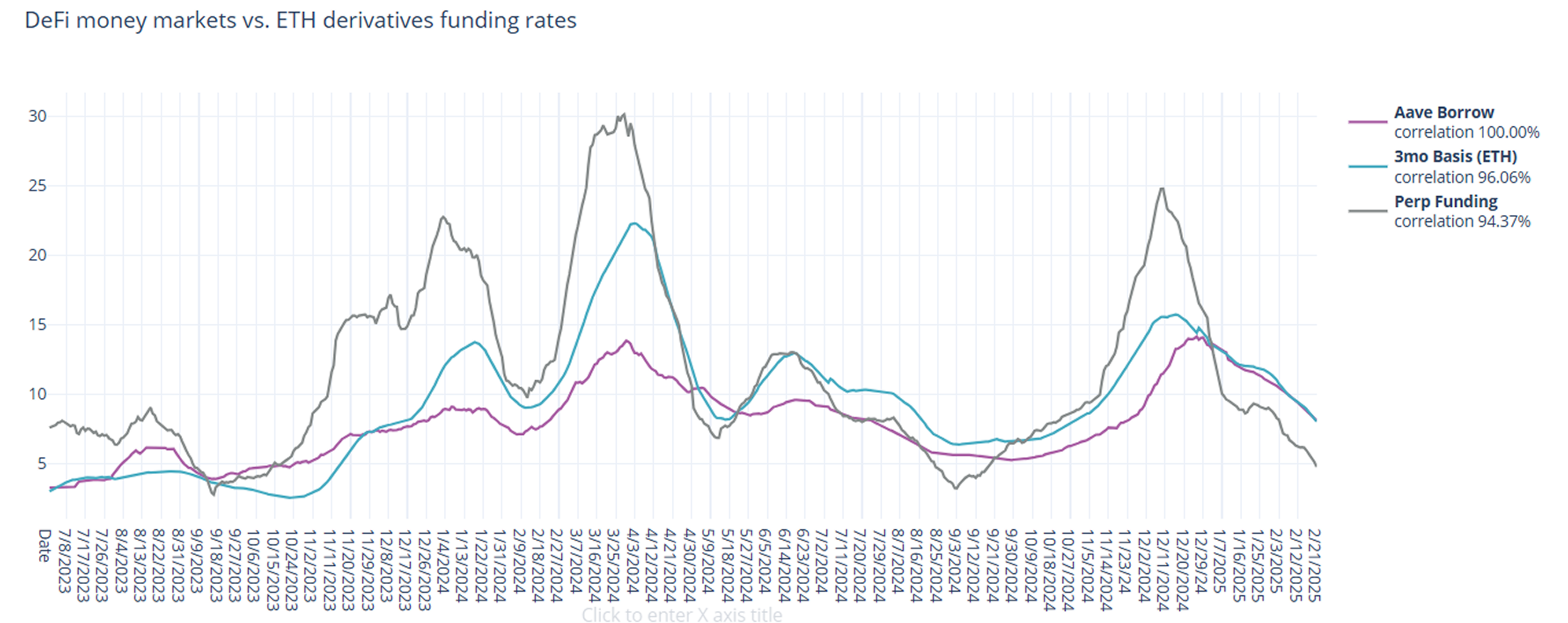

In derivatives markets, funding rates continue to freefall, with 3-month basis falling by -121bps to 8.00% and perpetual funding rates falling by -143bps to 4.74% on a 30-day trailing basis.

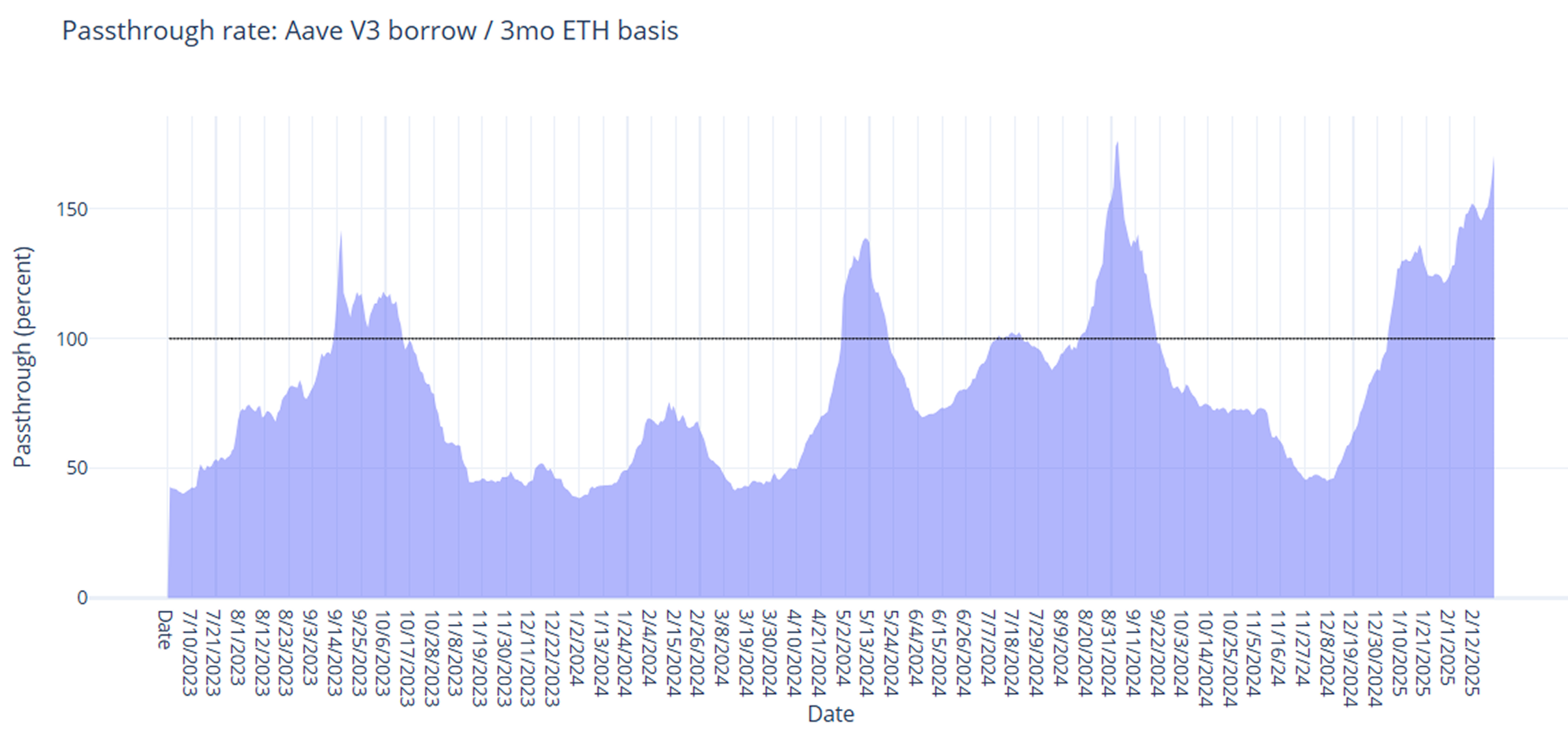

With floating rate protocols behind the curve on adjusting rates, DeFi borrow rates continue to remain elevated as compared to derivatives funding rates reaching extremes not seen since late last summer.

As they say, markets can stay irrational longer than you can stay solvent, and it certainly appears that this dynamic of mass deleveraging can go on longer than most would expect.

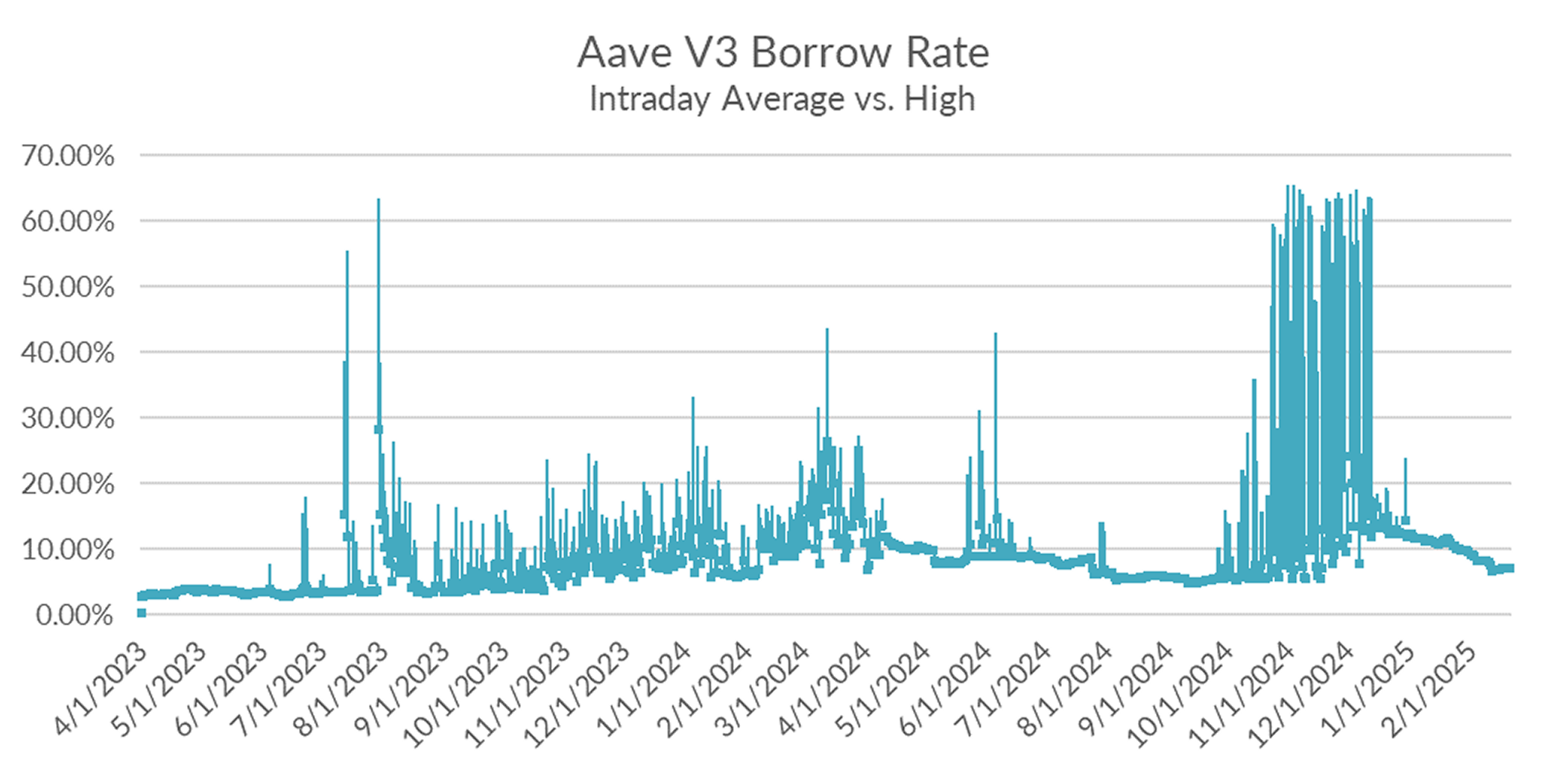

Turning to DeFi variable rate markets, floating rates continue to accelerate to the down side, closing down -98bps on the week to 8.08% on a 30-day trailing basis. Over a shorter lookback period (just seven days), Aave rates averaged 6.93% on the week, foreshadowing further declines ahead.

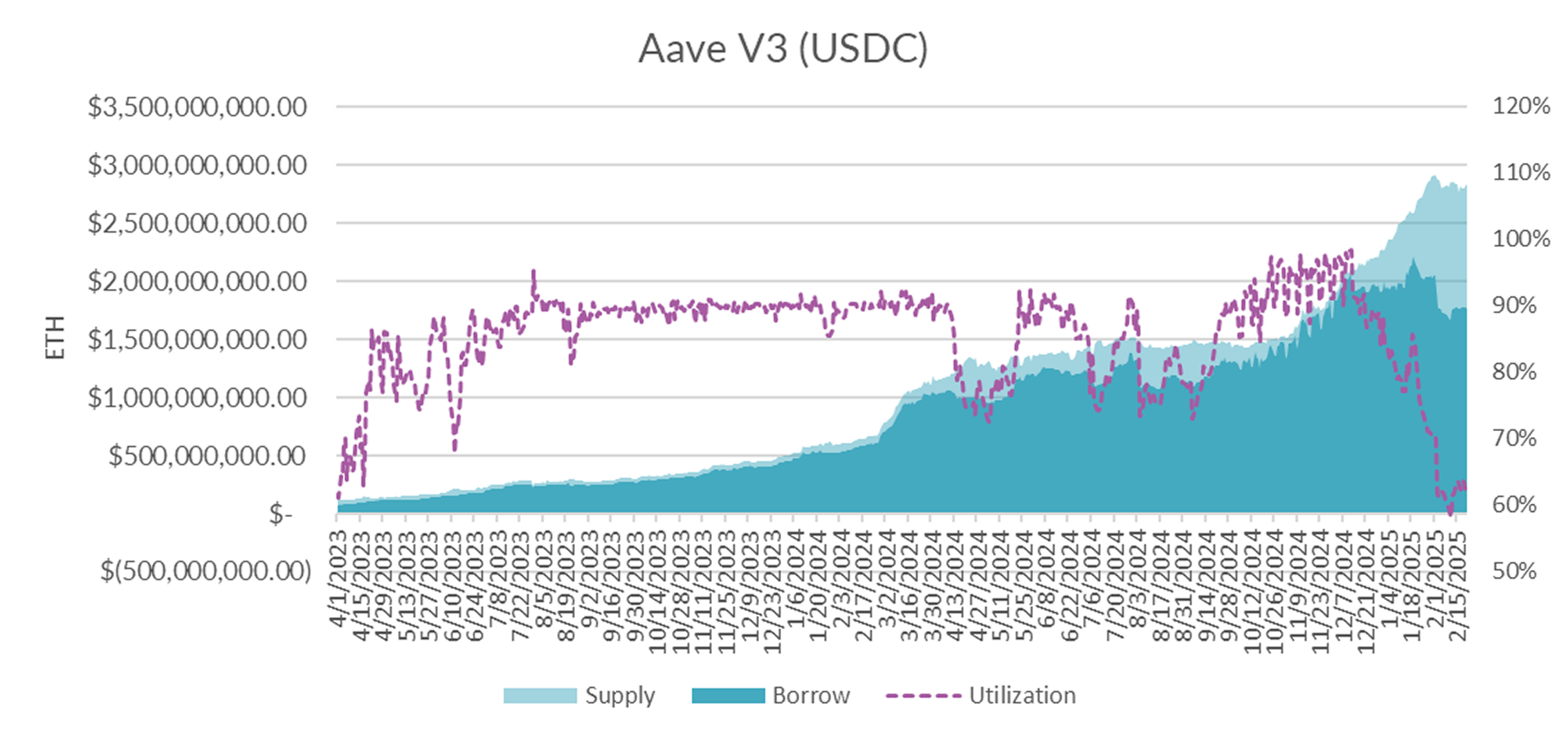

Diving in the microstructure of Aave USDC markets, utilization remains anemic, sitting at a two-year low of 62% as of the time of writing.

It seems Aave’s proposal to reduce the base rate from 11.5% to 9.5%, in line with sUSDS executive vote to reduce the savings rate to 8.75% from a couple weeks ago was too little too late.

With so much unutilized idle capital sitting on Aave, Aave suppliers are now earning LESS than 60% of the yield paid by borrowers, though this has improved slightly due to the recent reduction in the base rate.

Unless the market turns soon, Aave may have to make another adjustment in the not too distant future.

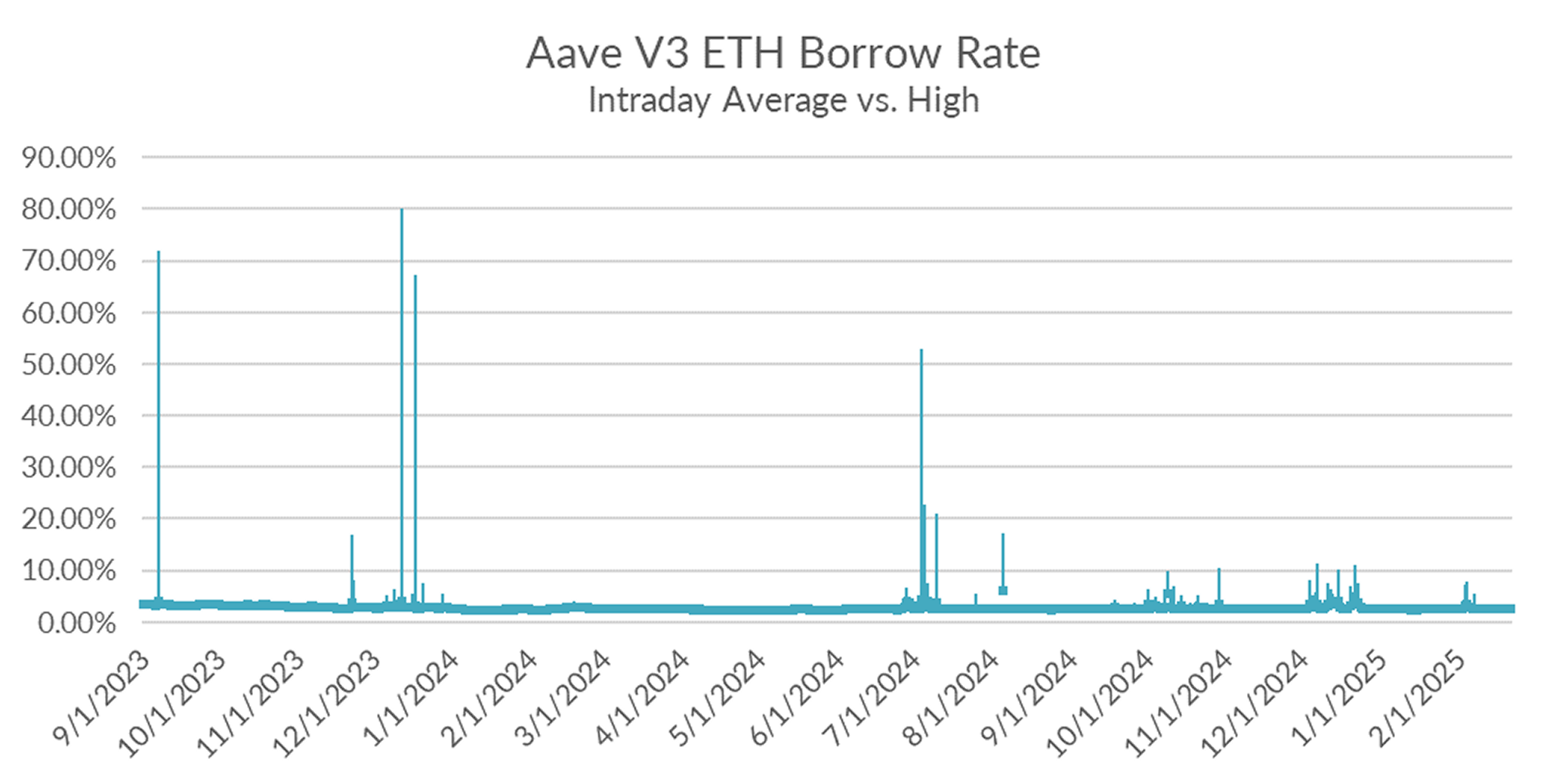

Turning now to ETH markets, ETH rates close unch’ed on the week at 2.63% on a 30-day trailing basis. The CESR index, on the other hand, declined by -6bps this week, narrowing the spread between staking and borrowing to 44bps on a 30-day trailing basis.

Market internals show that ETH supply is outpacing demand, which remains relatively stable over the past couple of weeks.

Overall, intraday volatility has settled back down to stable state due to declining utilization.

While not nearly as sharp as the fall in USDC borrow demand, ETH lending markets are also showing signs of slowing down.

With increased uncertainty in global trade and the Fed staying on hold pending signs of further decline in inflation, crypto traders appear to be abandoning leverage long positions. Nevertheless, despite the deleveraging, market prices remain stable and rangebound. This is a positive sign and suggests that the market just needs to see some positive catalyst, most likely from the Fed, to see another leg up.